Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineHow to buy £1 of assets for 50p

Deep value investing involves buying bargain basement shares in

the hope they will eventually move back to their intrinsic value. It is a strategy that has forged the reputations of some of the world’s greatest investors.

Value investing can be highly volatile and takes a lot of patience; hence many fund managers shy away from it. However, current practitioners include Kevin Murphy and Nick Kirrage, custodians of the Schroder Recovery (B3VVG60) fund, as well as British Empire Trust (BTEM).

The latter is managed by Joe Bauernfreund who also runs newly-listed AVI Japan Opportunity Trust (AJOT), an investment trust seeking opportunities in cash-rich Japanese firms which he believes to be under-researched and undervalued.

One of our favourite ways to play the deep value theme is via SVS Church House Deep Value Investment Fund (BLY2BF0). It is the brainchild of Dutch deep value master Jeroen Bos who is prepared to stand alone from the crowd and patiently await the upside from his often beaten-up stock picks.

Bos justifies a company’s value based on balance sheet information rather than future earnings forecasts. His goal is to find companies where the balance sheet assets outnumber the liabilities.

He trawls the market for so-called ‘net-net investments’, first described by legendary investor and Warren Buffett mentor Benjamin Graham. This is when the current assets of the company outnumber all of its liabilities, enabling investors, theoretically, to buy £1 for 50p.

On a cumulative basis, according to financial data group Trustnet, the fund is down 1.3% on a one-year basis, but has returned 41.3% and 19.1% on a three and five-year basis.

Bos says his portfolio has had a ‘pretty good run’ in 2018, being up 8.4% year-to-date, and is delighted with the award of a five-Crown rating by Trustnet in July. The FE Crown fund ratings seek to reward superior performance in terms of stock picking, consistency of outperformance and risk control.

The portfolio currently contains 23 stocks with a bias towards UK small cap and AIM stocks, at 29.9% and 33.3% of

the portfolio respectively, with 6.9% in the FTSE 100 and 1.3% in the FTSE 250 and 20.2% in treasury stock.

COMPETITIVE ADVANTAGE

Bos tells Shares that new EU legislation known as MiFID II

has been ‘a godsend to me’. These rules have made it harder for equity research to reach a wide audience, meaning many investors have a reduced pool of ideas. ‘For me, I know I’m the only one with a view or who’ll bother to do the homework (on certain companies), so my chances are much bigger now than they were previously.’

One of his portfolio holdings is oil and gas industry products supplier Enteq Upstream (NTQ:AIM). The shares have been flat since the summer, yet Bos remains confident about its prospects. ‘The management of this company is excellent and has done a fantastic job in the recession, cutting back on any kind of expenditure.

‘They previously bought oil and gas products play Sondex to the market for 100p and it was bought by General Electric in 2007 for 460p,’ he adds.

The fund manager believes Enteq’s share price can at least double and potentially repeat the Sondex trick, growing the business to such a strong position that it draws a takeover bid. He says cash-rich Enteq is ‘starting to make all the right noises’ and ‘we are getting close to the moment when this thing will start to take off’.

OTHER STOCKS IN THE PORTFOLIO

Bos is also a patient holder of unloved oil rig assembler Lamprell (LAM), UAE-based and boasting a strong balance sheet flush with $167.8m cash.

He believes Lamprell will eventually benefit from the upswing in the oil industry and given the massive cash pile, insists ‘the world will have come to an end’ before the company goes bankrupt. ‘It is all red ink when you look at this thing, but fundamentally, Lamprell is very, very cheap.’

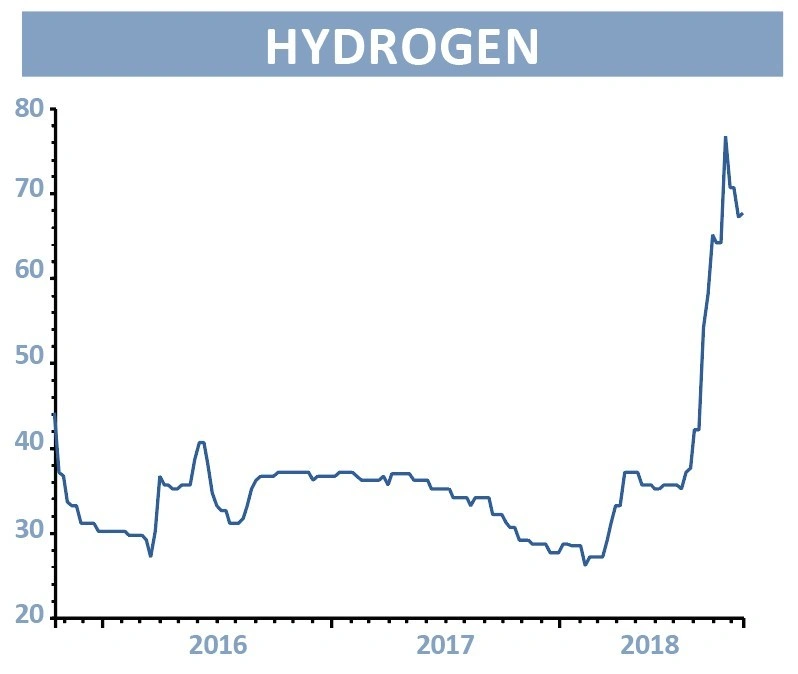

Among Bos’ winners is recruiter Hydrogen (HYDG:AIM), a classic net-net purchased at an average price of 28p and the ‘outstanding performer this year’, currently swapping hands at 67p.

In fact, Hydrogen enjoyed such a stellar run that the position hit the fund’s 10% limit, forcing the fund manager to sell some of his shares.

Co-founder Ian Temple has returned as CEO and restructured the company which has also resumed dividends. Hydrogen’s shares rose on recent half year results which confirmed the company’s strong rebound in profitability and triggered material earnings upgrades. ‘Once these companies return (to profitability), they return in

a very healthy way,’ adds Bos.

GAME ON FOR GAME DIGITAL?

Bos has continued to build up the fund’s position in bombed-out Game Digital (GMD), the retailer-turned-eSports venue organiser purchased as a debt free net-net at an average price paid of 32p. ‘I found this one and I got terribly excited. I don’t like this sector but this one is different,’ he says.

While Game Digital faces short-term trading pressures,

its BELONG gaming arena concept may interest some investors where the first sites under Game Digital’s joint venture agreement with shareholder Sports Direct (SPD) are now opening.

The shares are firmly in deep value territory, trading at 29.6p, less than the company’s 32p per share net cash position. (JC)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.