Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy investors must keep an eye on the Federal Reserve

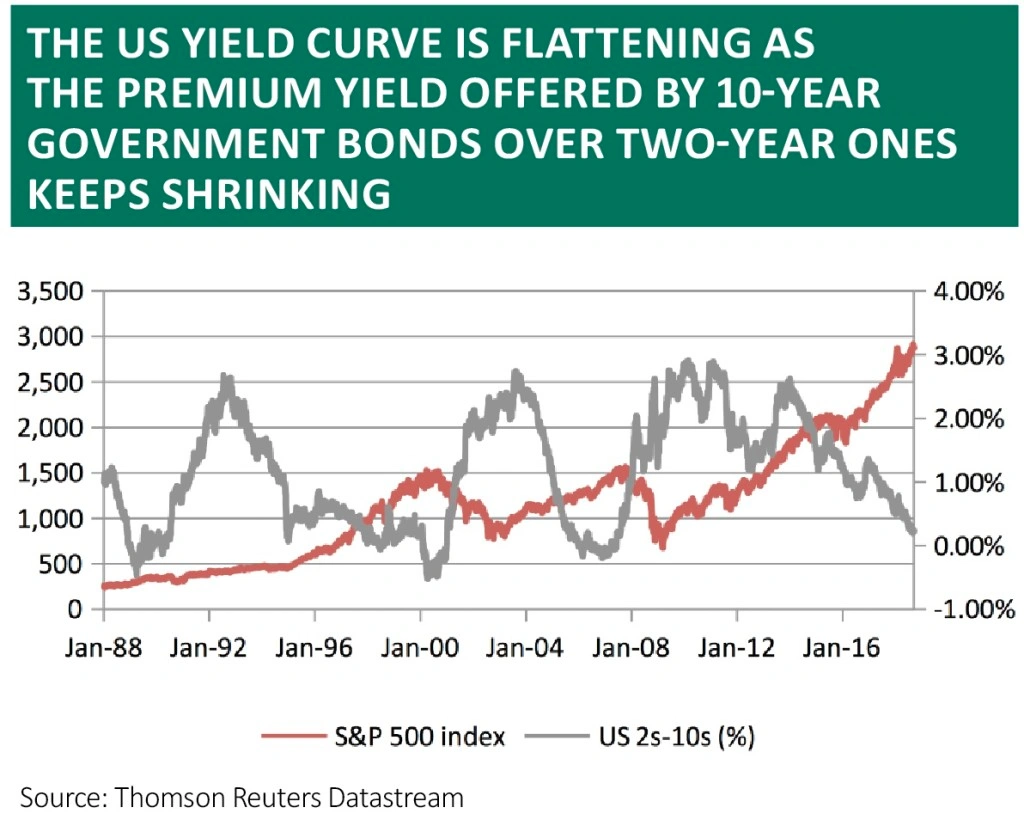

'The most expensive words in the English language are “this time it’s different”.’ This assertion from investor John Templeton has stood the test of time for a reason, so it is with a shiver that this column sees no less an institution than the US Federal Reserve arguing that the traditional measure of the yield curve should be ignored and a new one considered.

Instead of looking at the premium yield offered by 10-year Treasuries (US Government bonds) over a two-year period, the Fed is now saying we should look at the gap between the equivalent of 21-month Treasuries (three months plus six quarters ahead) and three-month Treasuries themselves.

This is very confusing, particularly as the average member of public cannot access information on 21-month Treasuries.

One possible explanation for this fudge is that the traditional yield curve is flagging danger. The new one is not.

The premium yield offered by 10-year Treasuries is just 0.22% (down to a 2007 low) and close to inverting, when the two-year yield is higher.

While there have been false signals, an inverted yield curve generally warns of economic and financial market trouble ahead and as we negotiate the tenth anniversary of the collapse of Lehman Brothers with markets at new all-time highs, it may be worth considering what could – eventually – end the multi-year bull market in most asset classes.

WAGES VERSUS WEALTH

We are overdue a correction of magnitude and this can be seen in how growth in US household income, in real terms, has been massively outstripped by growth in US household net worth.

The median US household income, in real terms, has just got back to the levels seen in 1999 and 2007 at around the $61,000 mark.

But US household net worth has just crossed the $100 trillion mark for the first time ever, a mark 50% higher than at the cyclical high of a decade ago.

The difference is likely to be accounted for by the surge in the value of financial and other assets – equities, bonds, property and frankly everything from vintage cars to art to wine to baseball cards – and this is one warning that at some stage another collapse in financial markets will sweep around the globe.

ASSET INFLATION

Surely household net worth cannot sustainably grow this much faster than incomes? The question then is what could trigger a correction in asset prices?

Lofty valuations and increased debt are both classic preconditions for any financial market calamity and they are in place, judging by the US household net worth figures and data from the Institute of International Finance which show global borrowing now massively exceeds the high of 2007.

That means one possible catalyst for disaster is a classic one – a policy error from a central bank and particularly the US Federal Reserve.

POLICY PICKLE

The US central bank is, in fairness, in a bit of a bind. Inflation is ticking up in the US, and frankly across developed markets (and that’s before asset price inflation is taken into account), so chair Jerome Powell and his team will want to nip this in the bud.

The US central bank will also want to normalise policy so it can build up some ammunition for the next downturn. The Fed has cut interest rates by an average of 5.25% since 1970 in response to recessions, once it has embarked upon a down-cycle in borrowing costs. It is hard to cut by that much when the headline Fed Funds rate is 2.00%.

But even a modest – and slow – increase in US borrowing costs, from 0.25% in November 2014, is starting to damage financial markets, especially now the US central bank is withdrawing quantitative easy (just as the European Central Bank is about to stop adding to it and even the Bank of Japan is being accused of stealth tapering).

Cryptocurrencies blew up first, followed by low-volatility strategies and then emerging markets – the currencies of Argentina, Turkey, Brazil, Indonesia and India, all among the world’s 25 largest economies, are at or near all-time lows against the dollar, which is responding to tighter policy in the US.

The Fed seems determined to press ahead with rate hikes and the danger is that they overdo it – this is one explanation for why the yield curve is so flat, with US 10-year Treasuries yielding only 0.22% more than two-year paper.

The flattening curve means investors seem to believe that while the Fed is keen to drive rates up now it will have to recant and cut sharply later.

That in turn could be why the Fed does not want markets to listen to it. Watch out for any discussion of this issue when Jerome Powell delivers the next interest rate decision on 26 September.

Policy error in the Marriner S. Eccles building in Washington therefore remains a key risk, especially as Fed officials are now peddling the line of ‘it’s different this time’. It is not for nothing that German economist Rudi Dornbusch once noted: ‘No post-war recovery has died in bed of old age – the Federal Reserve has murdered every one of them’.

By Russ Mould, investment director, AJ Bell

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.