Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineVenture capital trusts offer significant tax benefits but are they suitable for all investors?

The new venture capital trust (VCT) offer season is now in full swing where investors are able to apply for new shares and enjoy immediate tax benefits.

Recent offers from Amati AIM VCT, Octopus AIM VCT and Hazel Renewable Energy VCT have already closed, having hit their subscription target. Others are filling up quickly.

Each year VCTs seem to attract money faster than the previous year, meaning interested investors need to act fast once offers go live.

This article will explain all the essential points about why and how to invest in VCTs, plus the important points to note if you want to lower the risk of losing money.

WHY WOULD YOU WANT TO INVEST IN A VCT?

Venture capital trusts are funds that allow investors to claim up to 30% income tax relief on up to £200,000 invested in a VCT per year. You need to hold the investment for at least five years, but any dividends will be tax free and you will have a capital gains exemption on disposal.

The tax benefits are essentially compensation for taking on the extra risks of investing in growth companies, some of which could be early-stage businesses.

WHO IS BEST SUITED TO INVESTING IN A VCT?

Individuals on higher-rate or additional rate tax bands are naturally drawn to VCTs because of their tax benefits.

VCTs can also be of interest to someone who wants to invest in early stage growth companies or individuals who have maxed out allowances on various wrappers such as ISAs and hit or exceeded the £1.03m pension lifetime allowance.

These funds are popular among individuals seeking to supplement their income because dividends and returns from selling down capital are tax free.

Stuart Veale, managing partner at asset manager ProVen, says VCTs are not simply the domain of high net worth individuals, noting that the average investment size in its products is £12,000 and that many investors opt for its minimum £5,000 subscription.

Hugi Clarke, a director at VCT provider Foresight, says there are two obvious candidates for the VCT market. One is someone trying to resolve a persistent tax problem; the other is someone with a one-off exceptional tax charge as you can use the 30% relief to reduce your tax bill.

‘It is becoming quite common for people to face lifetime allowance issues,’ says Clarke, referring to the limit on the amount of pension benefit that can be drawn from pension schemes and paid without triggering an extra tax charge.

‘Individuals in this situation may have either built up a sizeable pension pot, or they’ve transferred out of a defined benefit scheme with a substantial sum of money.’

One solution for anyone in this situation who is still saving for retirement is to put further contributions into a VCT rather than a pension as it is more tax efficient in such circumstances. It is very important to understand the risks if taking this route.

LONG-TERM BENEFITS

VCTs can also benefit individuals who haven’t hit the pension lifetime allowance, assuming they are happy to let their money grow and don’t need to access it in the near-term.

For example, a 40 year old could invest money into a VCT and get 30% tax relief. After five years they can reinvest the proceeds of that first VCT into a new product and get another 30% tax relief. If they repeat this pattern, the individual could have invested in five VCTs back-to-back in five year batches and enjoyed considerable tax relief by the time they turn 65.

They could then take this money as a tax free lump sum in retirement or keep the money invested in a VCT and draw tax free dividends as an income.

The downside of the latter strategy is that VCT investments may be too risky for someone of that age. And don’t forget that you shouldn’t invest in something for the tax breaks alone.

WHO SHOULDN’T INVEST IN A VCT?

VCTs should be avoided if you need to access your money in less than five years and if you don’t have the stomach or patience for exposure to early-stage businesses.

Selling before five years is up will require you to pay back the 30% tax relief to the taxman. You also have to consider there isn’t always a liquid market for VCTs as most people only buy them in an offer period and don’t trade them on the market. That said, some VCT providers do offer to buy back shares at a 5% to 10% discount to net asset value.

‘Someone who is equity market risk averse shouldn’t invest in a VCT,’ says David Stevenson, fund manager at Amati. ‘The tax benefits would be outweighed by the fact they can’t sleep soundly at night.’

Stevenson suggests other people not suited to VCTs are those who are under-invested in a pension, don’t have a pension at all, or are a non-taxpayer.

HOW DO YOU BUY THEM?

You should buy VCTs direct from the fund manager or a specialist VCT broker during the offer periods to get all the tax benefits.

You can buy VCTs on the open market (also known as the secondary market) but you would lose the 30% income tax relief.

THE DIFFERENT TYPES OF VCTS

There are three different types of VCTs, each suitable for different types of investors: Generalists, AIM VCTs and Limited Life VCTs.

‘Generalists are classic venture capital businesses looking for the next big thing,’ says Eliot Kaye, a director at Puma Investments. ‘They need to win big and it can take years to find and realise a successful investment.’

AIM VCTs invest in AIM-quoted companies either when they join the stock market, participating in their IPO offer, or taking part in fundraising. Fund managers can only buy shares when a company is seeking new money, not simply picking up existing stock on the market in the way a normal investor would buy shares.

Limited Life VCTs are products that aim to preserve your capital – you’re likely to only make money from the tax relief component. They are deemed to be lower risk than Generalist and AIM VCTs.

GENERALIST VCTS

The traditional venture capital model is to back pre-revenue or pre-profit companies. These companies may have a strong idea and spend a lot on research and development, but still be lacking scale. ‘A venture capital manager should expect half of their investee companies to fail,’ says Hugi Clarke at Foresight.

‘Your average investor may not be used to thinking that one out of every two investments will fail, but it isn’t unrealistic for the VC market.

‘Against the failures, a venture capital trust could have two or three investments which succeed very big, such as 10 to 40 times return on capital.’

Private equity-style venture capital trusts will invest in revenue-generating companies where the failure rate is lower, says Clarke. ‘The trade-off is that your winners won’t be as big, perhaps three to six-times return. It is a less bumpy ride, so total return might not be as spectacular but nor are your potential losses.’

Foresight is among the private equity-style venture capital experts seeking to raise new cash; in this case its Foresight 4 VCT wants to raise £50m for new investments and had so far secured £13.1m at the time of writing.

The current portfolio includes stakes in computer graphics card manufacturer Datapath and prepaid electronic payment service Ixaris Systems.

LOOKING FURTHER AFIELD

Foresight differentiates itself from much of the competition by having offices across the UK, rather than simply being concentrated on the London and South East market which Clarke says is highly competitive for new investments.

‘We wouldn’t invest when there is only a bright idea like a business selling hot dogs and champagne. It is better to invest when there is a proven business model.

‘For example, we backed Mowgli Street Food. The founder is a barrister who grew frustrated at the quality of Indian food in the UK, full of butter and fat. It was profitable with three locations when we came across the business. The founder wanted to add more sites in the UK but didn’t have capital to expand, hence how we were able to help.’

Calculus VCT, Pembroke VCT, Seneca Growth Capital VCT and Maven Income & Growth are among the Generalist VCT products with live offers at present.

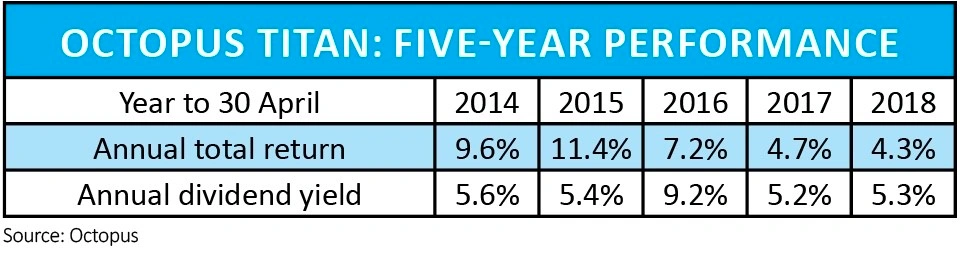

THE STRATEGY BEHIND OCTOPUS TITAN

The biggest VCT player in the Generalist segment of the market is Octopus whose Titan product is currently seeking to raise £120m. ‘We seek to invest in high growth businesses, typically UK-based ones that are trying to address global markets,’ says Jo Oliver, fund manager for Octopus Titan VCT. ‘The management are looking to solve big problems and we hope these businesses could eventually be worth in the hundreds of millions of pounds, or even billions.

‘We invest in some very early stage companies that are pre-revenue but the majority of the portfolio companies in Titan tend to be pre-profit.’

Oliver says he typically invests a small amount and then does follow-on investments if the business is performing well. ‘We hope for 10-times return potential but we have achieved 80-times in the past.’

Titan currently has 65 companies in its portfolio including WaveOptics which the fund manager describes as arguably the world leading technology for augmented reality.

‘Does Octopus Titan deserve its titan title? Certainly,’ says Alex Davies, chief executive of VCT broker Wealth Club. ‘Not only is it the biggest VCT, it has had numerous high-profile successes such as Secret Escapes, Swift Key, Graze and Tails.

‘With its investment in Zoopla it is also the first VCT to have spawned a billion-pound company. So far, its performance has been excellent and the team has been extremely shrewd in picking tomorrow’s winners – which at the time of investment is always far from obvious. There are caveats, however, and past performance is not a guide to the future. In addition, because Titan is now so big, it will require frequent and significant successes to generate mega returns for investors.’

AIM VCTS

Many individuals are drawn to AIM VCT because they are already familiar with stocks on London’s junior market. Unlike Generalist VCTs which are full of unquoted companies, AIM VCTs feature stocks which are more transparent in terms of corporate updates and their latest valuation.

Unicorn, Hargreave Hale, Octopus and Amati are among the asset managers with AIM VCTs, although not all of them are accepting applications for new investments at present.

David Stevenson at Amati says his firm often has an ongoing AIM VCT offer, such is the demand. However, investors may be disappointed to find its latest offer recently closed. ‘We only ever raise as much money as we feel comfortable investing over the next 12 to 18 months,’ he says.

Amati’s VCT portfolio includes Keywords Studios (KWS:AIM), a stock held since the computer game services group joined the stock market in 2013. Another holding is Water Intelligence (WATR:AIM), a leak detection business with a large opportunity in the US market. ‘It has a leading position in a strong growth market. It also has pricing power which you don’t often get with small companies,’ comments Stevenson.

Among the live offers, Hargreave Hale is seeking to raise up to £30m for its AIM VCT which targets a 5% annual dividend from a portfolio of 83 companies. The portfolio currently includes Learning Technologies (LTG:AIM), whose share price has gone up by 200% in the past year, and successful gambling sector technology provider Quixant (QXT:AIM).

LIMITED LIFE VCTS

Limited Life VCTs can be a suitable option for anyone who simply wants to take advantage of the tax benefits and have the lowest possible risks associated with how their money is invested via VCTs.

The fund managers’ goal is capital preservation, namely trying to ensure your investment doesn’t fall in value over a five-year period. Limited Life VCTs typically wind themselves up after five years to return cash to investors, hence why they are also sometimes known as Planned Exit VCTs.

One example is Puma VCT 13 which targets investments in companies that are expected to be revenue generating with limited external debt. One example of a current portfolio holding is Pure Cremation, a business which runs cremations without ceremonies.

‘This is an extremely disruptive company,’ says Puma’s Eliot Kaye, referring to how Pure Cremation is offering an alternative to a very traditional industry. Direct cremations will reach or exceed 10% of UK deaths by 2030, predicts Dignity Funerals. (DC)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Aston Martin and Funding Circle endure shaky starts after floating on the stock market

- Housebuilders hit by foreign buyers’ tax plan

- Time to sell Royal Mail shares as the once-attractive dividend looks unsustainable

- Ocado, Just Eat, Rightmove and others selected for new reliable growth’ list

- What Shurgard’s €2.4bn IPO means for UK self-storage plays

- Airline sector still in the danger zone as cost and operational pressures intensify