Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy liquidity really matters to investors

The American poet and critic Dorothy Parker once commented that ‘Love is like quicksilver in the hand. Leave the fingers open and it stays. Clutch it and it darts away’.

While hard-nosed investors looking for portfolio returns may not be unduly moved, replace the word ‘love’ with ‘liquidity’ and we are looking at an aphorism that has potential relevance for us all.

This is because liquidity – defined in investing terms as the ability to buy and sell securities – tends to be taken for granted.

Comments from two different regulatory authorities suggest investors cannot afford to assume everything can always be done at the swipe of a thumb on their smartphone or click of a mouse on their computer.

First, the Financial Conduct Authority (FCA) has revisited the issue of property and infrastructure funds. Chief executive Andrew Bailey has proposed that trading in a fund should halt if there is material uncertainty as to the value of its underlying assets.

This harks back to the summer 2016 panic that afflicted UK property funds, some of which temporarily gated clients’ cash in the wake of the referendum vote on the UK’s membership of the EU.

The FCA perhaps has an eye on next March, or whenever the proposed transition phase of Brexit comes to a conclusion. Bank of England Governor Mark Carney has also warned of the dangers that may be inherent in funds which offer the prospect of instant liquidity even if they hold what are inherently illiquid assets.

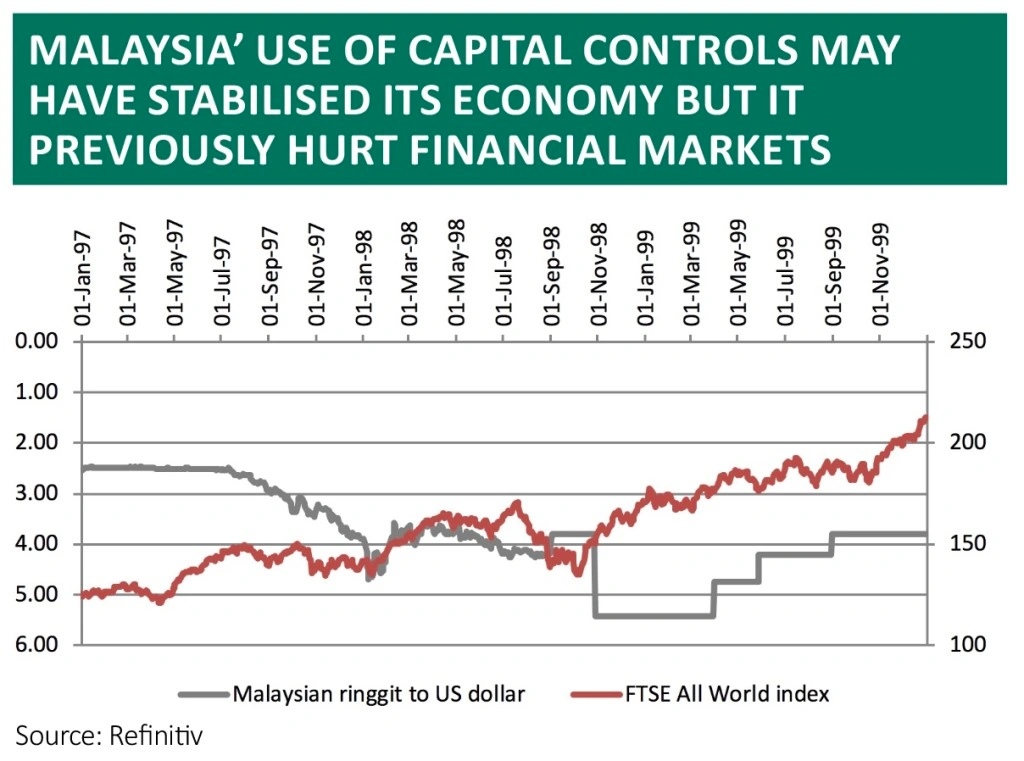

Second, Malaysia’s central bank governor, Nor Shamsiah Mohd Yunus, has argued that capital controls should be considered as a tool when it comes to pre-empting a financial crisis. This flies in the face of current International Monetary Fund orthodoxy. It also brings back unhappy memories for investors who have emerging market exposure.

Malaysia went down the path of capital controls in 1998 with horrible results for financial markets.

The Malaysian stock market plunged and those investors who found themselves with assets stranded in ringgit on the Kuala Lumpur exchanges looked to sell assets in other emerging markets.

They wanted to sell to avoid the risk of similar moves in other emerging markets and also raise liquidity to protect themselves (and in the case of emerging market fund managers to meet redemptions from their own nervous investors).

The contagion eventually reached developed markets and global equities tumbled in the wake of a seemingly unrelated Asian currency crisis.

WELL-TIMED WARNINGS

The Investment Company Institute’s 2018 Investment Company Fact Book reveals that regulated open-ended funds now manage $49 trillion, up from $22 trillion a decade ago. That represents just under one quarter of the globe’s securities markets, at least partly buoyed by the rise of exchange-traded funds (ETFs).

ETFs rely on the sort of liquidity that the Malaysians would consider taking away, if push to ever came to shove. And if underlying markets do prove illiquid then the funds themselves could struggle to meet redemptions, whether the collectives invest in stocks or bonds, let alone property or infrastructure projects.

This is a reminder that liquidity is not just being able to press a button and trade. True liquidity is dealing in the size, at the price and at the time that you want. Malaysia in 1998 and UK property funds in 2016 are examples of how this cannot be taken for granted.

None of this is to say a market accident or crash is imminent, even if cryptocurrencies and emerging market equities are already in bear market territory, and even the FAANG-plus index of leading technology stocks is suffering a correction after a 10%-plus tumble.

But rising volatility and rising interest rates raise the issue of whether investors should now be taking more or less risk at this stage of the cycle.

It is hard to think many investors are going to head into cash as the returns are so poor and the issue of timing market exit and entry points too fraught. But relying on liquidity – and the ability to redeem instantly to avoid trouble – may not be a good idea, either.

As such, investors should check their portfolios to ensure they are happy with every element of asset allocation and fund selection for the (very) long term. There is a chance any market downturn will make getting out of those positions at their preferred time, at their preferred price and in their chosen size, harder than they think.

As John Kenneth Galbraith noted in his seminal tome from 1955 The Great Crash: ‘Of all of the mysteries of the stock exchange there is none impenetrable as why there should be a buyer for everyone who seeks to sell. October 24 1929 showed that what is mysterious is not inevitable.

‘Often there were no buyers, and only after wide vertical declines could anyone be induced to bid. Repeatedly and in many instances there was a plethora of selling and no buyers at all.’

Russ Mould, investment director, AJ Bell

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.