Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThe Scottish Investment Trust takes a different approach

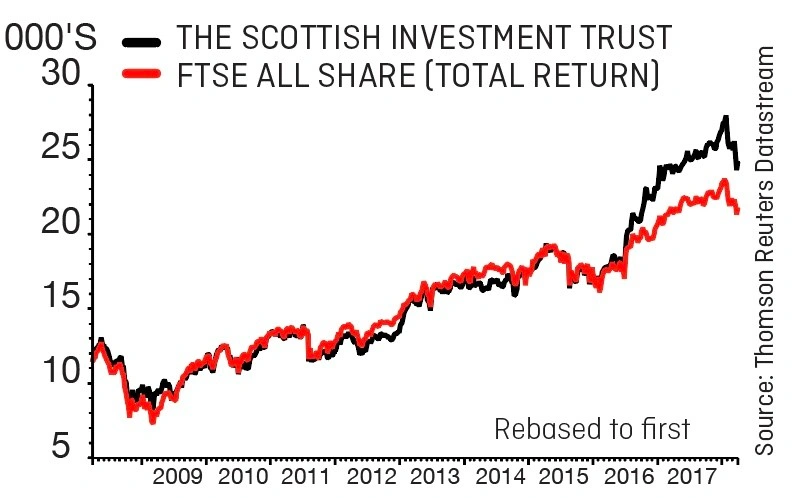

Trading at an 8.5% discount to net asset value, The Scottish Investment Trust (SCIN) may interest investors who want an investment trust that doesn’t chase the latest hot fads or so-called ‘story stocks’. Instead, this product is more interested in finding real value in the market.

Independently managed, the trust, which targets both income growth and above-market capital returns, has increased its regular dividend for 34 consecutive years.

The Scottish has delivered just under 10% annualised total return over the last three years. Ongoing charges are a relatively modest 0.49% a year and the trust has also announced a step-change in its dividend policy, increasing the regular distribution in preference to specials and moving to quarterly dividends. It has a 2.5% historic yield.

HIGH CONVICTION, GLOBAL CONTRARIAN

Contrarian investors look for companies whose potential for share price growth or recovery has been overlooked by the market. This style requires steely nerves; humans have evolved to like to belong to a group or feel a part of something bigger, so taking a contrarian stance is uncomfortable and you have to be patient as the investment case unfolds.

The Scottish’s fund manager Alasdair McKinnon and his team are firmly in the contrarian camp. They employ behavioural finance techniques to exploit investors’ tendency to ‘follow the crowd’. By focusing on stocks that are very unloved, those with operational improvements that have been overlooked, and more popular stocks that can continue to do better, the managers build in a margin of safety.

GOING AGAINST THE GRAIN

Patient portfolio builder McKinnon seeks to avoid the ‘madness of crowds’, investing away from the herd and scouring the globe for undervalued, unfashionable companies that are ripe for improvement.

He runs a portfolio of global best ideas with 56 names held in the trust at last count; the largest sector exposure is to financials, where holdings include banks in the US, Europe and Japan.

Ever willing to go against the grain, McKinnon’s picks fall within three categories. ‘Ugly ducklings’: unloved shares most investors shun, among them large caps such as Tesco (TSCO).

‘Change is afoot’ stocks that have endured prolonged poor operating performance but have recently demonstrated improving prospects; examples include Dutch bank ING and Brazil-based beer brewing behemoth Ambev.

Last but not least are McKinnon’s ‘more to come’ ideas, sound businesses boasting decent prospects yet where scope for further improvement has yet to be fully recognised, such as Rentokil Initial (RTO).

BACKING BRICKS & MORTAR

McKinnon’s unwaveringly contrarian ethos has lead him away from the ‘second internet bubble’ – you won’t find a ‘FANG’ name or a cryptocurrency here – and into areas such as oil companies, banks and retailers.

Meeting with Shares recently, McKinnon enthused: ‘We quite like US retail and we’ve got some Macy’s, GAP and a relatively new holding in Target. And we’ve also got some UK retail in Marks & Spencer and Tesco.’

He adds: ‘Everyone thinks the internet is killing US department stores and malls, but actually, what’s killing US department stores has been the rise of off-price retail,’ referring to the likes of Ross Stores and TK MAXX across the pond.

‘We think people have become infatuated with the internet and its wonders. The internet retailers are valued as if they are going to dominate the world and everything they do is seen as a good, even when it is slightly eccentric, like buying a physical retailer like Whole Foods Market or a door bell manufacturer.

‘People have written off the physical retailers, whereas what’s really hurt them has been the economy. There hasn’t been money in people’s pockets, but Trump’s tax bill has put money in people’s pockets and they’ve got more money to spend in the shops,’ he says.

A positive contributor to the trust’s 2018 performance, Macy’s is the largest fashion retailer and department store chain in the US, operating under three banners: Macy’s, Bloomingdale’s and luxury beauty products retailer Bluemercury.

‘The company has seen declining store traffic as customers have been tempted away by discount and online retail,’ says McKinnon, ‘and it fits into our ugly duckling category.’

Under a credible management team, ‘the company is working to address its challenges’.

Tellingly, the canny stock picker adds that ‘the balance sheet is underpinned by a portfolio of real estate assets with an estimated total real estate value of $12.5-$13bn.

‘The value of these assets arguably does not appear to be reflected in Macy’s valuation, due largely to concerns about the outlook for traditional retailers,’ but ‘Macy’s is a leading brand in the US, is cash-generative and pays a covered dividend of over 7%.’

McKinnon believes the UK retail sector is interesting because of a likely increase in spending power as inflation falls and minimum wage increases come through.

This is one his bull points for Marks & Spencer, ‘in essence, a play on the UK middle class which has been squeezed, but that is just starting to turn the corner.’

Fresh from a one-on-one sit-down with M&S chairman and turnaround expert Archie Norman, McKinnon concedes ‘they are definitely over-spaced, but they know that and they are closing stores.

‘They just need the top line to improve and they are making lots of efforts to make that happen. We think they’ve got a good chance of turning it round.’ (JC)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.