Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazine7 unloved stocks: can they bounce back?

It is important to take a balanced view when doing your research either for new investment ideas or to justify keeping current holdings in your portfolio.

You should consider the positive investment case and also the challenges and headwinds facing a business, as well as any flaws in its decision making, structure or corporate culture, for example.

Many investors find it easier to work out why a company could be attractive by only looking at its growth potential. Less attention is given to the potential nasty factors that could prevent an investment from generating a positive return.

A more balanced view can sometimes be obtained by considering why other investors are negative on certain companies. You can do this by looking at the list of most shorted stocks which is published on a daily basis by the FCA, a financial regulator.

Short selling means borrowing a slug of stock from a shareholder with the goal of buying the stock back (to close the trade) at a much lower price. The goal is to profit from a fall in the share price.

This activity is inappropriate for the vast majority of investors. If you buy shares in a company the worst you can endure is a 100% loss if the company goes bust and your stock ends up being worthless. In contrast, you can lose a lot more money with shorting, far beyond the cost of your initial trade.

Shorting is incredibly high-risk and this article is certainly not encouraging you to try it out. Instead, we believe you should just look at why short-sellers are attracted to certain stocks to get you in the practice of forming more rounded views with investments and not simply looking at the upside potential.

Later on in this article we will look at the seven most unloved stocks, being the most shorted ones on the London market, and look at reasons why they could fall further or bounce back. This exercise is to primarily stimulate your thought process rather than us fishing for recovery plays.

SHORTERS WERE RIGHT WITH CARILLION

Construction services business Carillion is a prime example of where short sellers got it right. Its shares were among the most shorted on the UK stock market for about four years.

The company’s share price was falling for a long time before it eventually went bust in January 2018.

Among the reasons why it failed were taking on riskier contracts where it was hard to make a profit, payment delays from clients in the Middle East, and running up an enormous debt pile under which it eventually buckled.

Savvy shareholders who noticed the large amount of short positions on the stock may have become less willing to own Carillion and potentially got out before major damage was done. Sadly many other investors were blind to the problems and ultimately lost everything.

SHORT END OF THE STICK

Short-sellers are often viewed negatively. They can be perceived as greedy and opportunistic, if not downright manipulative, putting a bet on shares they do not own with the aim of driving down a particular share price.

Some investors take the emergence of short positions in one of their own portfolio holdings as a personal attack.

What is usually forgotten amid the emotion is the real value that short-sellers can bring. For decades short-sellers have done the hard digging required to expose corporate fraud, for example.

When analysts, fund managers and a company’s own auditor fail to identify serious problems in a business, sometimes the short-sellers can.

In some cases, the FCA or the Serious Fraud Office are only alerted to potential rule breaking after it has been exposed by a short-seller.

It was a short-seller that sniffed out the financial issues at Enron in 2001. Closer to home, it was damning analysis that led to the downfalls of AIM stocks Quindell and Globo, having taken in a host of usually savvy investors and analysts.

A generous interpretation might characterise short-sellers as the stock market’s detectives. That said, one must also recognise the potential for individuals to spread lies in order to drive down a share price for their own financial gain.

There are examples where short-sellers engage in market manipulation to achieve their returns, most notably with so-called ‘bear raids’.

Bear raiders have a functional modus operandi that involves shorting a share, then publishing allegations of wrong doing or simple ineptness in the hope of sparking panic. This usually involves researching a company’s finances well enough to discover a financial weak point or outright malpractice.

But sometimes these charges are unfair, and the bear raider is just preying on the insecurity of investors and relying on a herd-like reaction from the market.

WHO ARE THE CURRENT TARGETS?

Defence engineer Babcock (BAB) and analytics software business First Derivatives (FDP:AIM) are both examples of UK companies recently being targeted by these types of aggressive short-sellers.

Compound semiconductor wafer designer IQE (IQE:AIM) has also been targeted in the past (more about IQE later).

Today, the building industry remains in the sights of short-sellers with some investors betting heavily against contractor Kier (KIE). Others perceive a bleak Christmas for some hard-up retailers.

GETTING TO THE BOTTOM OF THE STORY

There are lots of reasons why some investors are willing to bet against a company’s share price. These range from simply believing that a current valuation is too frothy and unsustainable to a belief that corporate incompetence will get found out in time. Or, in the worst cases, that outright fraud might be uncovered.

Understanding why a company has fallen under the sceptical gaze of short-sellers is a useful exercise for all investors.

Some of the companies are popular short-seller targets for obvious reasons such as the story of struggling sales and hefty store rents at Debenhams (DEB).

For other short-selling targets, the rationale may be harder to put your finger on. Shares has done the digging and we try to explain in simple language the lure for the bears in seven cases, plus reasons why some people may still see opportunities for the shares to bounce back.

It is important to remember that short-sellers don’t always get it right and every DIY investor has the responsibility of doing their own research at all times.

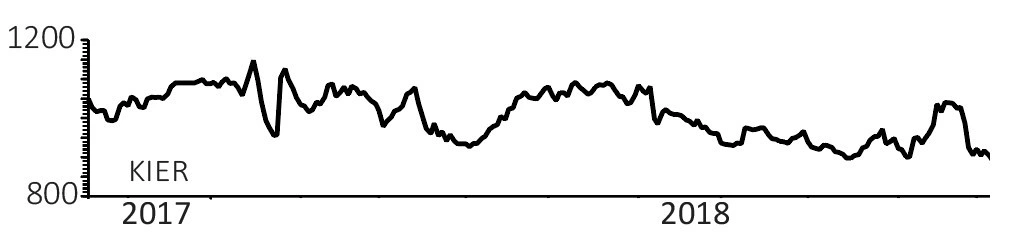

Kier (KIE) 861.5p

Proportion of stock on loan to short-sellers: 12.7%

THE BEAR CASE

Construction and infrastructure outfit Kier has been a target for short-sellers because of its high debt levels and exposure to an industry beset by contract delays and cost overruns.

Average monthly net debt is guided to fall marginally in its current financial year but at £390m is probably too high for comfort.

The fate of its counterpart Carillion earlier this year, which also was heavily shorted before it went bust, is also a big factor behind why so many people dislike Kier.

Among the issues at Carillion was the use of supply chain finance, whereby suppliers sell their invoices to a bank at a discount and effectively get paid immediately. The bank then collects from the payer (Carillion) later on.

This boosts working capital for both parties in the short-term but arguably obscures the true state of the payer’s balance sheet. Notably Kier also uses this financing option.

THE BULL CASE

The company is looking to improve its balance sheet and the recent disposal of its Australian highways business provides a useful £24m cash injection.

Kier does generate fairly robust cash flow and management incentives are now tied to average monthly net debt (as opposed to a year-end figure which could be massaged).

The firm tends to avoid the type of big unwieldy contracts which contributed to Carillion’s woes.

CHANCES OF SHARE PRICE RECOVERY OVER THE NEXT 12 MONTHS: MEDIUM

A June 2019 price-to-earnings ratio of 7.2 and a dividend yield of 7.7% suggests a lot of bad news is priced in. Yet management have little margin for error and a recent trading update (16 Nov) guiding for a second half weighting to the current year could be a precursor to a profit warning unless the trading period is executed flawlessly. (TS)

Pets at Home (PETS) 114p

Proportion of stock on loan to short-sellers: 12.6%

THE BEAR CASE

Short-sellers’ paws are all over pet food-to-veterinary services specialist Pets at Home amid competitive threats from online players and discount supermarkets, and the substantial lease commitments on the retailer’s balance sheet.

A number of management changes since Pets at Home’s 2014 stock market debut haven’t helped to foster positive sentiment either.

The need for keen prices to stay competitive is margin dilutive, and what’s more, Pets at Home’s joint venture vet practices aren’t expected to be profitable for a number of years and a shortage of veterinary practitioners is pushing up vet salaries.

Pets at Home is having to support maturing vet practices with working capital loans, which is suppressing free cash flow.

THE BULL CASE

Bulls argue the pet supplies-to-grooming salons operator offers a recovery play in a structural growth market because pet care spending is reasonably defensive.

They also point to Pets at Home’s retail business, which has shown a promising recovery in like-for-like sales, with the business becoming more competitive on pricing and a new offer of easy-repeat delivery across an array of online products.

A positive first quarter trading update (3 Aug) revealed a welcome acceleration in group like-for-like revenue growth, reflecting progress in the retail business and a like-for-like sales leap in the vets arm.

CHANCES OF SHARE PRICE RECOVERY OVER THE NEXT 12 MONTHS: MEDIUM

At 114p, shares in Pets at Home are trading on 8.3 times forecast 2019 earnings, a rating which discounts the challenges ahead yet fails to factor in Pets’ many strengths. While there is re-rating potential, we would wait for further evidence of a turnaround before considering an investment. (JC)

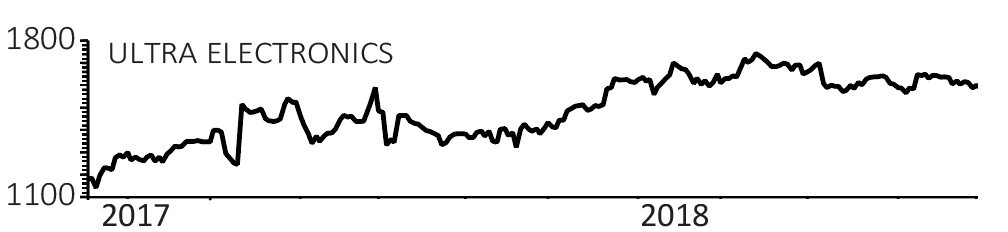

Ultra Electronics (ULE) £14.68

Proportion of stock on loan to short-sellers: 11.9%

THE BEAR CASE

The FTSE 250 electronics and software supplier is active in many industries including energy, security, transport and aerospace. It it is best known as a defence contractor to the Ministry of Defence and other national agencies.

Bears believe having so many small moving parts means that Ultra is losing focus. A patchy financial track record over recent years suggests there might be something in those claims.

Since 2013 revenue and profit have fallen as often as they have clambered higher, while analysts at investment bank Berenberg note that Ultra has failed to deliver annual organic growth since 2011.

THE BULL CASE

The responsibility for getting Ultra back on a stable growth footing falls to new chief executive Simon Pryce, in the top job since June 2018. His remit is to create an effective corporate strategy for the future, which will include a long hard look at its portfolio of operations.

That suggests bits may be hived off and sold leaving a more concentrated business capable of implementing top operational performance and financial discipline that does what a mature business should do – throw off lots of cash.

Strong relationships with key defence organisations stands it in good stead. It’s early days but if Pryce makes the right moves, he could potentially unlock very decent recovery potential from the shares.

CHANCES OF SHARE PRICE RECOVERY OVER THE NEXT 12 MONTHS: MEDIUM

The new CEO deserves the benefit of the doubt at this early stage, but investors would be wise to wait for firm signs that Pryce’s plans are bearing fruit before considering an investment. (SF)

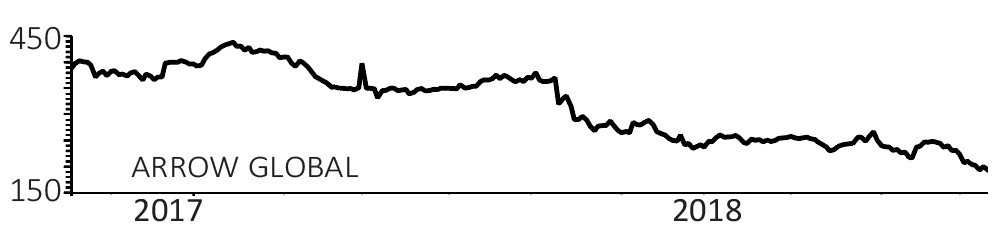

Arrow Global (ARW) 205p

Proportion of stock on loan to short-sellers: 11.5%

THE BEAR CASE

Debt purchaser Arrow Global has been widely criticised by investors for having accounts that can’t be trusted due to the large gap between actual earnings and what the company calls ‘underlying’ earnings.

These exclude the cost of refinancing its significant debt, which is an intrinsic part of its business, and give a misleading picture of the risks and returns of owning the business.

THE BULL CASE

The bulls, which includes many analysts, argue that Arrow’s business is low risk and high return with strong cash generation and potential for sizeable dividend payments in future years.

Its position in niche debt markets means it can continue to earn a premium return.

Meanwhile its asset management business provides growth and earnings stability.

CHANCES OF SHARE PRICE RECOVERY OVER THE NEXT 12 MONTHS: MEDIUM

At 200p Arrow Global currently trades on just five times consensus 2019 earnings and offers a prospective dividend yield of over 7%, so there is no doubt that Arrow Global is optically cheap.

With the majority of analysts rating the shares a ‘buy’ and a consensus price target of 270p, you can see why this stock may interest investors with an appetite for higher risk, barring an issue with the accounts. (IC)

Marks & Spencer (MKS) 291.1p

Proportion of stock on loan to short-sellers: 11.4%

THE BEAR CASE

As well as being exposed to falling in-store sales as shoppers desert the high street, its online offering is sub-standard and requires significant investment according to the short-sellers.

Its food business, which accounts for more than 50% of revenue, is underperforming with like-for-like sales down 3% in the first half.

The bears argue that restructuring plans don’t go far enough to get the company back onto a growth trajectory.

BULL CASE

Supporters of M&S point to the fact that the new management team has identified the problems and isn’t sugar-coating them.

As well as reducing the store count there is a new focus on cutting costs and complexity from its supply chain.

Also, part of the reason for food sales stagnating is a deliberate move away from promotions. A similar strategy is already paying off in clothing where full-price sales are now rising.

CHANCES OF A SHARE PRICE RECOVERY OVER THE NEXT 12 MONTHS: LOW

At 292p Marks & Spencer’s shares currently trade on 14 times consensus 2019 earnings and a prospective dividend yield of 6.5% which is at the high end historically.

Analysts are forecasting a fall in sales and operating profit next year and then zero growth for both out to 2021. Unless the company can prove them wrong the shares are likely to stay unloved. (IC)

Debenhams (DEB) 6.17p

Proportion of stock on loan to short-sellers: 11.1%

THE BEAR CASE

A structural shift to online shopping in conjunction with weaker consumer demand has decimated the core business of Debenhams. It has coughed up a string of profit warnings and remains locked in a battle for survival with a department store model ill-equipped for the new age of retailing.

Encumbered by substantial long-term lease commitments, Debenhams posted (25 Oct) a record loss of almost £500m for the year to 1 September, the biggest deficit in its history as the consumer continues to shun bricks for clicks.

The company has written down the value of assets, scrapped the final dividend and pared back planned capital expenditure plans in order to conserve cash and reduce net debt.

Supporting the short-selling thesis are negative like-for-like sales amid weak fashion and beauty markets and discounts which are eroding Debenhams’ margins. Reports of difficulties with suppliers ahead of Christmas are providing additional fodder for the bears.

THE BULL CASE

A turnaround strategy is in motion with new format stores delivering improved metrics and Debenhams’ online business growing rapidly.

One could argue that so much bad news is already in the share price, so only something as extreme as a disastrous Christmas trading period or severe financial problems may sink them further.

CHANCES OF SHARE PRICE RECOVERY OVER THE NEXT 12 MONTHS: LOW

At a bombed-out 6.17p, embattled Debenhams sells for a paltry three times the 2p of 2019 earnings forecast by Liberum Capital, a rating which suggests Debenhams is priced to go bust.

We’ve consistently been negative on Debenhams for many years and fear for the business given its long leases and the structural challenges in front of it. (JC)

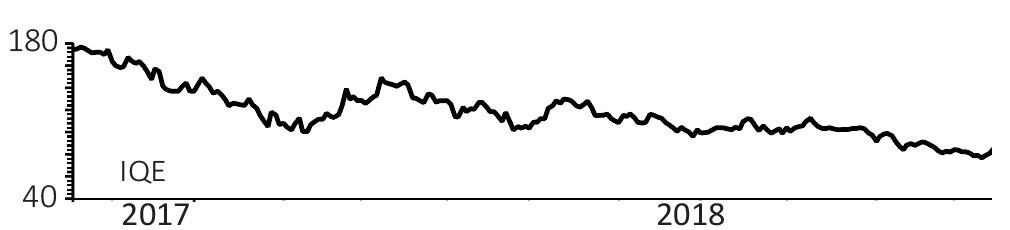

IQE (IQE:AIM) 57.3p

Proportion of stock on loan to short-sellers: 10.6%

THE BEAR CASE

When a stock jumps tenfold in price in just 15 months its investment credentials were bound to be put under the microscope, and that is the case at IQE, a compound wafers designer for the semiconductors industry.

Sceptics argue that IQE is a very expensive minor player in a complex supply chain with limited control over pricing given the scale of some of its clients.

Apple is widely believed to be among its clients, a giant of the technology industry well-known for squeezing its supply partners. Recent volume order cuts have added to the bears’ sense that IQE is still at the mercy of a smartphone industry at saturation point.

It is also fair to say that this science-heavy business is complex and misunderstood by many investors without the benefit of a PhD in physics. That leaves it open to scare mongering using terminology which can sound believable but can be aimed at causing panic among those less informed.

THE BULL CASE

Fans of IQE see the company at the very root of a technological shift away from silicon to more adaptable chemical formats, gallium arsenide (GaA) and gallium nitride (GaN), as bases for silicon microchips increasingly embedded into ‘smart’ everything.

Implied slowing Apple orders is a short-term knock, without doubt. But supporters will argue that new gizmos – such as the vertical-cavity light-emitting laser (VCSEL) technology used in facial recognition – is typically debuted in high end devices like Apple’s iPhones, only to be rolled out in much greater volumes by the legion of Android-based smartphones in time.

Android smartphones count for about 85% to 90% of all smartphones sold worldwide.

Importantly, smartphones is just one of the possible growth markets to which IQE is adapting its technology in the hope of creating vast value for shareholders. 3D technology, data centre tools, 5G next generation mobile networks and infrared applications are some of the others.

CHANCES OF SHARE PRICE RECOVERY OVER THE NEXT 12 MONTHS: MEDIUM

Judging IQE on 12 or even 24 month forecasts can make the stock look expensive, although a 2019 PE of 13.6-times suggests upside potential if order growth stabilises.

The broader semiconductor industry is under pressure at the moment, meaning sentiment may remain poor towards IQE in the near-term. (SF)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.