Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineFive ways to play the stronger oil price

Oil prices are marking new multi-year highs as we write, supported by a larger than expected draw on crude stocks in the US and bullish comments from Saudi Arabia.

Geopolitical tensions impacting major oil producing regions such as the Middle East and Russia have also contributed to the strength in prices.

Like most markets, oil is driven by supply and demand factors. Conflict and tension in major producing areas has implications for supply and falling US inventories are indicative of strong demand.

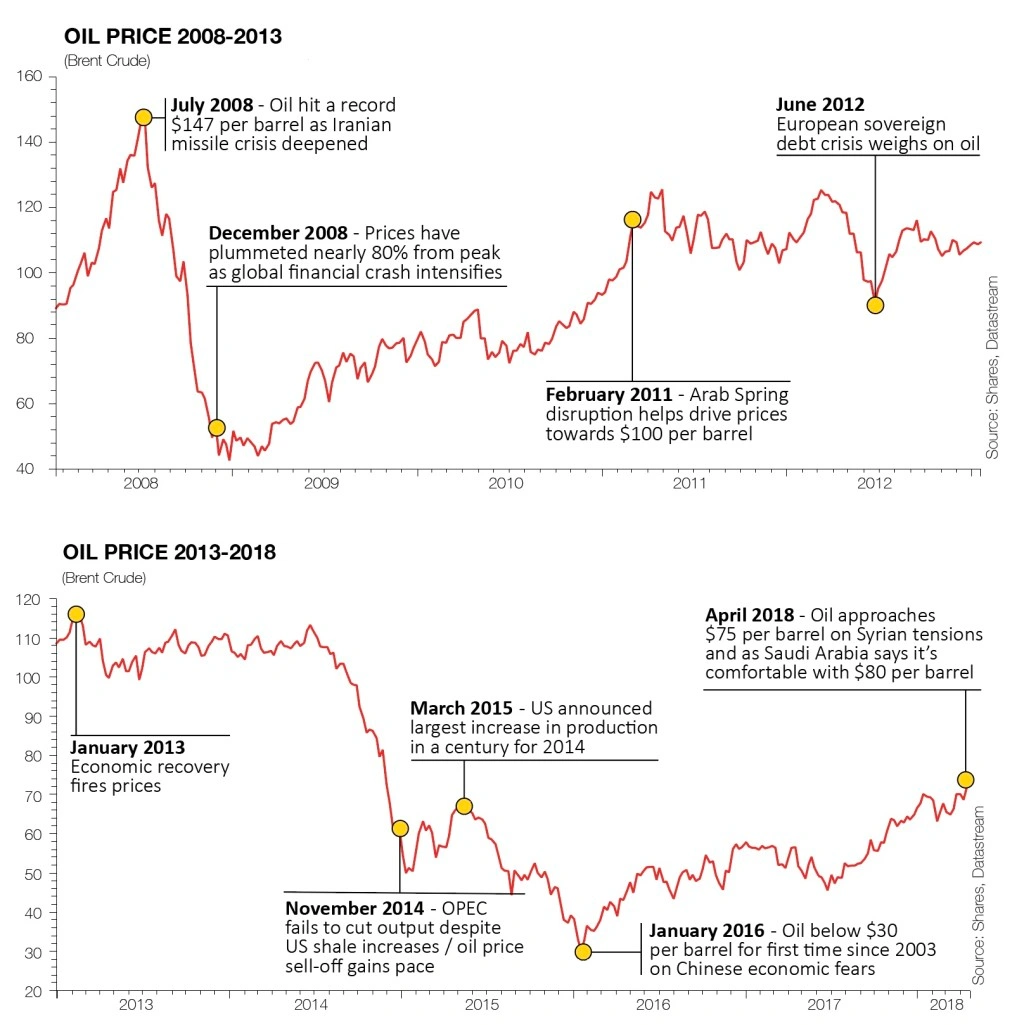

The Brent crude benchmark has been above $60 per barrel for around six months and has rarely traded below $50 per barrel in the last two years.

For industry and investor sentiment, the relative stability of prices is probably more relevant. We’ll reveal five investment ideas later in the article; first it is important to understand the context behind recent oil price movement.

There are several key factors impacting on supply: disruption thanks to geopolitical issues; industry spending; US shale output; and the actions of producers’ cartel OPEC.

In the wake of the 2014 oil crash when prices sank from more than $100 per barrel to less than $30 within 18 months, spending on the exploration projects required to generate future production dried up. However, this has been masked by a substantial uplift in shale production in the US.

The International Energy Agency forecasts US oil output will grow by 1.4m barrels of oil per day (bopd) by 2022 at an oil price of $60 per barrel, building on current record levels of 10.4m bopd.

THE IMPACT OF SHALE PRODUCTION

In 2013 and 2014 shale production began to ramp up to material levels. At a pivotal meeting in November 2014, after oil prices had already come under pressure due to a growing supply glut, OPEC failed to curb its own output.

This was perceived as an attempt by dominant member Saudi Arabia to neutralise the competitive threat posed by US shale by pricing operators out of the market. However, improvements in technology and increased efficiency enabled many projects to remain commercial even at lower oil prices.

The difference between 2014 and today is that OPEC has signalled its intent to support prices. Having capitulated on its apparent price war in late 2016 by announcing curbs on output, there are recent suggestions the Saudis would be happy to see prices of $80 or even $100 per barrel.

In the longer term electric vehicle adoption might impact oil consumption but the short-term picture looks more positive as crude will remain a key engine of economic growth.

The International Monetary Fund’s estimated global growth rate of 3.9% in 2018 and 2019 therefore has healthy implications for oil demand, barring an escalation of the current war of words over trade between major players US and China.

CAN THE E&P SECTOR BOUNCE BACK?

The exploration and production (E&P) sub-sector includes those companies which focus purely on the upstream part of the oil industry – in other words either seeking or producing oil and gas or a combination of both activities.

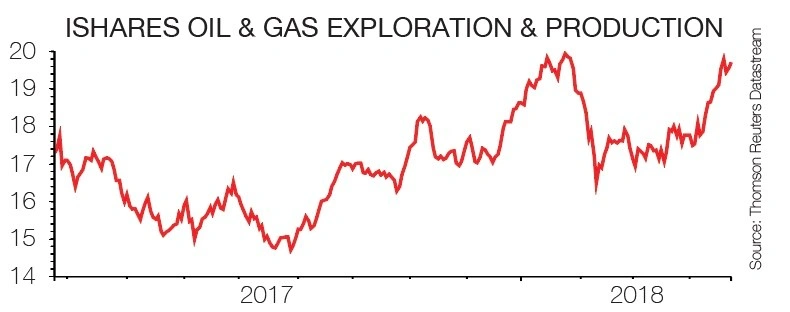

This space has endured several years of underwhelming returns, even before the collapse in the oil price. In effect investors have endured a lost decade and more with the index trading roughly where it was in January 2005.

As the chart shows the sector’s performance went from mediocre to disastrous in the wake of the collapse in the oil price as companies faced substantial balance sheet pressures to the extent that some simply went bust.

Before the oil price became a factor, there were several other issues which negatively affected sentiment towards E&P companies.

Operational performance was patchy, corporate governance left plenty to be desired, there was limited M&A activity and many results from exploration drilling were poor.

This last point is important. A big reason for investing in the sector is the step change in valuation which can be achieved when a company strikes oil. Yet UK E&Ps have made far too few discoveries in recent years.

Exploration is a high-risk activity and often has a binary outcome – a commercial discovery will result in a big advance in the share price and failure to find oil or gas in commercial quantities will lead shares to crash in value.

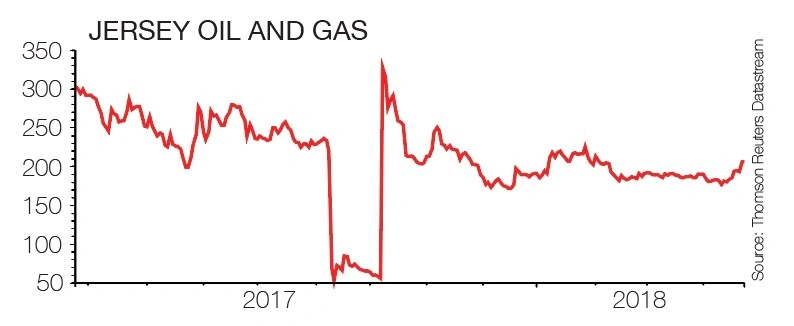

AIM-quoted oil explorer Jersey Oil & Gas (JOG:AIM) is a good example. On 9 October 2017 it traded 200% higher at 170p as a well, drilled in partnership with Norwegian operator Statoil, uncovered up to 130m barrels of oil.

However, a month earlier a previous well on Verbier, in which Jersey has an 18% stake, was less successful and prompted Jersey’s shares to shed more than 70% of their value in a day.

TAKING ADVANTAGE OF VALUATION ANOMALY

With E&Ps written off almost indiscriminately by the market, investors do not necessarily need to expose themselves to binary exploration outcomes.

Newly listed vehicle Reabold Resources (RBD:AIM) is focused on companies on the cusp of generating cash flow from their assets and ones which require a relatively limited amount of appraisal drilling to get them there.

Co-chief executives Stephen Williams and Sachin Oza, former fund managers who went down this route having failed to secure sufficient funds for an oil and gas investment trust in early 2017, note many of these firms are being valued at the same level as companies in the very first stages of exploration.

Once a company is generating cash flow it tends to get more credit from the market (and thus a higher equity valuation) and Williams and Oza hope to benefit from this anomaly.

Reabold is looking to invest around £2m to £3m in firms to allow them to meet the costs of an appraisal well.

Since Williams and Oza took over at the company in October it has made two investments – one in Corallian Energy, which is developing a near shore development in the UK; and one in Danube Petroleum, a subsidiary of ASX-listed ADX Energy operating in Romania.

FIVE WAYS TO PLAY THE STRONGER OIL PRICE

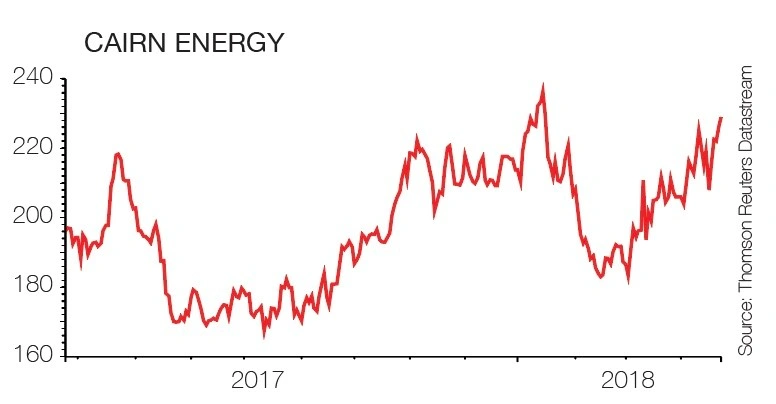

Cairn Energy (CNE)

222.8p

BUY

Unlike some companies in the sector, this mid-cap has a robust balance sheet with $57bn of net cash, so you can have greater confidence it is being run in the interests of shareholders rather than creditors.

The company should benefit from a ramping-up in output from its North Sea Catcher and Kraken fields in 2018. Cairn will also focus on its SNE development offshore Senegal where a farm-out could act as a catalyst for the shares, as well as a Norwegian exploration drilling programme.

You should also look for a final resolution of an Indian tax dispute which, if it went in Cairn’s favour, would allow it to realise value for its remaining interests in the country to which the market effectively ascribes zero value at present.

Diversified Gas & Oil (DGOC:AIM)

85p

BUY

A constituent of our Great Ideas portfolio, Diversified Gas & Oil is the largest producer in the AIM oil and gas universe with production of 28,000 barrels of oil equivalent per day, mainly natural gas from the Appalachian basin in the US.

The growing output, boosted by two substantial acquisitions earlier this year, underpins an attractive income story in the E&P space.

Having pledged to pay out 40% of free cash flow in dividends, earlier this month the company confirmed a 5.44 cents dividend for 2017 to be paid in May. This in turn implies a yield of 4.6%.

Thanks to the consistency of its cash flow the company plans to move to quarterly dividends in 2018.

With limited debt on the balance sheet, the company has scope to acquire further assets and by doing so boost cash flow and dividends further.

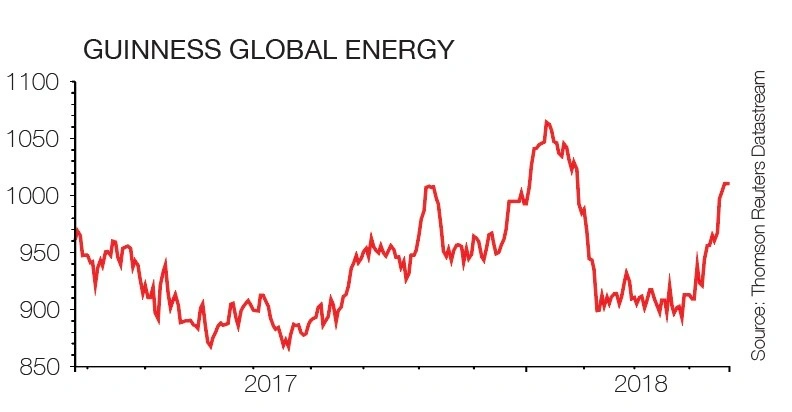

Guinness Global Energy (IE00B6XV0016)

997p

BUY

Launched in 2008 this specialist energy fund has around half of its assets in the US, 15% in Canada and a little over 10% in the UK, providing genuinely global exposure to the industry.

Among its largest holdings are the big US oil services firms Haliburton and Schlumberger alongside producers like Chinese state operator CNOOC and Canadian firm Suncor Energy.

Fund managers Tim Guinness, Will Riley and Jonathan Waghorn believe improving free cash flow from the sector should see companies trade at a higher multiple of the value of their assets.

iShares Oil & Gas Exploration & Production (IOGP)

$19.53

BUY

This exchange-traded fund may suit someone seeking to get diversified exposure to the oil industry with a low ongoing charge of 0.55%.The ETF tracks the performance of a global basket of companies which engage in exploration and production activities. Constituents of the index being tracked include ConocoPhilips, Woodside Petroleum and EOG Resources.

Jersey Oil & Gas (JOG:AIM)

193p

BUY

This story looks lower risk than in 2017 when the company’s hopes were entirely pinned on the results of exploration drilling on its Verbier prospect in the North Sea.

Jersey, in partnership with large Norwegian outfit Statoil, is drilling a lower risk appraisal well this summer which could still deliver material upside. This follows a major discovery in 2017.

A rig has been secured and having raised £23.8m last year, Jersey is fully funded for its share of the well costs. Successful appraisal drilling could prove up value of nearly £200m against a current market cap of just £45m.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Eurozone relief... but for how long?

- Good week for the markets but setbacks for Reckitt and Clarkson

- Stadium purchase to accelerate TT Electronic’s profits scale

- Online isn’t necessarily the ticket to retail success

- Should shareholders get involved with Capita’s £701m rights issue?

- Fast growth vaping firm Supreme to float on the stock market