Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineTime is right for LoopUp’s remote meetings revolution

Now with the MeetingZone acquisition bolted on, remote meetings platform LoopUp (LOOP:AIM) has the scale to really make the most of what we believe is a significant growth opportunity. Revenue is expected to jump by 80%-plus over the next couple of years (from this year’s anticipated total of around £34m).

This should translate into soaring earnings that will effectively slash the price to earnings (PE) multiple to below 20, on a 2020 financial year view, from this year’s 60-plus rating.

LoopUp’s patented and cloud-based remote meetings software is designed to drag audio conferencing into the 21st Century. LoopUp’s key advantage is a streamlined service for both hosts and participants that not only works well but is intuitive and easy to use.

That makes its package attractive for corporate users versus rival services from deep pocketed rivals, such as Microsoft’s Skype for Business, Amazon Chime, Google Hangouts, AT&T plus more recent start-ups, such as GoToMeeting, JoinMe and the UK’s Powwownow.

LoopUp had in excess of 2,000 customers before it bought MeetingZone in a £61.4m deal earlier this year, and it is in the process of bringing on board those new clients to the core LoopUp platform.

IMPRESSIVE RETURN ON INVESTMENT

One of the most exciting data points is that for every £1.00 of one-off investment in its sales and distribution it reaps 75p back a year. Every year. Churn, the measure of customers leaving the service, is negligible and is entirely offset by upselling into existing clients.

Established operations in the UK and US are now being rapidly expanded via its local sales teams, or Pods. These are semi-autonomous units geared to hit ambitious growth targets, and incentivised as such.

Two of the nine Pods it currently runs were virtual start-ups that will take a few months to get up to speed. That explains while first half (to 30 June) organic revenue growth of 22% looked slow compared to previous periods.

And LoopUp hopes to use its now set-up Australia Pods as a launchpad into Asia in the future.

With revenues almost exclusively of a reliable, software-as-a-service, recurring nature, the company has a firm grip on future revenues. It also means that the LoopUp business model is naturally cash generative. More than 70% of earnings before interest, tax, depreciation and amortisation (EBITDA), adjusted for one-offs, are converted into operating cash flow. We would expect that percentage to improve further in time.

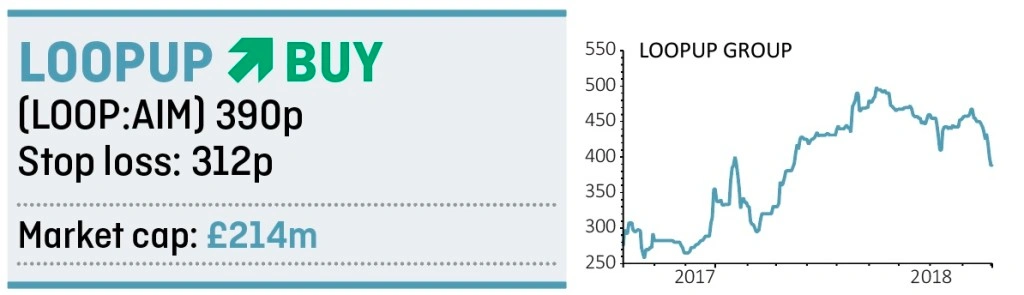

The stock has previously hit highs of 500p, after joining the market at 100p in August 2016, but analysts predict even better to come. The two brokers that cover the stock (Panmure Gordon and Numis) see the share price hitting 590p or 600p over the next 12 months or so, implying more than 50% upside. (SF)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Aston Martin and Funding Circle endure shaky starts after floating on the stock market

- Housebuilders hit by foreign buyers’ tax plan

- Time to sell Royal Mail shares as the once-attractive dividend looks unsustainable

- Ocado, Just Eat, Rightmove and others selected for new reliable growth’ list

- What Shurgard’s €2.4bn IPO means for UK self-storage plays

- Airline sector still in the danger zone as cost and operational pressures intensify