Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineMining sector down nearly 13% this year on multiple headwinds

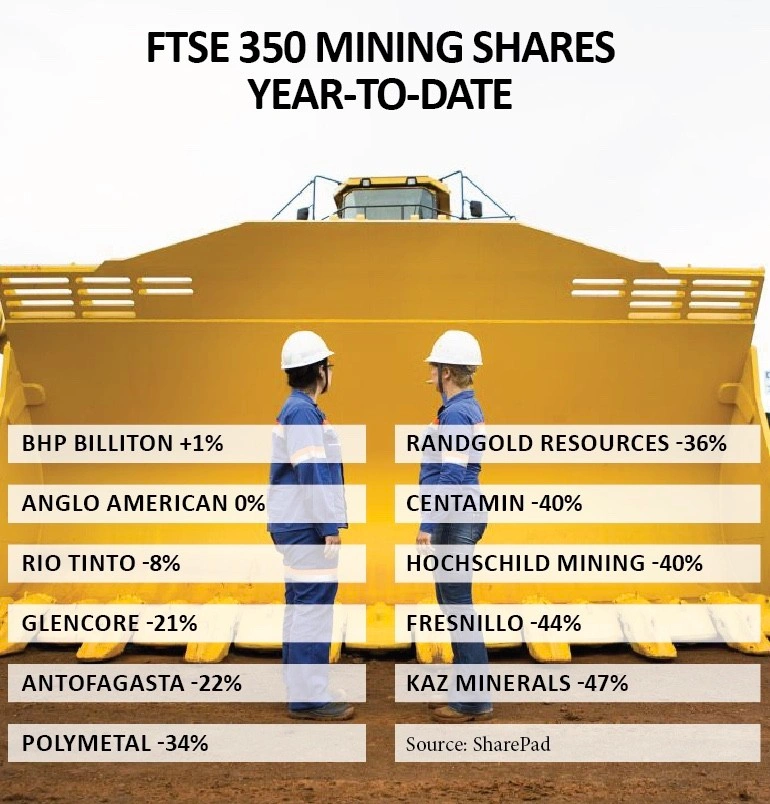

The FTSE 350 mining sector has disappointed investors this year, down 12.7% in value.

Most companies should have been in better financial and operational shape, having streamlined over the past five years following the previous commodities crash. Unfortunately a multitude of factors have weighed on share price performance.

The escalating trade war between the US and China has been a major factor as investors fear that Chinese commodities demand will be hit. Exacerbating the situation has been tighter credit in China acting as another headwind for commodities demand.

The Chinese government recently appears to be more accommodative around monetary policy such as providing liquidity for inter-bank lending, although there are no signs of ‘stimulus flood gates opening’, says Liberum analyst Ben Davis.

He says it is difficult to be negative on diversified FTSE 100 miners such as Glencore (GLEN) and Rio Tinto (RIO) because of momentum in the Chinese property development market.

‘However we could be in a very different position by the end of the year if the Chinese government have not pushed on the monetary stimulus accelerator pedal.’ He fears that property developers will be left with excess inventory if the current cycle runs out of steam.

Some mining stocks have suffered because of company-specific issues. Kazakhstan-based copper miner Kaz Minerals (KAZ) is down 47% year-to-date in part caused by negative reaction to a $900m deal to buy a Russian copper project. Analysts questioned the logic, saying it requires high capital expenditure and is located in a very difficult place to work because of extreme cold temperatures.

Precious metal miners Fresnillo (FRES) and Centamin (CEY) has suffered from operational issues. Randgold Resources (RRS) has battled resource nationalism issues; and Glencore has been engaged in a court battle.

Rio Tinto and BHP Billiton (BLT) are either sitting on, or are about to receive, a lot of cash generated from operations and asset sales. There is limited appetite to do large deals in the mining sector at present, so this cash is ultimately being used to fund dividends and share buybacks.

Shares in Anglo American (AAL) have outperformed the sector, albeit they are only flat year-to-date. It has been linked with potential carve-out interest from 19.35% shareholder Volcan. (DC)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.