Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineHow the SOX index can help investors work out whether stock markets are going to rock or roll

A slide in the share prices of Facebook, Apple, Amazon, Netflix and Google’s parent Alphabet, the so-called FAANGs, and Tesla

is grabbing all of the headlines.

Whether this is down to a collection of company specific reasons – such as questions over Facebook’s involvement in the Cambridge Analytica data use scandal, attacks on Amazon by President Trump (which could just be payback for Amazon boss Jeff Bezos’ ownership of the Washington Post newspaper) or Tesla’s inability to meets its production targets or get even close to making a profit – or a wider move away from highly-valued, momentum-driven, risky securities remains to be seen.

Such stock-specific niceties may not trouble all investors. But if they really want to get a real grip on technology stocks and stock markets more generally then they should be keeping an eye on the Philadelphia Semiconductor Index, more commonly known as the SOX index.

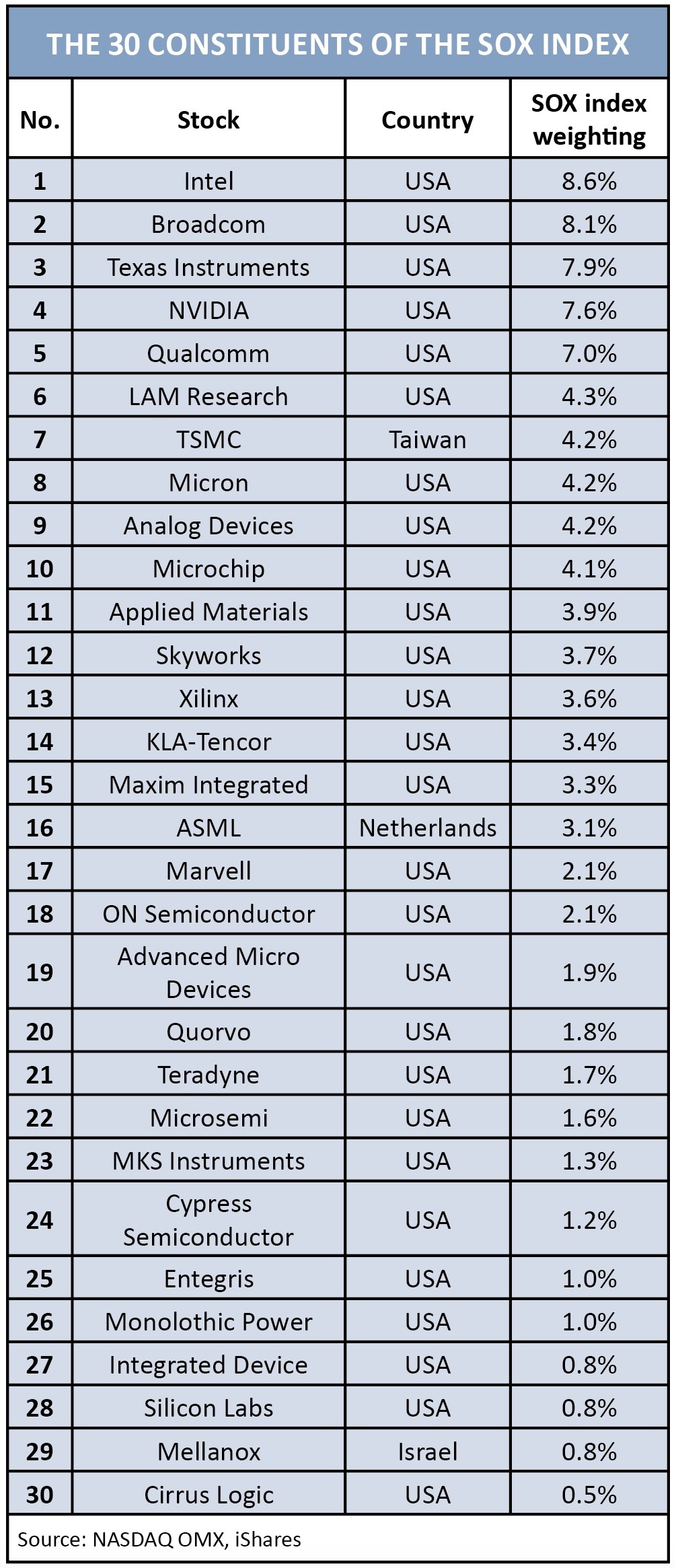

The benchmark contains 30 companies who are involved in the design, manufacture and sale of silicon chips and it is therefore a very useful guide for investors on two counts.

These integrated circuits are everywhere, from smart phones to computers to cars to robots, so they offer a great insight into end demand across a huge range of industries and therefore the global economy.

Chip-makers’ and chip-equipment makers’ shares are generally seen as momentum plays, where earnings growth is highly prized and valuation less of a consideration. As such they can be a good guide to broader market appetite for risk.

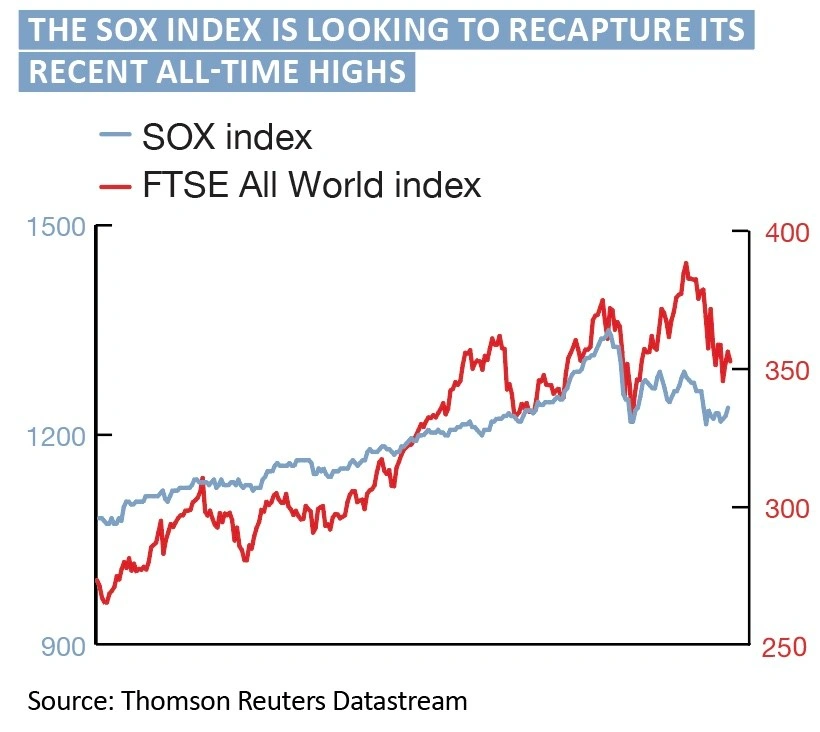

Since its launch in summer 1994 the SOX has been a good guide to America’s S&P 500 index but also the FTSE All-World benchmark. Peaks in the chip index in both 2000 and 2007 warned of trouble ahead on a much broader scale.

PULL UP THE SOX

The SOX could be every bit as useful a guide during this equity bull market, which began in 2009.

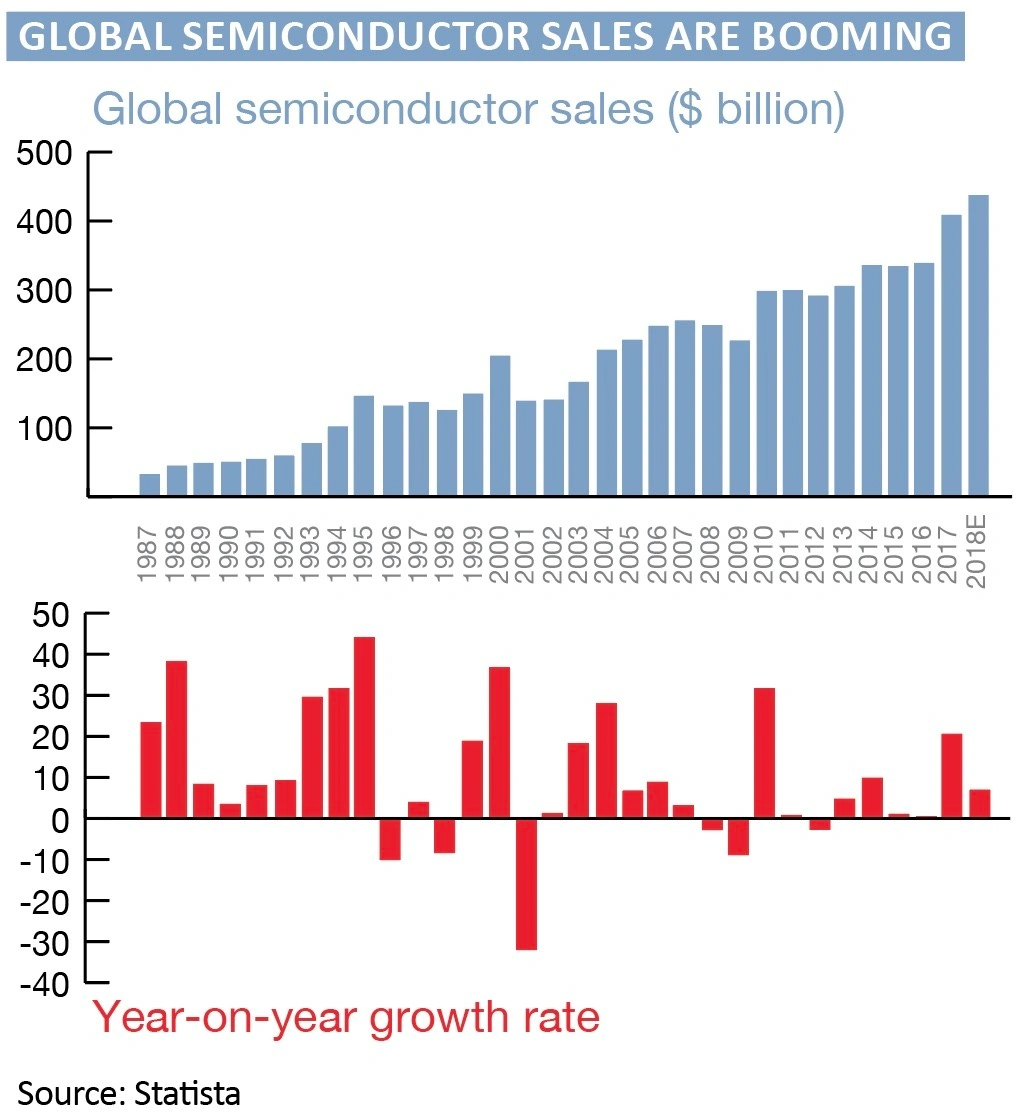

The good news, for the moment, is that the semiconductor industry grew like a rocket in 2017, as global sales surged by 21% to a new all-time high of $409 billion. Better still, revenues are expected to rise by at least 7% in 2018.

This may help to explain why technology overall has been a huge driver of equity market returns for investors.

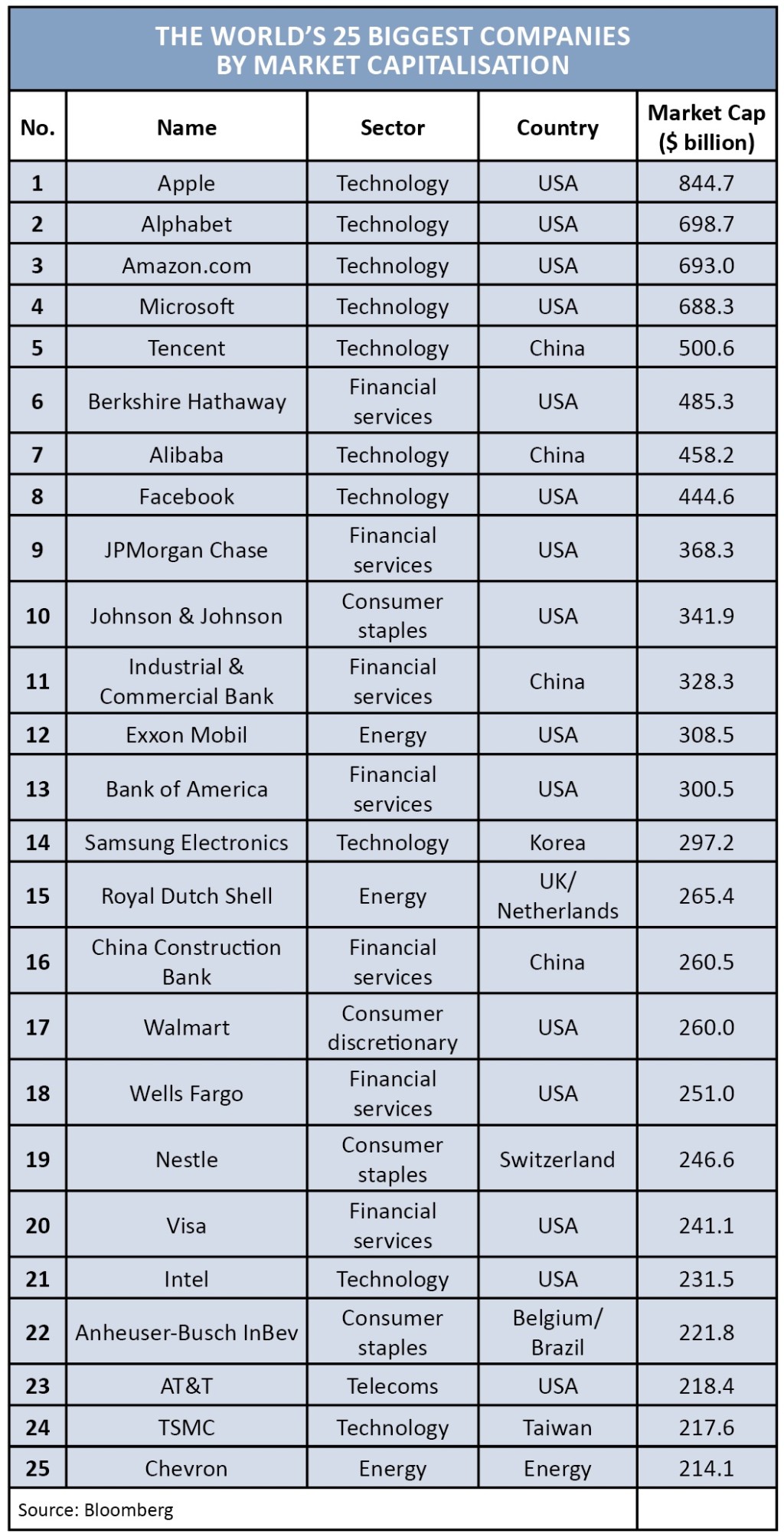

The net result is that 10 of the world’s 25 biggest companies by market capitalisation now hail from the tech sector.

This list includes three silicon chip makers – Intel (the world leader in microprocessors), Samsung Electronics (the world leader in memory chips) and Taiwan Semiconductor Manufacturing Company (the world’s biggest foundry, or chip maker on an outsourced basis).

IMMINENT NEWS FLOW

The good news is that Samsung Electronics has got the first-quarter reporting season off to a good start by estimating that profit for the January-to-March period will rise by 58% year-on-year.

However, that did not prevent a dip in the shares, which are still trading a fraction below March’s all-time high of Won 2.88 million.

Investors will therefore be looking to the first-quarter reporting season from Intel, TSMC and other leading SOX index members such as Broadcom, Texas Instruments, NVIDIA and Qualcomm

for reassurance on both end-demand and also share price momentum, especially as the silicon chip benchmark is no higher than it was in November.

After all, some cracks have already appeared in the technology edifice.

Despite the apparent success of the Dropbox and Spotify initial public offerings (IPOs), at least if they are measured by immediate share price performance in the wake of their listings, investors have begun to ask more questions of technology stocks and richly-valued but ultimately loss-making companies.

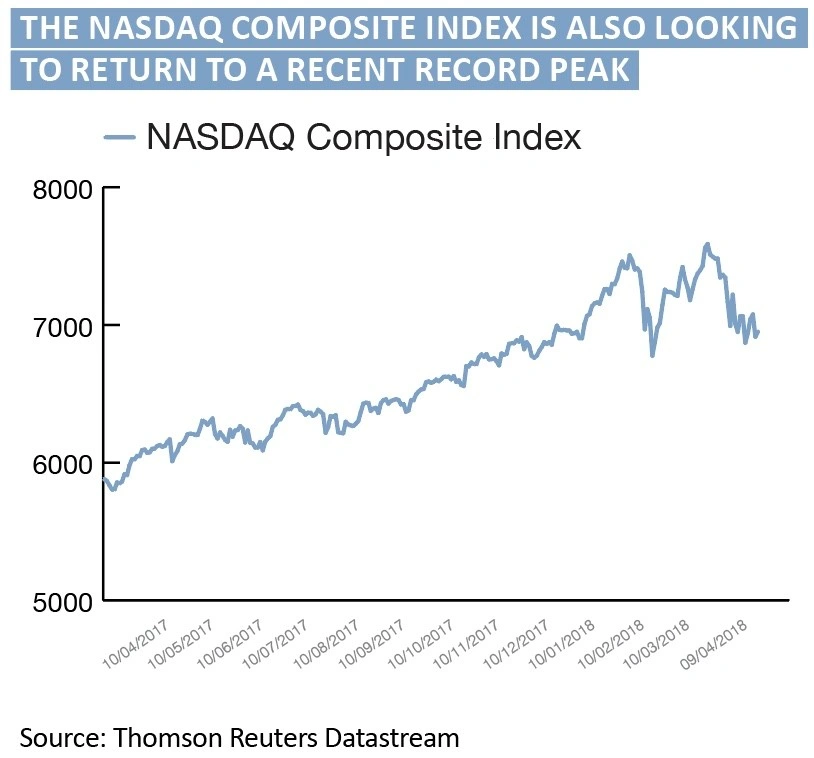

We have already seen the sharp drop in the FAANG stocks and the recently-created index that tracks them, as well as the retreat in wider, technology-laden NASDAQ index.

Softbank may have shown faith in transport technology platform (or taxi service, depending on your viewpoint) Uber, despite its governance and regulatory problems, but the Japanese technology investment behemoth injected capital at a price which implied a one-third cut in Uber’s valuation to $48 billion. This is known as a “down round” in the world of venture capital and is not normally seen as good news.

Twitter and Snap have both struggled to hold on to the share price gains they made in the wake of their respective stock market flotations in 2013 and 2017 respectively.

None of these have to signal that the tech is about to fall out of favour and take risk assets more generally with it. But tracking the SOX index and silicon chip stocks in particular may help investors in forming their view on this sector and, as a result, their asset allocations more broadly.

Russ Mould,

AJ Bell investment director

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- JD Sports is still fighting fit

- ImmuPharma collapses on trial failure

- British Airways owner eyes takeover of Norwegian Air

- Apollo stalks FirstGroup with takeover interest

- Pound pushes to highest level since Brexit vote

- Cyber security firm Avast set for £2.8bn IPO

- Activist investor Elliott rumoured to have Micro Focus in its sights

- Costa spin-off calls at Whitbread gain momentum