Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineBakk-it or Bakk-off? Should you invest in hummus and pizza seller Bakkavor?

Having joined the stock market at 180p in November 2017, shares in food group Bakkavor (BAKK) have since drifted down to 164p.

One possible explanation is a negative read-across from quoted peer Greencore (GNC) which has had mixed fortunes with its UK and US expansion.

Also weighing on the share price are tough market conditions, concerns about input cost volatility and the supply chain post Brexit, not to mention a share overhang with investors factoring in potential divestments by 25% shareholder Baupost.

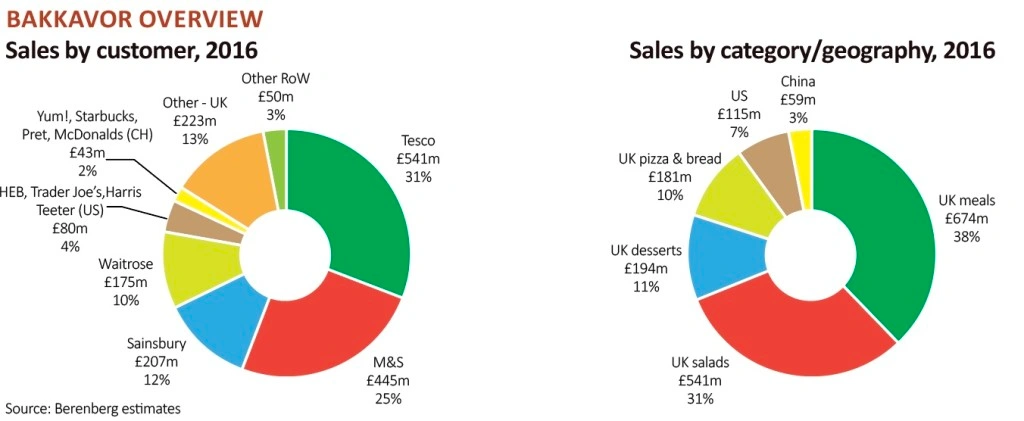

While this is a murky situation, it is still worth exploring how Bakkavor makes money, given it is a member of the prestigious FTSE 250 index.

WHAT DOES BAKKAVOR DO?

Bakkavor is the leading provider in the large, fast-growing UK fresh prepared food market, being driven by structural trends towards convenience, and is a business focused on building long-term sustainable growth in the UK, US and China.

Competitive strengths include strong capabilities in salads, ready meals, pizza and desserts. Bakkavor also caters to the more affluent dinner party set through products such as hummus, dips and artisan breads. Sustainable competitive advantage stems from Bakkavor’s sheer scale and close partnerships with customers.

Focusing on retailers’ own label brands, Bakkavor has dominant supply positions with key customers including Tesco (TSCO), Marks & Spencer (MKS), J Sainsbury (SBRY) and Waitrose, while also supplying WM Morrison (MRW), Asda, Aldi and Co-Op.

It has early-stage convenience food operations in China and the US, supplying retail and foodservice customers with everything from sandwiches and burritos to ready meals.

Significantly from a growth investor’s perspective, sales volumes are growing with all key overseas customers due to new store openings and the introduction of new ranges.

Adjusted EBITDA margin has been rising since 2014 and management see their charge growing sales in line with the 4-5% category growth rate with modest margin gains, although raw material cost inflation represents a margin headwind.

THE BAKKAVOR BACK STORY

Bakkavor is 50%-owned by Lydur and Agust Gudmundsson, who founded the business in Iceland in 1986 as a fish products manufacturer and exporter.

The business grew aggressively during the 2000s, riding the wave of a credit boom that blew up quite messily. Given its historical issues with debt, deleveraging has been a priority for management ever since Bakkavor delisted from the Icelandic stock exchange in 2009 and converted into a private limited company.

From 2010 onwards, Bakkavor began exiting low margin businesses and low growth geographies, then simplified its corporate structure with a new parent company domiciled in the UK in 2012.

In 2016, Baupost, the Boston-based hedge fund run by renowned value investor Seth Klarman, became a significant shareholder with a €163m investment for a 40% equity stake. As part of this process and the preparation for an IPO, mainly to allow Baupost an exit, Bakkavor refinanced its bank facilities and high yield bonds in March 2017.

TASTY TRENDS

The UK is Bakkavor’s biggest market at 90% of total turnover and here, thanks to scale and operational leverage, it makes an EBITDA margin of 9.1%. Bakkavor is geared into the consumers’ quest for fresh, healthy and convenient chilled foods, although retail price inflation and subdued consumer demand are material headwinds.

International represents a potentially huge growth opportunity for Bakkavor, although it only accounts for 10% of group sales at present.

Margins in the overseas business, where customers span Costa, Starbucks, KFC, Pizza Hut and McDonald’s, have scope to move higher on fixed cost leverage as volumes grow.

Bakkavor is undertaking an ambitious investment drive to expand its capacity and capabilities overseas – investing in a new factory for a key customer (HEB) in Texas and with a new state of the art factory in East China set to become operational in the fourth quarter of the year – although such expansion carries execution risk and returns are unlikely before 2020.

The latest half year results were solid rather than spectacular, showing sales up 0.8% to £910.4m, with like-for-like revenue edging 2.8% higher to £910.1m and pre-tax profit rising 38.9% to £47.1m.

We note with interest the 7.3% rise in free cash flow to £32.4m and a reduction in net debt from £368.2m to £269.8m, as well as signs of sales momentum building into the second half, although management’s caution about input cost volatility proved a trigger for modest downgrades to outer year estimates.

Drawing confidence from its strengthening balance sheet, Bakkavor has made its first UK acquisition in a decade, snapping up sweet bakery goods producer Haydens Bakery from bombed-out Real Good Food (RGD:AIM) for £12m.

The deal increases the breadth and depth of Bakkavor’s desserts range and management plans to grow sales and move Haydens from a break-even position into profit.

On the downside for the group as a whole, any sustained increase in labour costs, labour shortages post-Brexit or raw material input costs could materially affect margins. Furthermore, the bulk of Bakkavor’s outlook is still tied to its top four customers.

TASTY VALUE MORSEL OR SWEET TREAT?

Investment bank Berenberg forecasts a near-doubling of adjusted pre-tax profit from £56m to £102m this year, ahead of £110m in 2019 and £121m in 2020.

On these estimates, Bakkavor swaps hands for 11.3 times estimated 2018 earnings, which looks fair value given the uncertainties that hang over the business.

While there is reasonable earnings growth potential and a prospective 3.9% dividend yield, we’re concerned about rising food prices near-term and believe the shares could get a lot cheaper. That said, this is definitely one to watch should the valuation become more appealing. (JC)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.