Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazine10 stocks for your ISA

The end of the tax year is fast approaching which means investors across the country are being urged to make the most of any unused ISA allowance.

You’ve only got three weeks left to add up to £20,000 across the range of ISAs. This is the maximum amount of cash you can place in the tax wrapper each year for making investments. The deadline is 11.59pm on 5 April.

You don’t have to pay any tax on capital gains and dividend income if your investments are held inside an ISA wrapper. If you’re serious about investing, using as much of your ISA allowance as possible each year must be a priority.

IDEAS FOR YOUR ISA

We recently published a list of 10 fund ideas to give you inspiration for potential ISA investments. This new article features 10 stock ideas and we’ll publish 10 investment trust ideas in Shares on 29 March.

Our stock ideas are aimed at long-term investors. We’ve looked for companies with a track record of profit growth and which haven’t issued profit warnings over the last few years.

LARGE CAPS

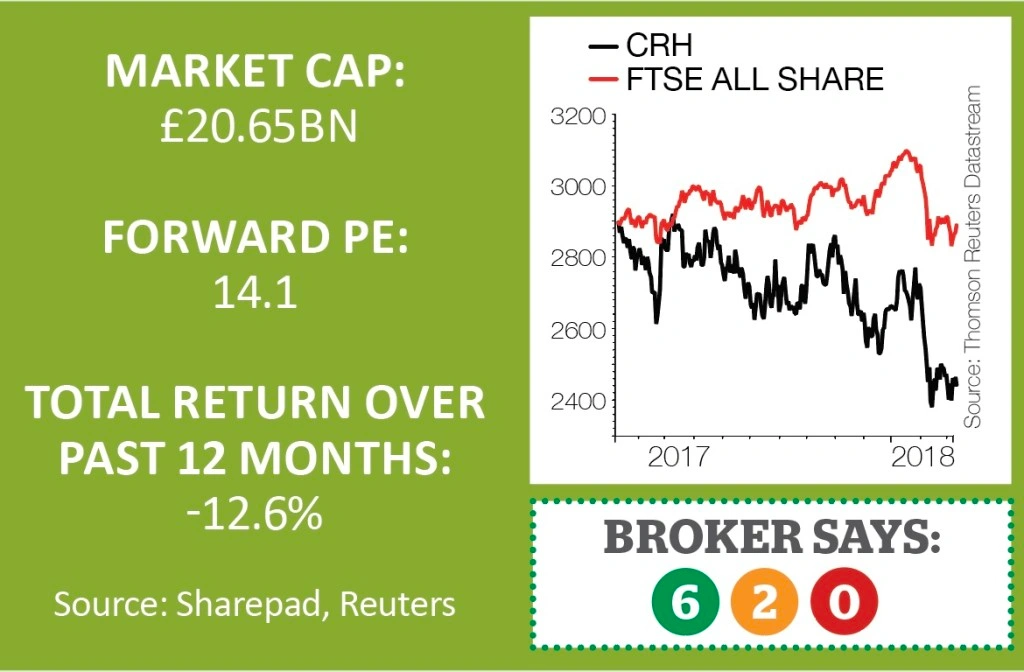

CRH (CRH) £24.22

FTSE 100 building materials business CRH (CRH) provides everything from foundations to frames, roofing and interiors to the construction industry. It has operations in 32 countries and employs some 85,000 people across 3,600 locations.

The Dublin-headquartered company’s business model involves continually looking to see how existing businesses can be improved and making select acquisitions. CRH aims to be diversified across different products, geographies and end-uses to mitigate fluctuating demand at different points of the business cycle.

In recent years the company has achieved a material improvement in its profitability and returns. Analysts at stockbroker Davy estimate return on net assets, a metric which measures how well a business utilises its asset base to generate profit, has doubled since 2013.

The company’s strong cash generation should allow it to participate in further M&A activity. Despite spending €1.9bn on acquisitions in 2017, net debt fell slightly through the course of the year to €5.8bn or 1.8 times earnings before interest, tax, depreciation and amortisation.

The shares trade on a 2018 price to earnings ratio of 14.1-times and yield 2.6%. Davy analyst Robert Gardiner comments: ‘With a balance sheet and cash generating capability that will continue to support the growth strategy, the stock looks undervalued on both a short-term and long-term basis.’ (TS)

NMC Health (NMC) £33.00

NMC Health (NMC) is the largest healthcare provider in the United Arab Emirates (UAE) and is set to benefit from the country’s growing healthcare market.

The FTSE 100 constituent owns and manages over 135 healthcare facilities in 12 countries under its Healthcare division. It also distributes pharmaceutical products, medical equipment and devices, as well as veterinary products via its Trading division.

Berenberg analyst Charles Weston says an ageing population suffering from more diseases is expected to boost the UAE healthcare market in the low double digits.

In the year to 31 December 2017, NMC’s net profit soared 38.2% to $209.2m and sales jumped 31.3% to $1.6bn. Sales growth was roughly split 50:50 in terms of organic means and acquisitions.

NMC recently acquired a 70% stake in cosmetic clinic CosmeSurge for $250m to tap into its high margin, double-digit growth business.

In a bid to expand its foothold in Saudi Arabia, the company also bought an 80% stake in Al Salam Medical for $37m. And it consolidated its position as the second largest player in the global fertility market by snapping up the remaining 49% stake in Fakir IVF. We expect further M&A in the future. (LMJ)

Ferguson (FERG) £53.20

Building materials support service company Ferguson (FERG) has a rich history and more importantly a potentially lucrative future.

Ferguson changed its name from Wolseley in July last year to reflect the dominance of its US division. It has come a long way since being founded in 1887 as The Wolseley Sheep Shearing Machine Company, putting it mildly.

The company distributes plumbing and heating products throughout the US, the UK, Canada and Central Europe. Its main profits come from the US, almost 90%.

Liberum analyst Charlie Campbell says ‘there’s much to like at Ferguson’ including market share gains and margin momentum.

Management come across as conservative when commenting on the outlook, which is something we like.

There have been some investor concerns about increased competition from Amazon which is a risk to consider, particularly from a market sentiment perspective.

However, we note that half of Ferguson’s sales in the US are for bid work, according to Investec. It says tradesmen work hand-in-hand with Ferguson before submitting a bid for a project. That type of close relationship arguably gives Ferguson a market advantage over Amazon. (DS)

DS SMITH (SMDS) 514.6p

There’s a lot of takeover activity in the packaging sector at present as companies seek to build scale against a buoyant industry backdrop. Demand is soaring thanks to the e-commerce boom and an improving global economic outlook.

One company helping to consolidate the industry is DS Smith (SMDS). It produces, collects and recycles packaging and works with some of the biggest names in the consumer goods industry such as Unilever (ULVR), Nestle and Procter & Gamble.

Having made several acquisitions in Europe, DS Smith recently shifted its attention to the US. It has been able to do big deals by leveraging its own scale and borrowing capacity in the knowledge

that debt can be rapidly paid down from its own reliably large cash flow.

Last year it bought Interstate Resources for £722m which was immediately earnings-enhancing. The deal helps DS Smith to expand its international fibre-based packaging business in the US.

A recent trading update highlighted strong volume demand. It’s worth noting that paper prices went up a lot in 2017 and companies like DS Smith are unlikely to have passed these extra costs on to customers immediately. This is a market issue, not a company-specific problem, and DS Smith has a good track record of dealing with such cost pressures. (DC)

MID CAPS

SSP (SSPG) 625p

We like SSP (SSPG) because it serves a captive audience. It has franchise or licence agreements to operate at airports and train stations under many well-known brands including M&S Food, Starbucks, Burger King and Yo! Sushi. Its own brands include Upper Crust and Caffe Ritazza.

Many people waiting for their plane or train may not have the time to go to the high street to find cheaper food or drink, so their only alternative is to use the airport or station facilities typically dominated by SSP or have nothing.

The shares have done well since it floated in 2014 and we believe they’ve got further to travel. SSP is expanding globally, having already cracked Europe where it has more than 30% market share.

Investec analyst Karl Burns calculates that it only has 7% market share in North America, implying scope for significant future gains if it can replicate the European success. ‘Over the last three years, SSP’s North American interests have grown revenue by 30% compound annual growth rate.’

He also reckons there is scope to improve margins in North America and its ‘rest of the world’ territories (these include Asia and Africa and exclude Europe) as they currently sit below the group average.

The shares aren’t cheap, trading on 25 times forecast earnings for year to 30 September 2019. However, we think SSP deserves a premium rating thanks to its impressive growth rates and market position.

It doesn’t look expensive on the EV/EBITDA valuation metric, being 10.9-times. A predator would have to pay a lot more than that level to buy a company of SSP’s position. (DC)

Softcat (SCT) 620p

Softcat (SCT) may sound like cartoon character but in reality it is an important supplier of IT to help organisations run their day-to-day business. It also provides third party enterprise software applications such as customer support, billing, accounting and network security.

Such activities are largely inflation-proof since prices increases are built in to contracts to reflect rising costs.

With limited need for capital it means a large portion of Softcat’s cash flows are returned to shareholders through ordinary and special dividends.

In the two full years since joining the stock market, the company has paid out 27.7p in special dividends, with another 10p to 15p anticipated this year. It has also paid 14.3p in ordinary dividends and is forecast to pay another 9.8p this year.

Forecasts out to 2020 imply compound annual growth of high single-digits in both revenue and pre-tax profit. Analysts at Berenberg believe there is scope to beat these estimates as demand rises.

The investment bank reckons a 20%-plus total return is likely for shareholders on a 12-month view. (SF)

DIPLOMA (DPLM) £10.89

FTSE 250 distribution expert Diploma (DPLM) is a fairly resilient business thanks to operating in different types of industries.

Spanning healthcare equipment to hydraulic seals, the business is diverse and global. While its seals business may be cyclical at the mercy of industrial production, its healthcare business provides some defensive downside protection.

It focuses on supplying essential products that are paid out of a customer’s operating budget (as opposed to capital budget) which results in a high degree of recurring revenues.

Diploma’s recent performance reinforces why this stock should be included in your ISA. For 2017, the company enjoyed 18% revenue growth to £451.9m and 24% pre-tax profit growth to £66.8m.

The company is highly acquisitive and with a strong cash position, £21.9m at 31 December 2017, it has plenty of fire power to bolt on additional companies. Investment bank Berenberg believes future acquisitions could add circa 6% annually to earnings per share between 2018 and 2020.

Some investors criticise companies like Diploma for being overly reliant on acquisitions. However, we believe Diploma’s organic growth record is truly underappreciated. Berenberg last September worked out that its organic growth had averaged 5% since 2006 and 7% since 2010. (DS)

Ted Baker (TED) £30.94

Investors seeking a high-quality and cash-generative ISA pick should snap up premium lifestyle brand Ted Baker (TED).

Rather than a mere retailer, Ted Baker is a quintessentially British brand with a quirky fashion offering which has barely scratched the surface of its international growth opportunity.

Boasting a terrific long-term track record, Ted Baker’s Christmas performance confirmed the ongoing resonance of the brand with consumers. Retail sales growth accelerated to 9% in the eight weeks to 6 January with e-commerce revenue rocketing 35% higher.

We feel comfortable with Ted Baker’s punchy forward multiple – the shares trade on almost 22 times prospective earnings – given the brand’s healthy scope for long-term growth in the outperforming affordable luxury segments of the global clothing market.

Ted Baker is expanding internationally in measured fashion, successfully using e-commerce to enter new markets. It has taken ownership of the bulk of its wholesale relationships and boasts a profitable and growing licence business.

Liberum forecasts growth in adjusted pre-tax profit to £83.4m (2018: £73.6m) for the year to 31 January 2019, ahead of £94.6m for the 2020 financial year. The broker also projects a 66.5p dividend for the current financial year, rising to 75.4p in the following year. (JC)

SMALL CAPS

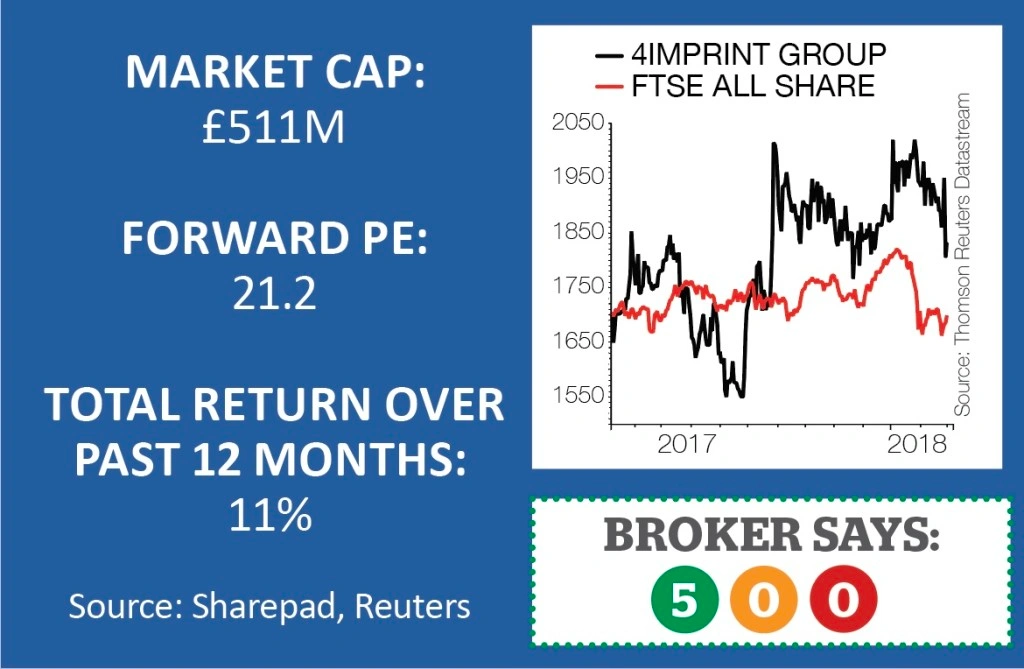

4imprint (FOUR) £18.40

Small cap media business 4imprint (FOUR) sells promotional products like mugs, dongles and pens to companies. It generates 97% of its revenue from the US. The company has a habit of under-promising and over-delivering and generates lots of cash flow.

Earnings are expected to be constrained in 2018 as the company invests $7m in brand awareness to boost its market share. Don’t let

that put you off the stock.

Despite being a leading operator, the company only has a very modest share of a highly fragmented $27bn market across the Atlantic.

The company has invested in technology and has a proprietary order processing platform and uses database analytics to drive efficient marketing to clients. It also outsources the supply of the promotional products which reduces demand for working capital.

The valuation isn’t cheap at 21.2 times 2018 earnings, but this does not seem out of line with the long-term average of around 20 times. Investors who were put off by a multiple of 18 times five years ago, for example, would have missed out on a subsequent 300% advance in the share price.

You need to keep tabs on the performance of the US economy as 4imprint has tended to be closely tied to movements in US GDP. (TS)

Zotefoams (ZTF) 495p

Materials technology specialist Zotefoams (ZTF) is a terrific growth story that is not fully understood by the market.

Zotefoams manufactures lightweight, high-quality polyolefin foams that are durable and strong. These foams can be used in various sectors, including sports, construction and medical, for a range of applications. The company also licenses its MuCell technology to provide stronger and more cost-effective packaging.

It recently formed a partnership with Nike to develop footwear technology and supply materials for its products.

Canaccord Genuity analyst Alex Brooks says overall production capacity will nearly double between the end of 2017 and December 2019. That’s very important given that Zotefoams has previously been limited by production capacity; in 2017 it was largely sold out.

Two expansion projects in the US and UK create big opportunities for the group. The latter involves new autoclaves in Croydon which

are expected to mostly produce Zotefoam’s highest-value, highest-margin product.

Brooks estimates pre-tax profit will jump 89% over the next three years, which is well ahead of market consensus.

If the analyst is correct about the rapid growth then Zotefoams definitely deserves its current high rating, trading on 27 times 2018’s forecast earnings.

Admittedly you are being asked to pay now for future growth, but we’re convinced this business is going places and could even become a takeover target. (LMJ)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- AJ Bell customers given priority access to company’s IPO share offer

- An increasing number of investment trust dividend heroes

- Spring Statement reveals (slightly) improved economic picture

- Gem Diamonds is on a roll with high quality discoveries

- Time is running out for GKN shareholders to vote on Melrose takeover offer

- Labour strike risk could lead to higher copper price

- Why is the dollar struggling?

- Big fall in London house prices

- Aviva under fire for plan to cancel high-yielding shares