Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThis is not the time to turn your back on technology stocks

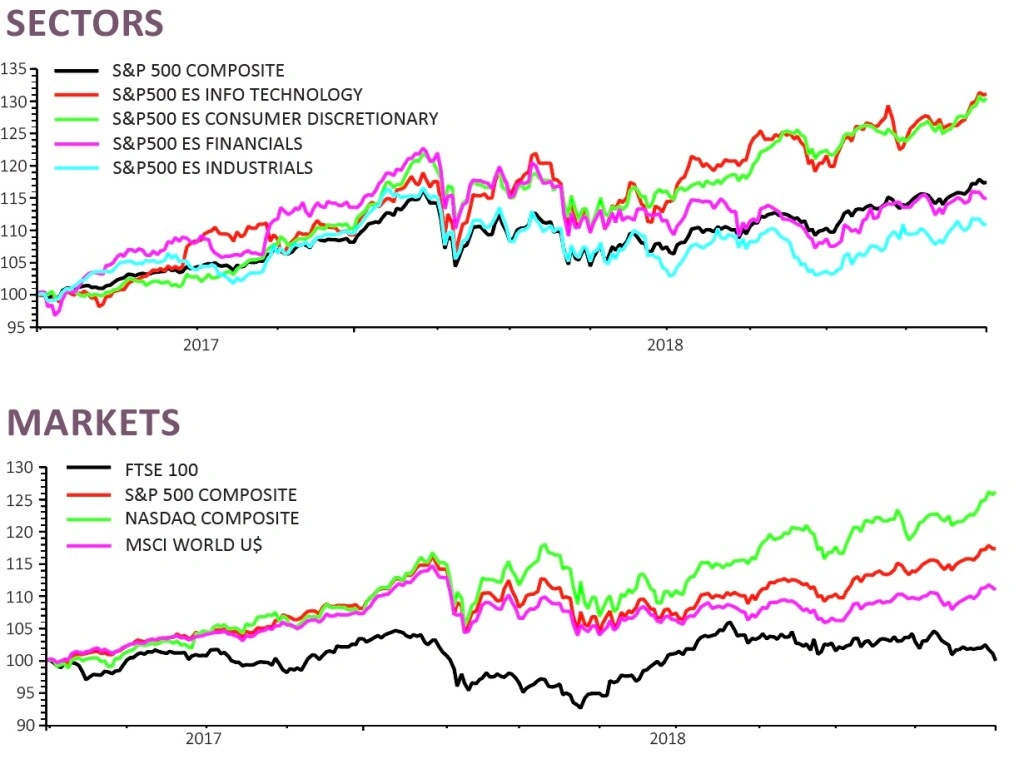

On 29 August the Nasdaq composite, led by popular technology FANG stocks (Facebook, Amazon, Netflix and Google – officially called Alphabet) set a new record high, closing at 8,109.69. Year to date the index is up 15.7% compared to a 7.6% gain for the wider S&P 500.

Add Apple and Microsoft to the FANG gang (their relative size and influence demands we do), those six stocks have chalked-up an average 38% share price return in 2018, and notably that encompasses a 2% decline for Facebook. No wonder talk of a tech bubble has returned and people are wondering if the space is overvalued.

‘The most common question I get asked as an analyst is whether we are heading for another crash like that in 2000,’ says Richard Holway, a long respected technology analyst and founder of the website TechMarketView.

Recent reports of hedge fund rotation out of the technology space and growing short positions in popular tech stocks have helped fuel these concerns.

The biggest concern for investors is valuation. Market darling Advanced Micro Devices (AMD) is this year’s best performing Nasdaq share, up 128% this year leaving it on a 2018 price to earnings (PE) multiple of 47.2. There are other stocks on even higher ratings.

So it is interesting to find that Alphabet, Facebook and Microsoft all trade on PEs of less than 30, while Apple’s next 12 months ratio is 16.6, according to Reuters’ data.

‘At the end of July 2018, Microsoft was the third largest constituent of the MSCI All Countries World Growth Index and the fifth largest in the equivalent Value Index, whilst at one stage last year Apple topped both the MSCI Growth and Value Indices,’ says Peter Askew, chief executive officer of Nottingham-based fund management boutique T Baile Asset Management.

PARTY, BUT IT’S NOT LIKE 1999

Multiple reasons stand between the tech bubble of 1999/2000 and now. Today’s companies are (largely) hugely profitable with enormous cash-supported balance sheets and many revenues lines.

But perhaps the biggest single difference is how technology is now embraced and used, permeating every industry sector and the everyday lives of ordinary people. Back in 2000 most businesses could operate quite happily without the internet, emails or smartphones.

What technology investment experts believe is evident is that earnings growth is providing ample support for rising share prices. ‘Higher valuations largely reflect a strengthening US economy, improved technology fundamentals and robust corporate earnings,’ says Ben Rogoff, manager of Polar Capital Technology Trust (PCT),

‘I still like tech,’ says Lars Kreckel, an equity strategist at Legal & General Investment Management. ‘Alphabet and Amazon delivered another set of expectation beating quarterly results,’ he says, even if Facebook, for the second time this year crashed the party after warning of slowing earnings growth in July.

‘The market reaction to Facebook’s results has been a useful reminder that the sector is not invincible,’ says Kreckel after more than 20% was wiped off the social media platform share price.

Walter Price, manager of Allianz Technology Trust (ATT), drew attention to Apple, whose second quarter results were better than expected. ‘The real surprise for us was the services business, particularly iTunes and iCloud which both grew ahead of expectations,’ Price says.

‘We saw that the cloud computing theme continues to expand, with providers generally meeting or exceeding market expectations,’ says Price.

A FEW GOOD STOCKS

This has led to claims of polarisation of stock performance, with a relatively small number of strong performing share prices driving the lion’s share of stock market returns. The S&P 500’s five largest companies (all tech firms; Apple, Alphabet, Microsoft, Amazon, Facebook) are worth 16% of the entire index.

This some experts believe is often a warning signs of an over-inflated stock market. Yet there would seems to be some inevitability about this when fund managers are often focusing on buying only the biggest and best in class within a niche industry or market.

‘History shows that stock market returns are driven by a small group of big winners and it is the job of the investment manager to identify such companies and then invest in them with conviction,’ that’s how James Anderson and Tom Slater see it.

They run the Scottish Mortgage Trust (SMT), one of the UK’s most popular investment trusts, and while not strictly a tech fund, its focus on long-term growth opportunities means many of the FANG+AM stocks sit in the portfolio – Amazon is its biggest holding and is worth 10.2% of its invested funds.

Polar Capital Technology’s Rogoff points out digital transformation and public cloud stocks such as Twillio, RingCentral, Five9, Ansys, Cognex, GrubHub ‘all reporting strong quarters,’ which helps illustrate the broader spread of performance than many investors may realise.

The technology sector’s price to earnings multiple expansion may be running out of steam, believes Rogoff, yet this could be a positive for share prices as investor turn their attention on the underlying superiority of earnings within the sector.

This could mean a narrower group of winners drive strong returns, bringing us back to the polarising effects potentially at play on global stock performance.

‘If we are correct, this should continue to favour our growth-centric investment approach,’ believes Rogoff.

‘That’s not to say that a correction won’t happen,’ points out Richard Holway, but ‘I think that it’s the global economy as a whole that runs the greatest risk - it is not tech specific.’ (SF)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.