Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThe magic ingredients: 2 simple rules to better investing

There are few truly great investors who reliably beat the market, and even they will admit they don’t get it right every time.

Most investors, private and professional, are doing well if they can match an index over the long term.

Even if you invest with a professional manager who does perform in line with the index, after management fees your returns will be lower.

That is one of the reasons why index investing has become so popular over the last decade. If you don’t have the time or the skill to pick stocks yourself, by using an index or tracker fund you can get the same return as the market with much lower fees than an actively-managed fund.

While that’s fine if you want to invest in funds, what about those who are happy to invest in individual company shares – is there any way you can get some help to beat the market? The answer is yes.

THE ORIGIN OF THE ‘MAGIC FORMULA’

In Little Book That Beats The Market, veteran money manager Joel Greenblatt argues that you can succeed. Moreover he argues that anyone can do it, and that the results are repeatable.

Greenblatt wrote in his book, published in 2006, that a portfolio of 30 stocks following his ‘Magic Formula’ delivered approximately 30.8% per year in the preceding 17 years. During that period the overall market averaged a return of 12.3% a year.

In the book he argues that investors need to view their relationship with companies as if they are actively involved in them.

He sets out two simple criteria for buying companies. The first is to only buy good businesses, the second is only to buy them at bargain prices.

HOW TO IDENTIFY A GOOD BUSINESS

How do we measure whether a firm is good? After all, it’s hard to quantify the quality of a firm’s products, the value of its brands, the loyalty of its customers or the skill of its management in financial terms.

Rather than try to estimate a company’s value, we should stick to what we know, starting with how much money it made last year and how much capital it used in the process. In other words, what was its return on capital?

We’ve covered return on capital as a measure before (see Shares, 30 November 2017, How experts find the best companies) but in a nutshell the higher the return, the better the business.

If in the normal course of running its business Firm A uses £1bn of capital and generates operating profit of £150m per year, its return on capital is 15%.

If Firm B also uses £1bn of capital but only generates £50m of operating profit per year its return on capital is just 5%.

That’s obviously a better return than the 1.5% yield on 10-year UK government bonds (gilts), the risk-free alternative, but it’s not as good as Firm A.

It’s also only half the average return on capital employed for all the firms in the FTSE 100 (10.3%).

The reason that operating profit – also known as EBIT (earnings before interest and tax) – is a better measure than pre-tax profit is that companies all have different levels of debt and different tax rates.

Companies publish their operating profit every quarter or every half year, making it easy to track, but they only tend to publish capital employed in their audited full-year results.

Helpfully on Shares’ website there is a record of both operating profit and capital employed so you just have to divide one by the other. Search for a specific stock and then go the quote page. Click the ‘Fundamentals’ tab and you’ll find all the necessary data.

Returns on capital tend to be higher for businesses with few fixed assets and little working capital than for companies with lots of fixed assets (like electric utilities) or those that need lots of capital (like banks).

Using return on capital as a measure of how good each business is, we can now rank them from best to worst.

TWO SIMPLE STEPS TO BETTER INVESTING

HOW TO IDENTIFY A CHEAP BUSINESS

The second step is to buy good businesses at bargain prices. If the market is efficient, surely there aren’t any good businesses at bargain prices?

To be fair, a lot of stocks which look like bargains are usually cheap for a reason, namely they aren’t very good businesses.

However, just as there are times when investors get carried away with the prospects for stocks and pay sky-high prices, there are times when they become gloomy and decide they won’t buy at almost any price.

This is where it’s important to distinguish between price and value. Share prices can change rapidly, often for no reason other than sentiment, while the underlying value of a business changes relatively slowly.

If we already know what a company’s operating profit is, we can divide that profit by the ‘enterprise value’, which is the current market capitalisation plus net debt, to get the earnings yield.

As with return on capital employed, typically the higher the yield the more attractive the business.

Using the previous example, we already know that Firm A has an operating profit of £150m. If its enterprise value is £1bn, then its earnings yield is 15%.

We also know that Firm B has an operating profit of £50m. If its enterprise value is also £1bn, then its earnings yield is 5%. Therefore Firm A is cheaper/more attractive than Firm B.

Using the earnings yield, we can rank stocks from best to worst as we did with return on capital. Finally we can take the two rankings and see which stocks come out top by their combined score.

Typically a balanced portfolio will have somewhere between 20 and 30 stocks. The ultimate choice may depend on liquidity although as individual investors it’s unlikely we would want to buy enough shares to ‘move the market’ even in a small-cap stock.

IT'S ALL ABOUT COMMITMENT

This simple, intuitive method has been shown to beat the market and just about every professional investor over decades.

The key phrase in the last sentence is ‘over decades’, because here’s the first rule: you have to stick with this method for many years, through thick and thin, for it to work.

Typically when a stock-picking process stops working for a while and investors start to see losses, most of them will give up and try a different strategy.

Most professional managers are measured on their quarterly performance so they can’t afford to see losses for very long or they’re out of a job. This means you have a big advantage if you can stick with the process.

The reason you need to stick with it for a long time is the power of compounding, which Albert Einstein is said to have described as ‘the most powerful force in the universe’.

If you start with £10,000 and you make a 10% return every year for 10 years, your investment does not become £20,000 (£10,000 plus 10 x £1,000) but £25,937 because every year you are making a 10% return on a higher number.

If you do that for 30 years, by the power of compounding your £10,000 will have turned into £174,494. First you have to generate 10% annually to achieve these returns.

BE YOUR OWN ONCE-A-YEAR FUND MANAGER

The second rule is that the list of top stocks changes over time as shares go up and they drop down the list in terms of cheapness.

Therefore you need to spend one day a year to run your screen, remove the stocks which no longer meet the criteria and add those that do.

We would add a third rule, that stocks should be equally-weighted. Giving stocks an equal weighting minimises the damage if – or rather when – one of them fails, because the law of averages says that at some point some of them will fail.

Also by equally-weighting stocks you are getting away from the market capitalisation weighting of the index, which is something the majority of professional fund managers aren’t allowed to do.

So which stocks tick the right boxes using our combination of quality (return on capital) and value (earnings yield)?

Financial website Stockopedia has a pre-built Magic Formula screen which produces a list of 30 stocks which match the criteria desired by Joel Greenblatt. You have to pay a fee to access this information, although we can reveal a few names from its list in this article.

Stockopedia’s system uses trailing 12 month data which means it takes into account any recent half year results announcements, rather than simply relying on the last published set of full year results. The latter can become out of date as a company reports through the year, particularly if they’ve enjoyed positive momentum with their business.

Some of the stocks on Stockopedia’s list are not good investments, in our opinion. For example, logistics group Connect (CNCT) appears on the list, yet it has recently suffered a major profit warning and there are clearly major challenges for it to overcome.

It acts as a good reminder not to assume that all stock screeners will give you superb investment ideas. They can help to filter the market but you will still need to do your own research afterwards.

We’ve gone through Stockopedia’s Magic Formula screen and picked four stocks which pass our quality test and are worth buying. Read on to learn why we like De La Rue (DLAR), Dairy Crest (DCG), Gem Diamonds (GEMD) and SciSys (SSY:AIM).

Dairy Crest (DCG) 467p BUY

Shares in food producer Dairy Crest currently languish at 467p as poor sentiment reflects concerns over profit-impinging input costs and limited pricing power. We see merit in buying the shares at the current price for several reasons.

The firm behind the Cathedral City, Clover and Country Life grocery brands, as well as rapidly growing non-dairy spread offering Vitalite, generates a high return on capital.

It leverages high quality assets, a strong supply chain and leading industry positions to generate industry-leading margins, while a commitment to new product innovation augurs well for the future of the business.

Despite cut-throat levels of competition, in the first half of the financial year, Dairy Crest saw strong performances from its two biggest brands, Cathedral City and Clover.

Besides the core branded groceries business, Dairy Crest offers upside through a fast-developing functional ingredients business with tasty global growth potential.

For the year to March 2019, Shore Capital forecasts pre-tax profit improvement to £66.7m (2018: £62.3m) and a dividend hike from 22.6p to 22.8p, meaning there’s a portfolio-nourishing 4.9% prospective yield on offer. (JC)

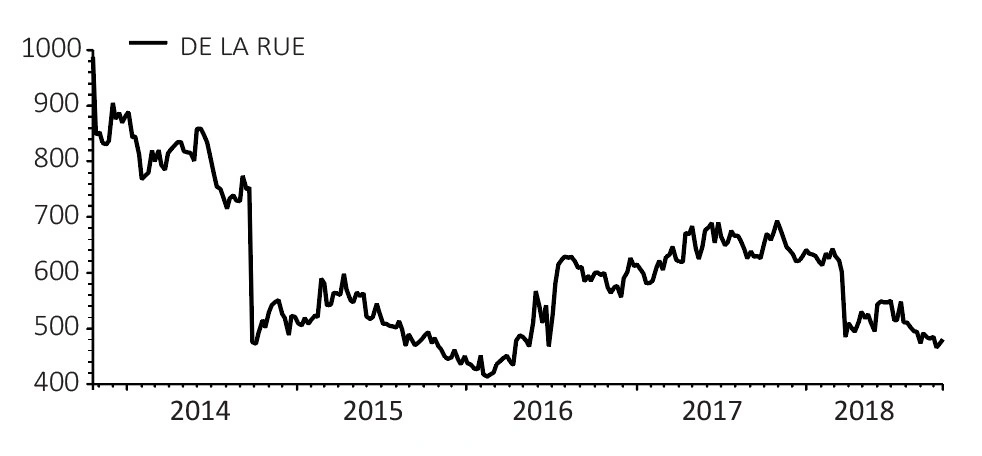

De La Rue (DLAR) 484p BUY

You may wonder why we are saying to buy De La Rue. After all, it is the world’s largest printer of banknotes in a world which is increasingly cashless.

It also prints passports, but earlier this year lost out to Dutch rival Gemalto on a lucrative contract to design and manufacture the new

blue British passport.

The shares aren’t far away from their decade-lows of 2015, and to cap it all management are under fire from activists investors.

This last point is a positive. It often takes an outsider to shake things up when a company and/or its management is under-performing.

Despite its troubles De La Rue is a very profitable company. Banknotes and passports need extremely sophisticated security features to protect against forgery, and that kind of technology is very valuable.

Its capital employed is actually negative because it has very low fixed assets and its gets its customers often pay upfront.

Its earnings yield is almost 22% as earnings before interest and tax (EBIT) was £123m for the full year to March 2018 and its enterprise value is £564m.

Investor sentiment is negative yet analysts are uniformly bullish with an average 600p price target. We think this is a good one to buy, albeit not for impatient investors. (IC)

Gem Diamonds (GEMD) 116.5p BUY

Asset quality makes all the difference in the world of mining and Gem Diamonds’ Letseng mine in Lesotho is really top class. It is impossible to accurately predict when the next big diamond will be found, yet history tells us to expect high quality ones when they do come along.

After a long period of not finding much, plus weak diamond prices forcing it to close another mine, Gem Diamonds has bounced back into fashion this year. So far in 2018 it has found 12 diamonds in excess of 100 carats – an outstanding result.

A renewed focus on mine planning to reduce the amount of waste material being mined should help to enhance value. Earnings are expected to soar over the coming years thanks to the good run of large diamond discoveries, cost savings and productivity improvements.

We acknowledge the share price has already enjoyed a strong run this year. However, we feel now is still a good time to buy the stock as the business is in a better position both strategically and financially.

Investment bank Berenberg notes that Gem has a mixed track record with acquisitions. While Letseng was a super buy, the business has also impaired c$739m of investments over 11 years. It reckons Gem will no longer pursue acquisitions, instead preferring to focus on Letseng, strengthening its balance sheet and returning capital to shareholders. (DC)

SciSys (SSY:AIM) 143.11p BUY

Pulling a newly energised growth rabbit out of the hat has done wonders for SciSys over the past couple of years, transforming the company’s financial performance and its share price.

SciSys is a Chippenham-based IT projects, tools and services provider to large public sector, broadcast media and space industry clients.

The UK’s Ministry of Defence is a big public sector client, while it has worked for years with the BBC and European Space Agency (ESA), including on its Galileo and Mars missions.

SciSys has always been a solid little company, profitable, cash generative and paying regular dividends but it lacked the growth oomph craved by most investors. That situation has now changed with pre-tax profit forecast to grow by 21% this year and by 15% next year.

The shares have been sold off steeply during the recent market shake-out, much of which relates to Brexit worries because of SciSys’ ESA contracts. That presents a good opportunity to buy cheaply.

Management should be applauded for taking a belt and braces stand, announcing last week a structural re-jig that will keep its AIM listing intact but moving its corporate base to Ireland.

We’ve spotted some discrepancies between Stockopedia’s data and information published by broker FinnCap on SciSys, so we’ve decided to do some calculations ourselves using data from the latter. We reckon it has an 11.8% earnings yield and trades on a 10.4-times price-to-earnings ratio, using FinnCap’s forecasts for 2019. (SF)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.