Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineXLMedia looks exciting... but is there a catch?

Online gaming marketing firm XLMedia (XLM:AIM) is fresh from announcing another set of record full year results. But is this growth stock getting the credit it deserves from the market and, if not, why not?

The Israeli company helps direct players and customers to online gambling sites through its portfolio of more than 2,300 websites and the purchase of online ads. It receives a share of the revenue this activity generates. In 2017 sales grew by a third to $137.6m and gross profit increased by 37% to $73.1m.

Consistent earnings upgrades and a compound annual growth rate (CAGR) in earnings of 37.2% since 2014 have helped drive significant gains in the share price since its IPO (initial public offering) at 49p in March of that year.

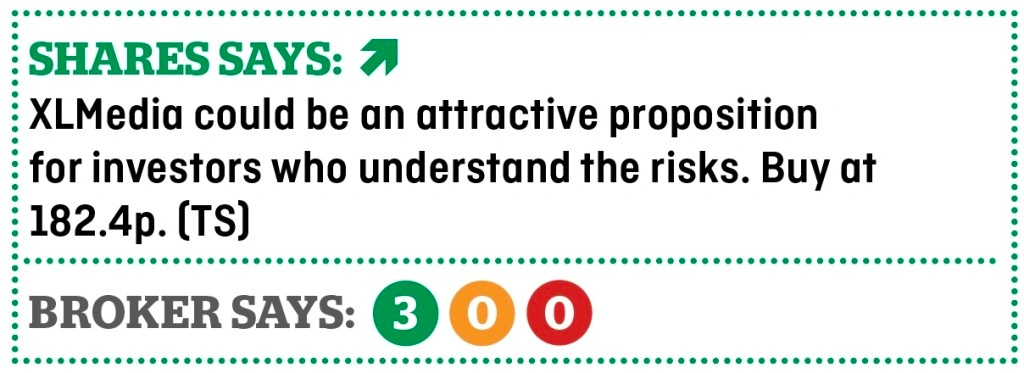

Today it trades at 182.4p, but this only represents a relatively undemanding 16 times Berenberg’s 2018 forecast earnings per share.

This rating compares unfavourably with another AIM growth stock – spirit mixers firm Fevertree (FEVR:AIM) which listed on the junior market around six months later.

Fevertree’s earnings growth has been more rapid at a CAGR of 54.5% over the same timeframe but its shares are up nearly 22-fold on the 134p issue price and they trade on a forward PE of close on 70 times.

There are reasons why XLMedia doesn’t have a premium rating. It is a harder business to understand than Fevertree and Israeli technology companies have not historically enjoyed the best

of reputations.

WHAT IS BEHIND RECENT SHARE PRICE WEAKNESS?

Recently XLMedia’s shares have drifted from the 220.5p record highs seen in December 2017. This is perhaps is a reflection of lingering scepticism towards the wider advertising tech space, a dilutive share placing in January 2018 and some concern about what barriers to entry the company enjoys.

The company recently raised £31.7m by issuing new shares to fund the acquisition of new websites. This raised some eyebrows given the company has virtually no debt and closed 2017 with cash of $43.3m, so perhaps didn’t need to issue new equity.

XLMedia generates a gross margin of around 80% on its website business and this kind of return seems sure to attract competition.

Stockbroker Cenkos argues the company enjoys genuine barriers to entry. Analyst Tom Callan says: ‘XLMedia’s online estate (+2,300 sites) cannot be easily replicated.

‘The group’s top performing assets consistently rank highly across all major search engines. Proprietary technologies (Palcon, Rampix) ensure the group remains at a consistent technological advantage versus immediate peers.’

The other risk to consider is increased regulation of online gambling and digital advertising which could represent a serious threat to XLMedia’s profits.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Impressive earnings ‘beats’ from service companies and engineers

- Barclays now in Edward Bramson’s cross-hairs

- What does Putin’s win mean for Russia-focused investments?

- FTSE 100 in a spin amid takeovers, restructures and spin-offs

- Is there more to come from Burford Capital?

- Pound see-saws on Brexit progress and softer price growth