Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineB&M snaps up French rival Babou

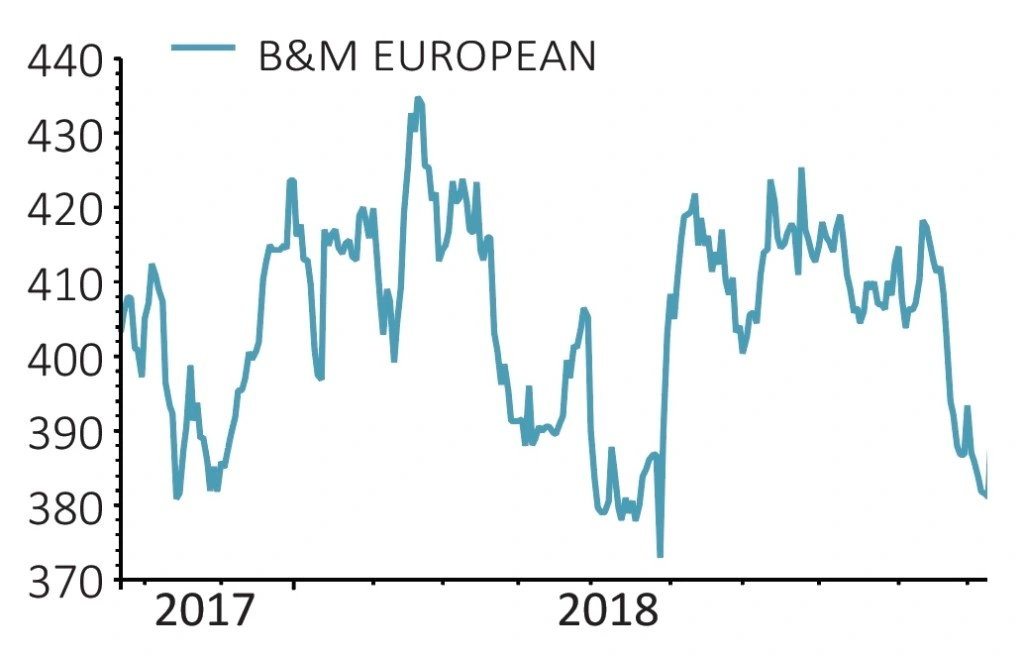

B&M EUROPEAN VALUE RETAIL (BME) 391.2p

Loss to date: 6.4%

Original entry point: Buy at 418p, 1 February 2018

We’re sticking with our bullish stance on multi-price discounter B&M European Value Retail (BME), albeit irked by a share price drift to 391.2p that leaves our trade languishing in a modest loss.

B&M’s acquisition (19 Oct) of Babou Stores in France for €91.2m provides a base which will enable the Simon Arora-led firm to develop and grow its proven, profitable value retail model across the channel.

Babou is a 95-store-strong chain of discount general merchandise outlets. The average store size, location and customer base of Babou are comparable to the flourishing B&M Homestore operation in the UK.

France, alongside the existing German and UK markets in which B&M operates, has attractive dynamics in terms of overall size, the rising popularity of the discount channel and the healthy operating margins achieved by several incumbent players.

While the retail sector struggles, B&M is a self-funded growth business, a cash generative concern offering a play on trends towards value and convenience, and scope for higher ordinary dividends and special payouts on top.

Numis Securities welcomes the Babou deal, moving its recommendation from ‘add’ to ‘buy’ following a soft share price run; the broker’s 475p price target implies 21.5% upside from these levels.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.