Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWill the market sell-off prompt investors to look at value investing again?

Does the end of momentum in the UK stock market since February’s sell-off suggest investors may become less willing to pay high ratings for growth and instead look more closely at value plays?

It’s an interesting thought and one that’s likely to become a key talking point among the investment community over the coming weeks.

The past few years have seen many investors eager to buy shares with fast earnings growth, with no regard to valuation. This ‘growth at any price’ mantra was fine while the market was trending upward. Investors may need to rethink their strategy now momentum has stalled.

REAPPRAISING RATINGS

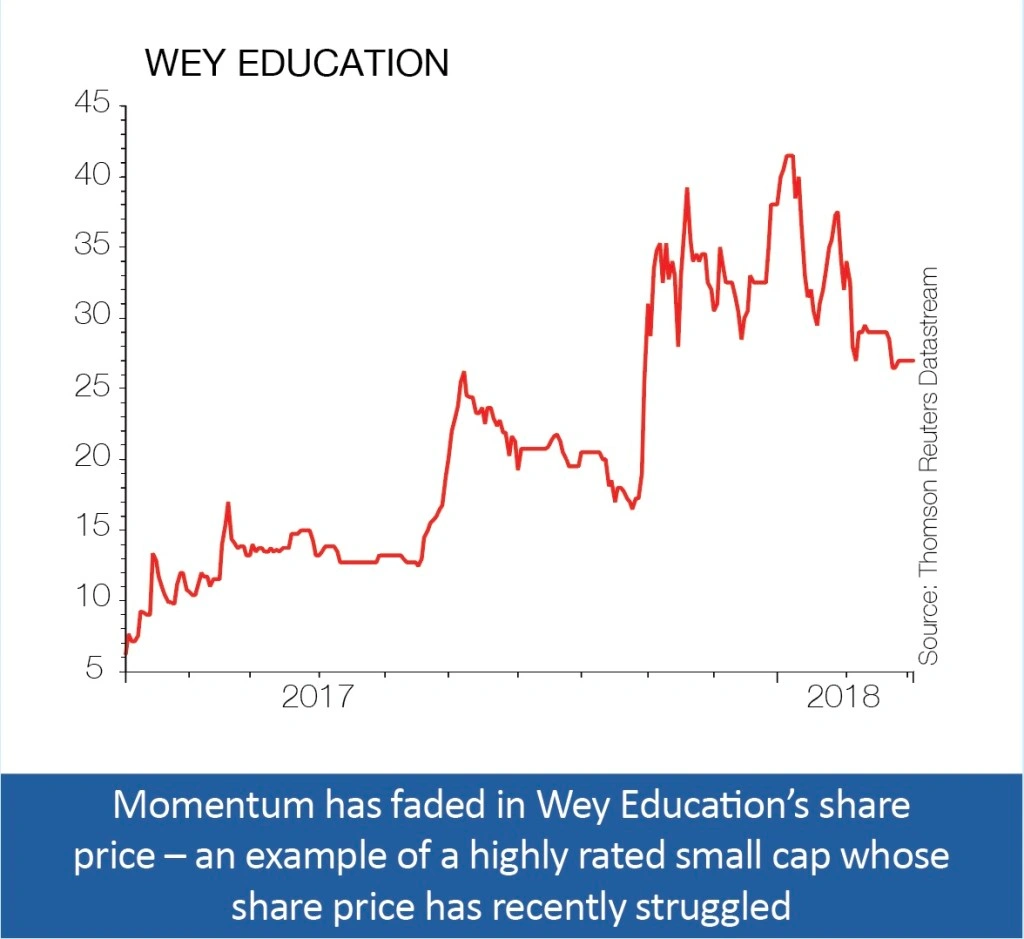

Many small caps trading on high price to earnings ratios have fallen in value since the global market sell-off last month – and they’ve generally not raced back upwards since the sell-off stabilised.

That potentially tells you one thing: that many investors are no longer prepared to pay high multiples to access high levels of growth.

As for large caps, many investors have been paying a steep price for predictability, as evidenced by the high ratings on which many defensive companies have traded over the last few years.

Highly rated companies are at risk of a de-rating if they cannot deliver decent earnings growth and live up to market expectations.

We’re now seeing numerous companies disappoint the market with their latest earnings announcements and their share prices have been punished.

For example, shares in consumer goods giant Reckitt Benckiser (RB.) last month hit a two-year low after investors questioned whether it was still at risk of falling short on sales targets after a tough year for the firm.

WILL VALUE INVESTING COME BACK INTO FASHION SOON?

Value as an investing style has been out of fashion for some time. However, the UK market is full of value opportunities, particularly domestic-facing stocks which have been partially marked down because of the Brexit risk to the UK economy and the near-term prospects for these businesses.

Simon McGarry, senior equity analyst at Canaccord Genuity Wealth Management, believes 2018 could be the year when international investors become more interested in UK stocks.

He says there is already evidence of this happening with well-known value investors taking stakes in UK-listed companies.

‘Just look at Harris Associates; it has the best track record of any value manager in the US, and it is now looking at UK businesses,’ says McGarry, referring to the fact that Harris recently took a stake in funeral services provider Dignity (DTY) following a major profit warning in January.

‘ValueAct is another example; it has just taken a stake in Merlin Entertainments (MERL),’ adds McGarry.

George Godber, co-fund manager of Polar Capital UK Value Opportunities Fund (IE00BD81XW84), thinks he is in a great position to take advantage of value opportunities in UK equities. He says: ‘Not many people are doing value in the UK which is great for us’.

Godber’s fund has returned 14% in a year.

IS THERE AN OBVIOUS NEXT STEP?

So should you now prioritise investing in value stocks or funds? We believe it is certainly an area worth investigating, however you should also have some understanding of the catalysts that are required to drive a re-rating of a stock and ultimately take it from being cheap to fair value.

McGarry at Canaccord suggests that investors shouldn’t purely follow one style of investing. ‘It’s better to have a blend,’ he says.

Dan Brocklebank, a director at asset manager Orbis, says it would be wrong to adopt a ‘naive value strategy’, namely only buying stocks that are trading on low price to earnings (PE) ratios.

‘You could end up investing in a value trap,’ he says. ‘Stocks can look attractive on a PE valuation metric but they can also be terrible investments.

‘You need a selective approach. Stock picking skills are essential,’ adds Brocklebank.

Investors can either research stocks themselves to ascertain if certain value opportunities are worth pursuing, or they can use the services of a fund manager who has a value tilt.

FUNDS TO PLAY THE VALUE THEME

Examples of funds and investment trusts focusing on the value end of the market include Schroder Income Fund (GB00B5WJCB41) and Fidelity Special Values (FSV).

Run by fund manager Alex Wright, Fidelity Special Values has beaten its benchmark out of four of the last six years, a period where value has mostly been out of favour. That highlights the power of a successful fund manager in being able to pick the best stocks.

Elsewhere, Orbis is considered to be a value-focused asset manager, although by its own admission its funds such as Orbis OEIC Global Equity (GB00BH6XLH54) don’t always hold companies which would sit under a standard value definition.

‘The distinction between value and growth stocks is meaningless,’ says Orbis’ Brocklebank. ‘Every business has a value and a growth rate. It is a dramatic over-simplification putting something into one camp.’

Orbis looks to invest in companies it believes are worth a lot more than their current share price.

‘We start by asking a relatively straightforward question: “How much would a rational buyer pay to own the entire business?” The answer is what we call the “intrinsic value”. This is basically an estimate of how much a business is worth today, based on its earnings and potential for growth in the future,’ says the asset manager.

‘We take a long, hard look at the fundamentals of a business, its structure, market, competitors, and the way it is managed in order to assess its intrinsic value.

‘Over the short term we think a company’s share price can be a pretty poor indicator of its intrinsic value. This is because share prices tend to be influenced by the human emotions of greed and fear, and as such their value can vary considerably over the short term.

‘We look to buy shares when they’re trading well below our assessment of intrinsic value, which often tends to be when they’re out of favour with other investors.’

VALUE IN THE BANKING SECTOR?

Phil Hoffman, head of UK, Middle East and Africa for Pzena Investment Management, likes stocks that have been out of favour. He says ‘we like them as long as we think the problems they’ve faced can be fixed’.

In the banking sector, he owns Barclays (BARC) and Royal Bank of Scotland (RBS). Hoffman believes that value stocks tend to do better when economies are growing, especially true of cyclical stocks such as banks.

He says during downturns, when central banks intervene by lowering interest rates and flooding the market with liquidity using quantitative easing, investors focus on growth stocks.

When interest rates are rising this hurts growth stocks and investors look more at value plays. While the spread between growth and value stocks may be wide in the US, value is not actually doing terribly says Hoffman.

Moreover, it’s the dominance of the tech growth powerhouses such as Facebook, Amazon and Apple which skews the market away from potential value stocks.

EXCHANGE TRADED FUNDS TO PLAY THE VALUE THEME

Value investing is picking up in the passive space as well. Anthony Kruger, a smart beta specialist at ETF provider iShares, says his firm’s iShares Edge MSCI Europe Value Factor ETF (IEVL) is enjoying good inflows.

The product tracks the MSCI Europe Enhanced Value index. iShares use various screens to avoid value traps, such as forward price to earnings and enterprise value to free cash flow.

Kruger also says it’s important to compare stocks within in a sector to find true value.

For instance sectors like utilities will tend to be on a low PE rating but that doesn’t necessarily mean they are under-valued or mispriced.

FINDING GOOD VALUE EQUITIES

For choosing value stocks, Godber at Polar Capital’s starting point is the price to book (PB) of a stock, generally going with those with a multiple of less than 1.0.

He won’t automatically dismiss those companies whose PB ratio is above 1.0 although companies above 1.0 have to contain ‘great attributes’.

Pzena’s Hoffman says that UK stocks are cheap in a global context due to Brexit and the resulting weakness in sterling.

While investors were willing to pay very high multiples for bond proxies in the consumer staples space – this is when investors use equities to get bond-like yields – this arguably has started to end as bond yields rise.

With global growth on the rise, fundamentals are back in favour and so it seems may be value investing. (DS/DC)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Unexpected fall in UK house prices

- Just Eat’s big strategic change will weigh on earnings growth in 2018

- Miton to launch US small cap fund

- Beaufort Securities collapse affects 14,000 clients

- Tesco-Booker deal gets final sign-off

- Ex-Melrose experts float new buy, fix and sell firm Stirling

- Smurfit Kappa bid approach lifts packaging sector

- What the Government’s housebuilding plans mean for the sector

- Why restaurant closures are healthy for the sector’s longer term future

- Brace yourselves for the big weather fall-out

- Businesses are looking for Brexit transition deal