Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineEKF Diagnostics seen as a future takeover target

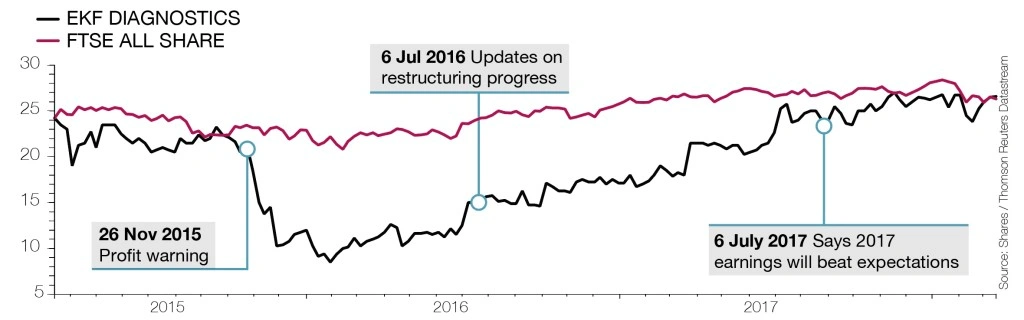

Healthcare company EKF Diagnostics (EKF:AIM) could become a takeover target if it successfully expands into new geographic regions with approved products, according to stock broker Panmure Gordon.

Analyst Julie Simmonds says the company has recovered from historic challenges and margins have improved sufficiently to make the business interesting.

She believes the company could eventually be acquired on a multiple of between three and four times sales, assuming it can expand product lines into new regions, particularly the US.

‘The current focus on driving profitability and cash generation puts EKF in a stronger position to drive this outcome,’ she comments.

‘With only a limited number of profitable companies with established point of care diagnostics products EKF has some scarcity value,’ adds the analyst.

EKF manufactures point-of-care devices and tests for haemoglobin, glucose and lactate levels, as well as glycated haemoglobin, also known as HbA1c.

Measuring glycated haemoglobin provides an overall picture of average blood sugar levels over a specific period.

The business is currently worth £123m which equates to three times 2017’s sales (£41.6m).

We believe the shares currently trade on a fair valuation given low expectations for near-term sales growth. Sales are only forecast to increase to £43.4m in 2018 and £44.8m in 2019.

You could argue that EKF really needs to accelerate earnings in order to capture the interest of a predator.

Potential catalysts would include the US approval of HbA1c measurement device Quo-Test and handheld haemoglobin analyser DiaSpect.

N+1 Singer analyst Chris Glasper argues future growth can be supported by investing in manufacturing capacity to drive stronger margins and add revenue opportunities.

He is confident EKF can launch new product variants, highlighting a ‘potentially significant opportunity in early sepsis detection’ and gains from monetising sTNFR biomarker technology.

Glasper believes EKF is ‘materially undervalued’ compared to its peers and reckons positive momentum in the business and/or acquisitions could help the shares hit 35p to 40p over the next few years. They currently trade at 26.9p (LMJ)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Impressive earnings ‘beats’ from service companies and engineers

- Barclays now in Edward Bramson’s cross-hairs

- What does Putin’s win mean for Russia-focused investments?

- FTSE 100 in a spin amid takeovers, restructures and spin-offs

- Is there more to come from Burford Capital?

- Pound see-saws on Brexit progress and softer price growth