Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineHow to test the foundations of the property sector

He is unlikely to have appreciated it, or cared, at the time, but Mark Twain’s advice to ‘Buy land, they aren’t making it any more’ has long since formed the basis of the investment case for UK commercial property, either via quoted stocks or dedicated funds.

Whether property is right for an investor’s portfolio will depend upon their overall strategy, target returns, time horizon and appetite for risk but at least some may look to it for income, some form of diversification or both.

It may also be cropping up on the radar of contrarians because it is easy to form a bearish view, despite Twain’s comments on the peculiarities of supply in the sector.

This is because Brexit is seen as casting a cloud over demand for UK commercial property, especially in London and its financial district in particular.

In addition, the Bank of England is working towards its next interest hike and sentiment toward the property sector is taking a battering in the wake of the woes of the retail and casual dining sectors.

The collapse of BHS and Toys R’Us, planned company voluntary arrangements at New Look and possibly Carpetright (CPR) (so they can streamline their estates and cut their rent bills) and store closures at Mothercare (MTC), to name but one, all raise questions over the state of Britain’s high streets and shopping centres, and their capital and rental value to landlords.

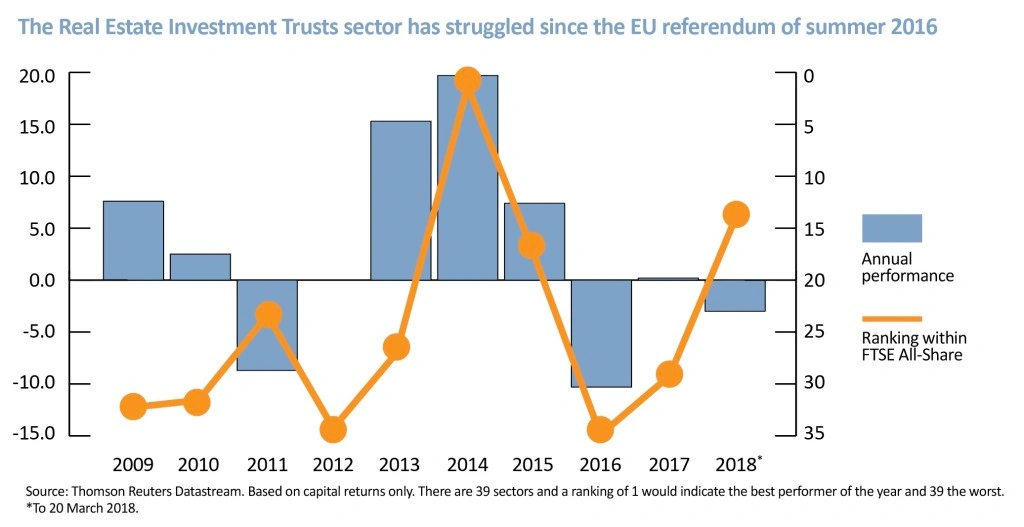

These fears are all reflected in the poor performance of the quoted FTSE All-Share Real Estate Investment Trusts (REITs) sector. In addition, investors will remember the post-referendum panic of summer when some property funds went into lockdown in the face of an initial torrent of redemptions.

And yet someone, somewhere seems to think the gloom may be overdone.

Hammerson (HMSO), the owner of the Brent Cross, Bullring and Cabot Circus shopping centres in London, Birmingham and Bristol respectively, has launched an all-share bid for fellow FTSE 250 stock

Intu Properties (INTU), which owns the Trafford Centre and Lakeside.

France’s Klepierre has since made a takeover approach for Hammerson.

Hong Kong billionaire Samuel Tak Lee has continued to build his stake in another FTSE 250 REIT, Shaftesbury (SHB), the owner of large swathes of property in Soho, Covent Garden and Chinatown in London, although there is no intimation that a full bid is in the offing.

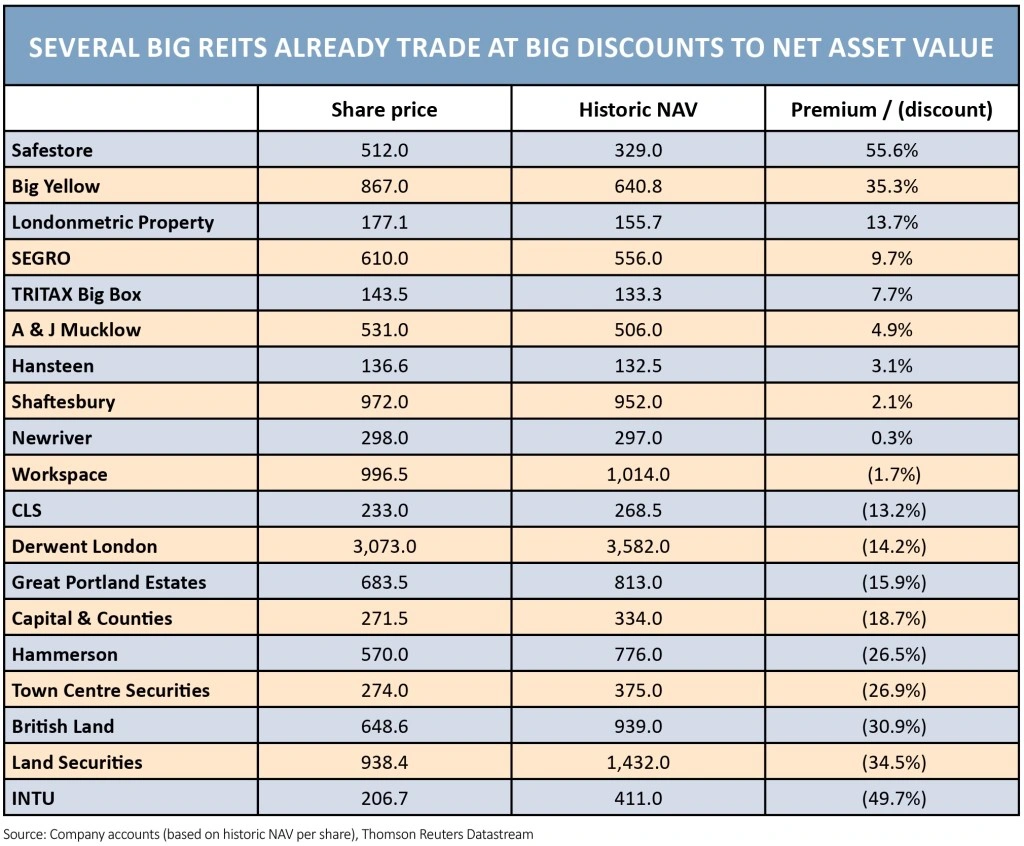

BIG DISCOUNTS

Such activity may not be brave as it may first seem, for all of the high street gloom, given some of the valuations on offer. Many REITs, or at least those with exposure to retail and London, are already trading at big discounts to net asset value, so it may be that a lot of bad news is already factored into valuations.

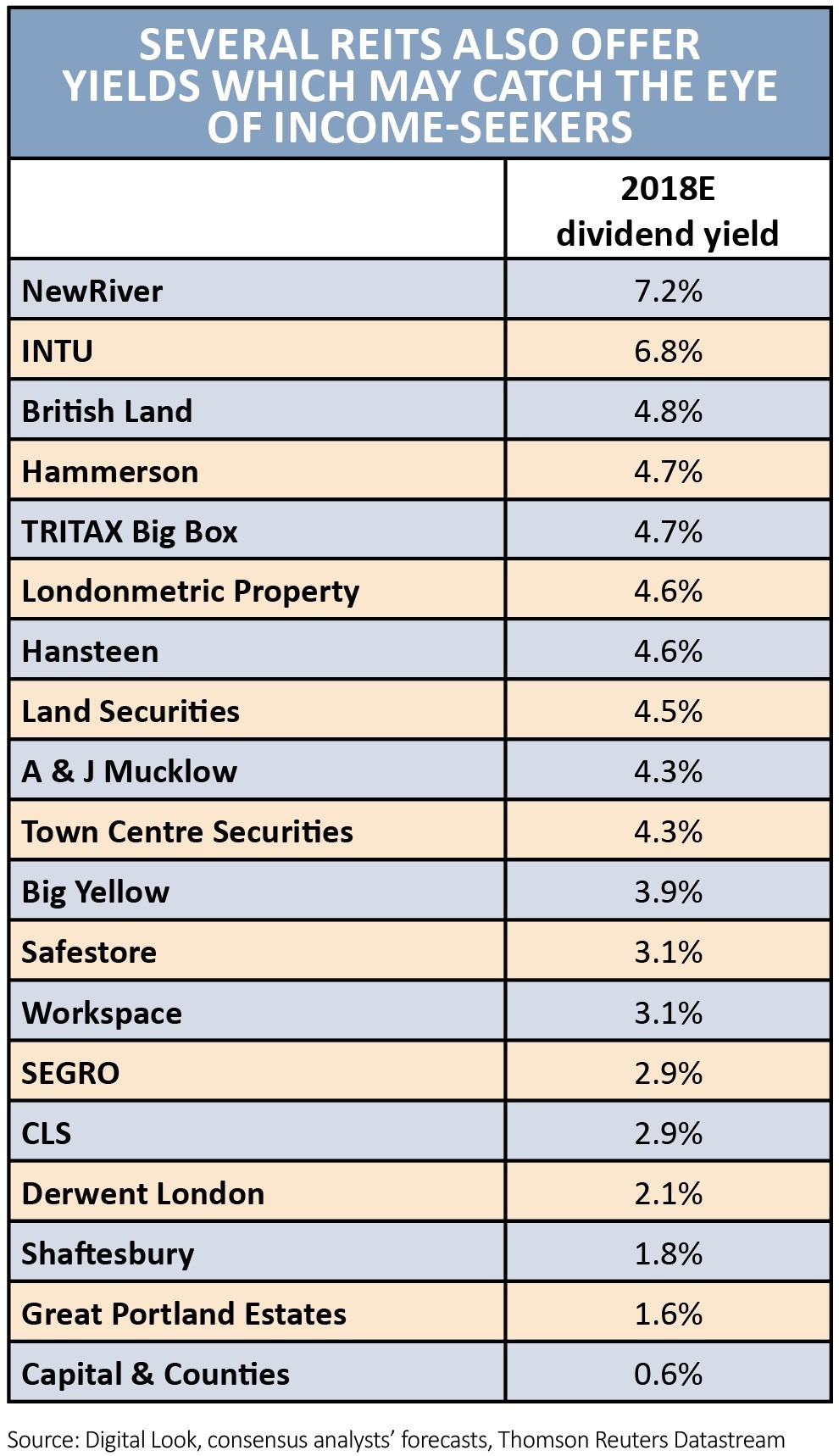

In addition, the full-year reporting season largely passed without major incident, with net asset values (NAVs) holding up well. The dividend yields on offer also still surpass the returns obtainable from Government bonds or cash (albeit in exchange for greater capital risk).

FUND OPTIONS

In the event that investors do not wish to embrace stock-specific risk, they can turn to funds.

AJ Bell’s list of favourite funds features two property collectives. The £3bn, actively-run Janus Henderson UK Property PAIF (GB00BP46GF57) has a mandate to generate capital growth and income over the long term.

It comes with a spread of retail, industrial/warehousing and office sites across the UK, with a bias toward the south east of England. It also has a 22% cash weighting to manage liquidity.

The passively-run, £780m portfolio of exchange-traded fund iShares UK Property ETF (IUKP) tracks a basket of 23 REITs quoted in the UK. As such, it is likely to provide less diversification for a portfolio that already has a heavy weighting towards equities, given that it provides property exposure via stocks rather than via direct ownership of the buildings.

END GAME

It may be that the market is correct and a post-Brexit slowdown is coming at the same time as fresh supply, to the detriment of those REITs with exposure in London’s financial district.

There is a clear trend in the accompanying net asset value (NAV) discounts table, in that the less exposure a REIT has to London’s financial district and to new development, the higher the valuation it currently commands.

But at least valuations are lowly and sentiment already depressed at those REITs with exposure to London, retail, new development or all three.

This brings to mind another quote, this time from Warren Buffett: ‘Most people only get interested in stocks when everyone else is. The time to get interested is when no-one else is. You can’t buy what is popular and do well.’

It will be interesting to see over the coming months and years whether this pungent aphorism works for property stocks.

Russ Mould, investment director, AJ Bell

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.