Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineCan shares in tobacco companies fight back after a torrid time?

Once considered defensive investments and dependable sources of income, tobacco stocks have recently gone through a troublesome period and experienced significant share price declines.

Cigarette companies were long-prized for their strong brands, pricing power, high margins and strong returns on capital, a function of the fact smokers are addicted and willing to stump up premium prices for their brands.

Yet shares in the London-listed British American Tobacco (BATS) and Imperial Brands (IMB) have de-rated on fears over declining cigarette volumes, the economics of so-called Next Generation Products (NGPs) and the implementation of a nicotine standard across the pond.

Increased health awareness, decreasing social acceptance of smoking and legal and regulatory changes, including the introduction of plain packaging in numerous countries, have steadily reduced volumes.

Also weighing on sentiment is the fact tobacco stocks are considered ‘bond proxies’ and have sold off amid rising government bond yields.

THE BULL AND BEAR CASE

Bulls insist the industry is transforming which should enable it to become less controversial and enjoy a higher rate of sustained sales growth.

Bears argue that next generation products are beginning to cannibalise the profitable combustible tobacco business.

HOW ARE CIGARETTE COMPANIES FIGHTING BACK?

In reaction, ‘big tobacco’ is aggressively investing in NGPs, which bears argue are beginning to cannibalise the profitable combustible tobacco business.

Put simply, the epochal shift from conventional cigarettes to NGPs is driving the biggest changes this sector has seen in living memory.

Yet many well-followed portfolio managers are sticking with the London-listed duo. Neil Woodford holds Imperial Brands and BAT (British American Tobacco) in his LF Woodford Income Focus Fund (BD9X6D5).

Mark Barnett holds both stocks in Edinburgh Investment Trust (EDIN) and BAT is a leading holding in the Michael Clark-managed Fidelity MoneyBuilder Dividend Fund (B3LNGT9).

The pair also features in the Colin Morton-managed Franklin UK Equity Income (B7DRD63) and Franklin UK Rising Dividends (B5MJ560) funds, while BAT is a long position in the Nick Osborne-steered BlackRock UK Absolute Alpha (B5ZNQ99) fund.

We’re taking the view that all the bad news is fully priced into the two UK-listed tobacco stocks and that now could be a good time to buy the shares.

GOING UP IN SMOKE?

Investor sentiment towards the sector is cautious to say the least. ‘The market doesn’t like the uncertainty the introduction of NGPs has presented and the increased regulatory oversight from the FDA (US Food & Drug Administration),’ explains BlackRock’s Osborne.

This is on top of illicit trade – a perennial industry headache – and rising regulation in developed markets, all factors behind steady volume declines as population growth remains muted and smoking prevalence continues to fall.

Emerging markets remain promising due to fast population growth, increasing disposable incomes and less-stringent regulatory environments.

Yet even some emerging markets are becoming more aggressive in their tax treatment of cigarettes; recent major tax hikes have been pushed through everywhere from Russia and Brazil to Saudi Arabia, Indonesia and the Philippines.

Last summer, the FDA announced it would move to ‘harm reduction’ as the basis for regulating the US market and look at the feasibility of reducing nicotine to non-addictive levels in US cigarettes, potentially going far beyond previous attempts to reduce tar and nicotine levels.

CHANGING FOR THE BETTER?

Bulls insist the industry is at the start of a long transformation, one that should enable it to become less controversial and enjoy a higher rate of sustained sales growth.

The shift to NGPs is sure to be slow, with many hopelessly addicted consumers likely to remain cigarette smokers long into the future.

There is also evidence that public smoking bans and declining affordability are the major causes of volume decline, rather than a dramatic shift in societal attitudes.

CONSUMPTION TRENDS

Berenberg analyst Jonathan Leinster points out demand for nicotine is actually rising, and not declining.

‘In our study of 12 major markets, the number of smokers of conventional cigarettes (aka factory manufactured cigarettes or FMC) has declined by about 1% per annum over 2010-18, but the total number of users of vaping, FMC and heated tobacco combined has risen over the same period,’ he explains.

‘This may be double counting dual-users who both vape and smoke, but even if we assume 50% of vapers are dual-users then the total number of consumers is flat over 2010-18.

‘Retail sales of FMC, in US dollar terms, rose 1% per annum over 2010-18 in these markets and rose 2.4% per annum for the combined categories.

‘This does not take into account the rising number in volumes of oral tobacco and cigars in the US. Overall, the demand for nicotine is rising and consumers are spending more. The issue for the industry is that governments have become increasingly aggressive at maximising tax revenues and taking a larger share of the gross revenues.’

Tobacco titans are tackling the threat head on by creating NGPs they can demonstrate are less harmful to consumers.

Their strategy is based on the fact regulators broadly accept ‘harm reduction’ as a regulatory framework as this implies a greater ability to innovate and market products that are less damaging to health and critically, for a differentiated tax system for them. Bulls believe NGP can and will be profitable, among them the Berenberg analyst.

Leinster believes investor concerns about the future profitability of NGP markets are overdone, the focus on margins misplaced and worries about new entrants ignores the opportunity ‘big tobacco’ will have against smaller national players and illicit trade.

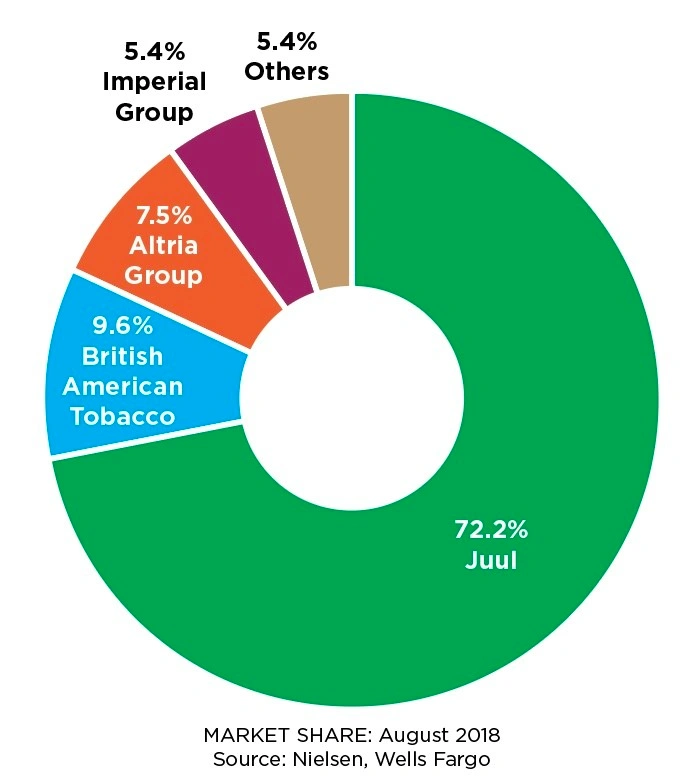

Big tobacco has already developed products that have gained widespread consumer acceptability in both vaping and heated tobacco, notably Philip Morris International’s iQOS product, BAT’s Glo device and JUUL.

COMPELLING ECONOMICS

Liberum Capital argues that both BAT and Imperial Brands trade at the widest discount to the Consumer Staples sector in over 15 years despite their improving prospects.

‘Shares are so depressed that we believe the market is discounting a nicotine standard far earlier than the FDA can reasonably deliver,’ thunders Liberum. ‘Our base case assumes the US nicotine standard comes in 2023. We see significant upside on conservative assumptions.’

For those unfamiliar with the sector, it is worth re-stating the compelling economics of the major international tobacco manufacturers, which remain intact, for now.

‘There are few (if any) low-ticket “must-have” consumable products that one billion people desire on a repeat basis at the same scale and pricing power as tobacco,’ says Liberum.

‘Cigarettes are cheap to produce at scale and travel well. Tobacco growers and distributors have weak bargaining power.

‘Tobacco companies’ attractive positions are further entrenched by advertising bans, which makes it difficult for new entrants to steal share. This industry structure and the addictive nature of the product create a highly favourable pricing and margin structure for manufacturers.’

A further strength is that the cigarette industry is highly consolidated. Stripping out China, India and the US, 84% of the global market is spoken for by four players – PMI, BAT, Japan Tobacco and Imperial Brands.

While the consolidated structure of global tobacco makes it more difficult to get regulatory approval for further mergers & acquisitions (M&A), it also means there are fewer price wars among legal competitors, a trait that supports high profit margins.

Bear in mind that cigarettes are a $683bn global market – that is the retail value based on the 5.5trn cigarettes the tobacco industry sold in 2016.

THE LOWDOWN ON NEXT GENERATION PRODUCTS

The burgeoning band of less harmful NGPs include tobacco heating products (THP), also known as heat-not-burn (HNB), an important category for tobacco giants as they are sold at a higher gross margin than conventional cigarettes.

THPs have done well in Japan, where PMI’s IQOS heatstick dominates, while BAT’s glo heatstick is in 13 international markets.

NGPs also include electronic cigarettes (e-cigarettes), nicotine delivery systems that use electricity to create a nicotine vapour (they include cigalikes, vape pens, mods and pod-based systems including JUUL and Imperial Brands’ myBlu and Altria’s CYNC).

Walk down any high street and (irritatingly if you are a non-smoker), your face will probably encounter a plume of vapour.

BAT believes the vapour category size is £9bn, with approximately 55m consumers currently ‘vaping’. This means the market is equivalent to cameras or smart watches and is twice the size of cognac or low/no alcohol beer.

By 2020, the vapour market is expected to be larger than the men’s shaving market, with vaping proving especially popular among more health-conscious youths.

During late 2018 and early 2019, BAT is looking to make significant further launches in vaping.

Both Imperial Brands and Japan Tobacco believe that vaping will emerge as the major nicotine format long-term for the bulk of consumers – Imperial’s main vaping brand is Blu, while Japan Tobacco’s is Logic – although both are developing heated tobacco products in response to the success of iQOS in Japan and South Korea.

BlackRock’s Nick Osborne says the economics of NGPs versus combustibles looks good, ‘so the aggregate profit pool isn’t changed and existing players take the vast majority of that market – so far, so good for the traditional industry’.

However, he warns there is one area where NGPs appear to be more disruptive and that is vaping, where there is much more fragmentation across the market and in the US particular where the introduction of JUUL’s product appears to be taking considerable share.

LARGE MARKET

More than 1bn people smoke globally. That is roughly 15% of the global population or 20% of the world’s adults.

According to Euromonitor, the fastest growing tobacco markets by retail sales are China, Russia, Indonesia, Turkey, Argentina, South Korea, Egypt and Iran.

Colin Morton has been adding to both London-listed stocks in his Franklin UK Equity Income and Franklin UK Rising Dividends portfolios. He says that over a long period, they’ve both produced very good dividend growth and dividend yields and both have very good free cash flow yields and strong market positions.

Whether NGPs present a challenge or an opportunity is ‘the million dollar question’, chuckles Morton. ‘Will they end up being the market leaders in NGPs and will they be able to make the same margins and profitability?’ he rhetorically asks.

Morton believes that a lot of the bad news is already in the price and he is willing to take a risk that more likely than not, BAT and Imperial will be the winners no matter what happens.

BRITISH AMERICAN TOBACCO

BAT has invested heavily in the vaping category, while also doubling-down on the combustible business through its blockbuster takeover of Reynolds American.

A high-quality behemoth armed with strong brands including Dunhill, Kent, Lucky Strike, Pall Mall, Camel and Newport, BAT generates high gross margins north of 85% and is highly diversified with a presence in 200-plus markets and an attractive emerging markets footprint.

However, the £88bn cap faces significant regulatory risk in the US, where the FDA has given advanced notice of proposed rulemaking on setting a nicotine standard, although it is possible a nicotine standard won’t be implemented at all.

Following its £41.8bn takeover of Reynolds American, the US has become BAT’s biggest and most profitable market.

BAT’s biggest NGPs opportunity is tobacco heated products (THPs), which generate higher gross margins than the combustible business; the portfolio includes THP product glo, Vype e-cigarettes and the VUSE vapour brand.

BAT has a stated target of NGP sales of £5bn by 2022, 70% of which it sees as being heated tobacco sales, the other 30% vaping-related.

Liberum forecast 2018 pre-tax profit north of £9.55bn, moving to £10.3bn in 2019 and £10.98bn in fiscal 2020.

Based on this year’s 295.5p earnings per share estimate and a forecast hike in the dividend to 203.9p (2017: 195.2p), BAT swaps hands for an undemanding 12.9 times forecast earnings and offers a 5.3% prospective dividend yield.

IMPERIAL BRANDS

Cigarettes, fine cut tobacco and smokeless tobacco manufacturer Imperial Brands is often seen as the sector’s growth laggard and rated accordingly, although it is actually gaining share in conventional tobacco.

The smallest of four global tobacco giants, Imperial generates 80% of profits from tobacco in mature markets such as the US, UK, Germany, France, Spain and Australia.

Its growth brands include Davidoff, Gauloises Blondes, JPS, Winston and Lambert & Butler, while Imperial’s specialist brands include blu, Kool, Golden Virginia and Montecristo.

Imperial’s margins came under pressure in 2017 due to increased brand investment and tough trading in Russia, while 2018 profit will be crimped by the bankruptcy of tobacco wholesaler Palmer & Harvey.

The good news is that under CEO Alison Cooper, Imperial is rationalising its brand portfolio and migrating niche brands to global brands with scale, a strategy designed to deliver better growth and enhanced margins.

The £27.2bn cap is targeting up to £2bn of proceeds from the sale of further non-core brands within the next 12 to 24 months.

Imperial’s NGP portfolio is built around its pioneering blu e-vapour brand, although the consumer staple is expected to have a heated tobacco product ready for late 2018 or early 2019.

An income-investor’s favourite down the years, Imperial targets 10% dividend growth per year and the half year payout (9 May) was raised by 10% to 56.87p. However, Liberum cautions dividend growth must taper in 2021 ‘without a meaningful step change in growth’.

Due to its size relative to rivals, Imperial Brands is also a perennial takeover target, although any takeover would be complicated by being a consortium bid; the most likely bidder would be Japan Tobacco, with BAT probably picking up any crumbs from the Japan Tobacco table.

Berenberg forecasts adjusted earnings per share of 267p and 188p dividend for 2018, rising to 279p and 207p respectively in 2019.

On these estimates, the shares trade on a PE of 10.8 with a juicy 6.5% dividend yield.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Aequitas

Big News

- Sosandar is a rare retail success story in 2018 with soaring shares

- Asset valuation concerns cloud Hammerson as it seeks £1.9bn disposals

- Shareholders rally to block excessive pay packages

- Can Jack’s work its magic as Tesco’s new discount chain?

- Renewed speculation that GlaxoSmithKline could spin off consumer division