Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineBrexit: six months until D-Day

As the UK prepares to leave the EU on 29 March 2019 at 11pm, there are many questions left unanswered for investors, businesses and the general public.

Stock markets in recent months haven’t been troubled too much by the Brexit negotiations as investors have had plenty of other distractions such as the US/China trade war and volatility in emerging markets. The situation may soon change given we’re now six months away from the big day of separation.

The type of exit from the economic block is still unclear with political infighting dominating the agenda. And while it is impossible to predict the precise impact on investors’ portfolios, it is worth understanding the different scenarios and how they may affect markets, economics and currencies.

A transition period is scheduled to begin on 29 March 2019, lasting to 31 December 2020, to let businesses and individuals prepare for the time when the new post-Brexit rules between the UK and EU begin.

Free movement will continue during the transition period and the UK can strike trade deals, although they won’t be able to come into force until 1 January 2021. But failure to strike a withdrawal agreement by the deadline next March would scupper this transition period, hence why a ‘no deal’ outcome could spook the stock market.

UNDERSTANDING THE DIFFERENT SCENARIOS

SOFT BREXIT

This type of withdrawal from the EU should appease large swathes

of the population who voted to remain and has been dubbed BRINO (Brexit in Name Only). In this scenario, the UK would remain part of the customs union in a similar fashion to Norway’s model.

A customs union sees EU member states all charge the same import duties to countries outside the EU. Member states can trade freely with each other, without customs checks at borders. In contrast, a free trade area charges no tariffs, taxes or quotas on good and services moving within the area but members are free to strike their own external trade deals.

Both Prime Minister Theresa May and Labour leader Jeremy Corbyn have ruled out staying in a single market. May has also said the UK will not remain in the customs union as it prevents Britain negotiating free trade agreements with other countries. It would mean every single lorry going from the UK to the EU would face mandatory customs checks.

Mark Ward, head of trading at investment firm Sanlam, implies that a soft Brexit would limit a sharp drop in the stock market as it would essentially mean little change to the current system. However, after the Government released its white paper dubbed the Chequers Accord, the political mood has changed somewhat.

HARD BREXIT (WITH AGREEMENT ON GOODS AND SERVICES)

In this situation, the UK would no longer be a member of the single market or customs union. Instead, it would come to an agreement that maintains the flow of goods and services similar to Canada’s Comprehensive Economic Trade Agreement with the EU.

This would still be disruptive as flows of goods would no longer

be as free, causing supply chain disruption. In reality this would probably depress sterling’s value and may soften the UK economy.

However, it would not be a disaster for equities and has been priced in to some extent. Paul Jackson, head of multi-asset research at Invesco Powershares, gives this outcome a 30% probability.

HARD BREXIT (WITH AGREEMENT ON GOODS ONLY)

In this situation, the UK would be able to trade with the EU in goods pretty much as now but not in services. The UK Government seems to think this would be a good outcome but the service industry would suffer which is bad as it accounts for about three quarters of the UK economy.

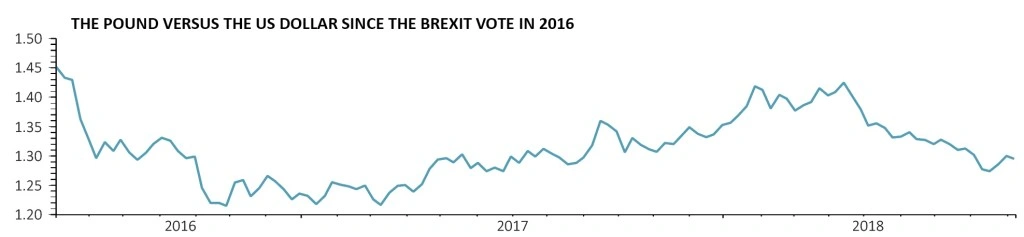

Sterling would more than likely suffer in this situation, possibly pushing the pound/dollar exchange rate down to $1.20 (versus $1.30 at the time of writing) with the potential for a recession.

The services sector is very important, particularly as many companies which provide goods also provides associated services such as Rolls-Royce (RR.) which derives a large chunk of profit from engine maintenance.

The range of service companies is very broad and includes transport, communication firms, banks, hotels and restaurants. They are widely represented by well-known firms on the UK stock market, meaning any setback to the service industry as a whole could negatively impact investors.

NO DEAL

A no-deal result would mean the UK’s relationship with the EU would be conducted via World Trade Organisation rules. Given the increase in tariffs, inflation would probably rise and a recession could happen as it would be more costly to trade goods with many overseas partners.

Growth could be boosted in the long term when new trade deals are struck although there are currently no concrete plans in place. Shares in UK domestic companies may suffer compared to global indices as sterling would most certainly tumble.

Philip Smeaton, chief investment officer at Sanlam, says since the Government released its Brexit white paper the market is certainly pricing in a no-deal outcome.

While this may seem a potential disaster, Smeaton comments: ‘Even a “no deal” provides clarity and something you’re working with and you know whatever happens afterwards will be an improvement.’

That’s being optimistic. In reality the Government would have to rethink its spending plans which could have major repercussions. Various think-tank research papers have also suggested food prices could go up and we could see some shortages of goods, but this may only be a temporary phenomenon.

From an investment perspective, we believe the stock market could experience a short period of volatility upon a no-deal outcome which

could prove to be a good time to go bargain hunting for stocks.

NO BREXIT (REMAIN IN THE EU)

We think a ‘no Brexit’ outcome is highly unlikely despite continued calls for a second referendum from various camps. These include GMB, one of Britain’s biggest unions, and Superdry (SDRY)

co-founder Julian Dunkerton who recently gave £1m to the People’s Vote campaign for a referendum on the final Brexit deal.

OTHER POINTS TO CONSIDER

WHAT’S HAPPENED TO THE UK ECONOMY SINCE THE BREXIT VOTE?

The British economy has disappointed since the referendum vote two years ago as businesses have become more cautious with spending and consumers have battled with rising inflation.

In 2017, the savings ratio — measuring the proportion of UK household income that is not spent — dropped to 4.1%, its lowest rate for more than 50 years.

Economic growth slowed in 2017 and started 2018 poorly due to snow disruption. Figures now show an improvement as the year progresses, helped by good weather over the summer. The latest figures show 0.6% growth for the three months to July.

Ultimately the UK economy has been sluggish but the performance hasn’t been disastrous and unemployment rates are low.

Yet investment bank UBS believes UK GDP is already 2.1% lower than where it would have been without Brexit. ‘Investment is 4% weaker, inflation 1.5% higher, consumption is 1.7% lower and the REER (real effective exchange rate) is 12% more depreciated,’ it says.

‘To put 2.1% cumulative decline in real growth in context, that’s roughly a quarter to a third of the total Brexit costs estimated in the most pessimistic assessments done prior to the EU referendum (eg. HM Treasury, OECD) and almost equal to the full costs of some of the more optimistic assessments. But the UK has not even left the EU yet!

‘Why is it going largely unnoticed? Because the global economy started to accelerate strongly right after the mid-16 referendum, allowing UK GDP growth to move sideways rather than dive lower,’ explains UBS’s economists. ‘Without Brexit, however, we think UK GDP could have been 100 basis points per year higher.’

The key point to now consider is whether companies get even more jumpy as the Brexit deadline approaches. We believe it is plausible that companies could scale back employment and investment decisions unless there is firm progress with the talks between the UK and EU.

‘The UK Treasury estimated that UK GDP might fall by 3.6% to 6% over two years in a ‘cliff-edge’ Brexit. This probably an underestimate – failing to account for the legal/regulatory basis for

EU/UK trade suddenly being eliminated,’ says Conall MacCoille, chief economist at stockbroker Davy. ‘We illustrate a hard Brexit scenario where UK GDP falls by 4% in 2019 and 2% in 2020.’

MacCoille believes a cliff-edge Brexit is a low probability event. In July, UBS strategist John Wraith says recent developments make a no-deal outcome more, not less, likely.

ISSUES FACING QUOTED COMPANIES

Tim Ward, chief executive of the Quoted Company Alliance (QCA), has been talking to small companies who are concerned with recruiting. Without the free movement of people, this limits the potential pool of talent available to UK nationals.

This is a key point of contention in the whole Brexit debate and yet again one that is unclear. However, Sajid Javid, home secretary, has said that free movement of people will end, with no automatic right for anyone from the EU to come to the UK and work. Others in Government have said the UK will offer work visas to EU nationals for UK employment.

Ward of the QCA says companies he’s surveyed are finding it hard to retain and attract talent given the uncertainty surrounding the status of workers after 29 March 2019.

There are numerous sectors in the UK which employ large amounts of people, many of whom have come from abroad to seek work. For example, the construction, retail and services sectors could be significantly affected if this pool of workers shrinks.

From another perspective, many UK companies with large operations across multiple countries should be able to adapt to the Brexit landscape, particularly if they need to operate across the EU.

For example, EasyJet (EZJ) has been making preparations for a new base in Austria as airlines must have an air operator certificate in an EU member country to allow it to continue flying between member states after Brexit.

HSBC (HSBA) has shifted ownership of its Polish and Irish subsidiaries from its London-based entity to its French unit, and plans to do the same for seven more European branches, as it prepares for Brexit.

And asset manager Ashmore (ASHM) is setting up an office in Ireland to ensure continued access to EU-based institutional clients.

CORPORATE SPENDING: WAITING FOR BREXIT CLARITY

While some companies can make contingency plans, there is still plenty of evidence that businesses are delaying investment spending until there is clarity over how Brexit will play out. After all, why make a decision now when you can wait a short time and know what’s going on?

Consultancy Vendigital says since the referendum vote in 2016, businesses have invested £22bn less than they would have done based on pre-Brexit trends.

UK business investment grew at a mere 1.6% in 2017. And a survey of finance directors by Deloitte covering the second quarter of 2018 found that just 15% of UK CFOs expected to increase capital expenditure.

‘The April 2018 pan-European Deloitte CFO survey revealed that UK CFOs are the most pessimistic and risk averse across 20 countries surveyed,’ comments Conall MacCoille at stockbroker Davy.

Even the recent UK Government note to financial service firms warning them to prepare for a no-deal has not really quelled fears as much as was clearly intended.

Andrew Pilgrim, government financial services leader at accountant EY, comments: ‘While this paper reiterates that the UK Government is doing all it can to maintain continuity in that scenario [no deal], there is a limit to what they can promise unilaterally. Whether there would be similar flexibility from the EU is likely to remain unclear for some time. Until then uncertainty remains the word of the moment.’

CHALLENGES AROUND THE WORLD... NOT JUST THE UK

It’s a truism that one thing markets hate is uncertainty and given the transition period following Brexit it may be some time until we

know the true lay of the land.

Invesco’s Paul Jackson says: ‘It has to be remembered that the UK has yet to leave the EU and has yet to agree on what terms it will do so. Hence, we expect a renewed build-up of uncertainty, which could eventually lead to a decline in investment spending and potentially recession.’

One thing is perhaps certain, in a global context Brexit may not rank as highly as those in Europe and especially Britain think.

US President Donald Trump’s trade war rhetoric has being spooking the markets much more than the details of the manner in which the UK exits the EU. A trade war between the US and China has far more repercussions for the global economy than a member of an economic block leaving after its citizens voted to do so in a democratic process.

Mike Coop, head of multi asset portfolio management EMEA at Morningstar, says many UK investors are focused on Brexit but they forget that other areas of the world have uncertain macro issues.

‘For example, there are trade policy concerns in the US; Continental Europe has its own challenges, such as dealing with fiscal policy

and the immigration crisis; and China is managing a large debt cycle. You need to view Brexit in the broader context of what else is happening in the world.’

He concludes: ‘There will be a material change in how the UK trades with Europe and the impact on profitability could be significant from Brexit, but less so than people think.’

The takeaway for investors is not to panic and try to second guess what will happen with Brexit. There is going to be a considerable amount of noise over the next six months and you shouldn’t make knee-jerk reactions to your portfolio as events unfold with the Brexit negotiations.

Ultimately it is imperative you have a diversified portfolio which provides coverage to lots of different parts of the world and not heavily concentrated on the UK and only on a handful of companies.

Make sure you also have cash to hand should there be a sharp decline in the stock market in the run-up to the March 2019 Brexit deadline, so you can pick up bargains if there is a big share sell-off. (DS/DC)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Investors braced for potential dilutive equity fundraise from Sirius Minerals

- Will Unilever exit the FTSE 100?

- Second worst September start for US tech stocks in 10 years

- Are UK markets finally ready to shed their Brexit discount?

- Share price decline implies Debenhams is at death’s door

- Is this the beginning of the end for Whitbread?