Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineShould I prioritise repaying debts or investing?

Once you start planning for your future one of the biggest decisions you’ll face is whether to begin investing or pay off debts.

Both are commendable and necessary measures that will improve your chances of reaching your financial goals.

The decision will often come down to the types of debt you have and the return you hope to achieve on investments.

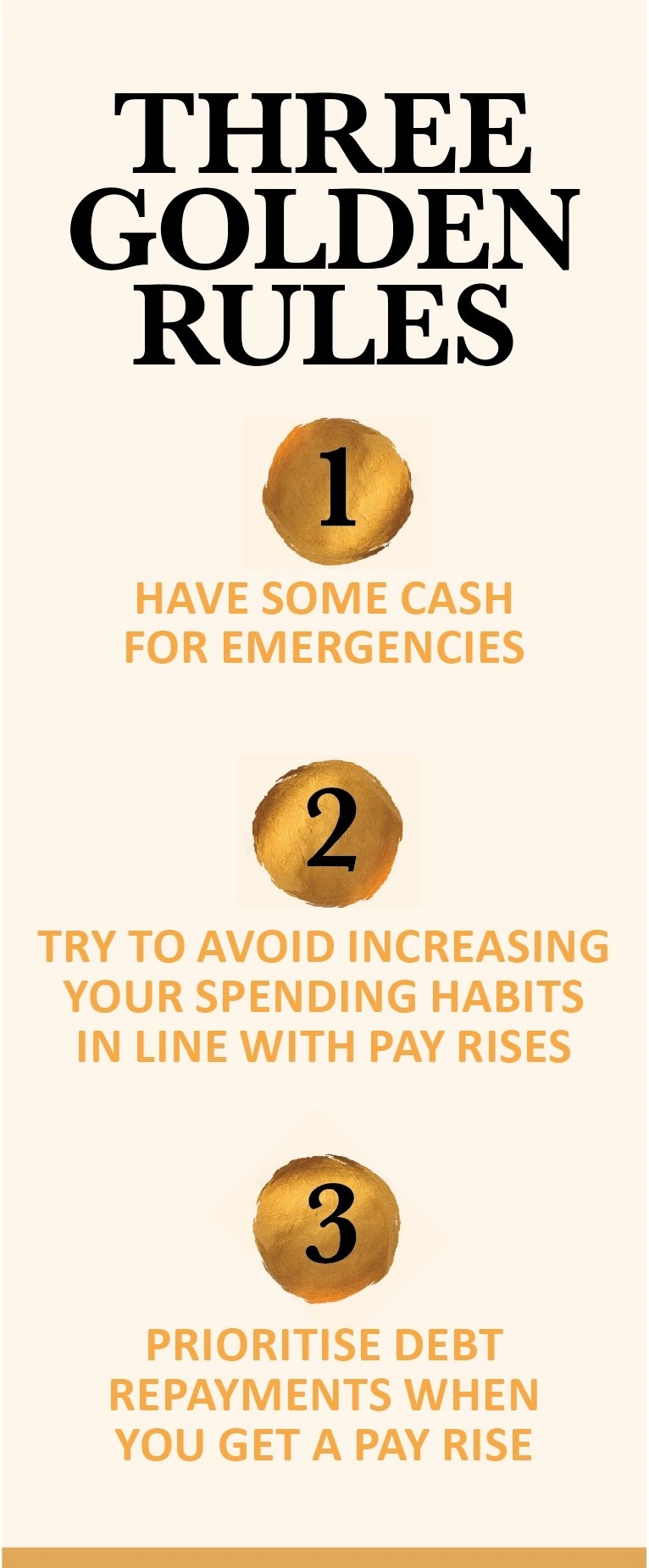

IS IT WISE TO PAY OFF DEBTS FIRST?

It is usually better to pay off debts before you start investing, especially if the interest rate on your debt is higher than the returns you could expect to gain from investments.

Imagine you’ve got £10,000 in credit card debts and the interest rate is 18%. This debt is not only costing you a huge £1,800 a year, but it will be a challenge to achieve this rate by investing.

‘Expensive debt means that the interest rate charged by, for example, credit card providers and lenders on outstanding balances will undoubtedly be greater than the returns you can make on your investments,’ says Andrew Craig, founder and author at Plain English Finance.

‘It’s like filling a bath with the plug hole open – the speed at which the water disappears down the plug hole exceeds the speed at which the water is filling the bath.’

The interest rate, size and lifespan of the debt and affordability are all factors you should consider when deciding the best strategy to repaying debt.

WHAT ABOUT LOW INTEREST RATE DEBTS?

In theory, if investment returns are likely to be higher than the interest you’re paying on debt it may make sense to consider delaying or reducing your debt repayments until the situation changes.

The problem is that returns on investments aren’t guaranteed and you can lose money.

‘Deciding whether to pay off debts or invest isn’t as simple a decision as it may first appear,’ cautions Tom Selby, senior analyst at AJ Bell. ‘This is partly because whether such a decision is proven “right” or not depends on future investment returns which, by definition, are unknown.’

If you think the debt is manageable, it might make sense to balance the debt repayment with some investment, especially if the loan has a long lifespan and interest rates are very low.

WHY IS MORTGAGE DEBT ANY DIFFERENT?

Many investors are likely to be paying off a mortgage, so it’s reasonable to wonder why that type of debt should be treated any differently.

It’s partly down to the way people view mortgages. ‘For most people a mortgage replaces the cost of renting a property so it is seen as a simple exchange of costs,’ says Adrian Lowcock, investment director at asset manager Architas. ‘In addition to this, unlike many other loans, you get something in return – a property.’

Mortgages are a loan that can last decades. ‘It becomes impractical to wait to invest until the mortgage has been repaid,’ adds Lowcock. ‘One of the strengths of investing is compounding and returns are delivered over the longer term.’

However, if you fail to keep up your interest repayments, your bank will probably sell the property to repay the loan.

SHOULD I PAY OFF MY STUDENT LOAN?

Student debts are slightly different to other debts because repayments only have to be paid once your salary reaches a certain level. They are wiped out altogether after 30 years, or if you die.

You pay back 9% of your income annually over the minimum amount of either £18,330 or £25,000 depending on which of the two different loan plans you are on. If you’re in a good job, you may have spare cash left over each month, even after accounting for your student loan repayments.

Interest rates on student loans vary enormously, depending on factors such as the year you started your higher education and how much you’re currently earning.

AJ Bell’s Tom Selby says a graduate with £10,000 of student debt where the interest rate is just 1.5% might prefer to invest any spare cash in an ISA or SIPP (Self-Invested Personal Pension), assuming they’ve not got any additional debts incurring high levels of interest.

‘For most people with any form of debt, it will be a question of balancing saving and investing with paying off any debts they have,’ he explains.

‘When making this decision, it’s worth remembering that early money invested in the stock market can benefit from the magic of compound growth, while vehicles like ISAs and SIPPs allow you to take advantage of tax-free investment growth.’

IS IT SENSIBLE TO INVEST IN A PENSION IF I HAVE DEBTS?

Paying into a workplace pension is a sensible move even if you have debts because many employers will match your contributions. You’ll also get tax relief on the contributions.

‘This uplift makes pension contributions rather attractive,’ says Matthew Bonney, financial planner at European Wealth.

‘But younger savers should keep in mind that they’re unlikely to be able to retire until they are at least 68. As such, if you have the means, a mix of pension contributions and building an accessible savings pot – via a stocks and shares ISA for instance – may well be more prudent.’

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Eurozone relief... but for how long?

- Good week for the markets but setbacks for Reckitt and Clarkson

- Stadium purchase to accelerate TT Electronic’s profits scale

- Online isn’t necessarily the ticket to retail success

- Should shareholders get involved with Capita’s £701m rights issue?

- Fast growth vaping firm Supreme to float on the stock market