Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

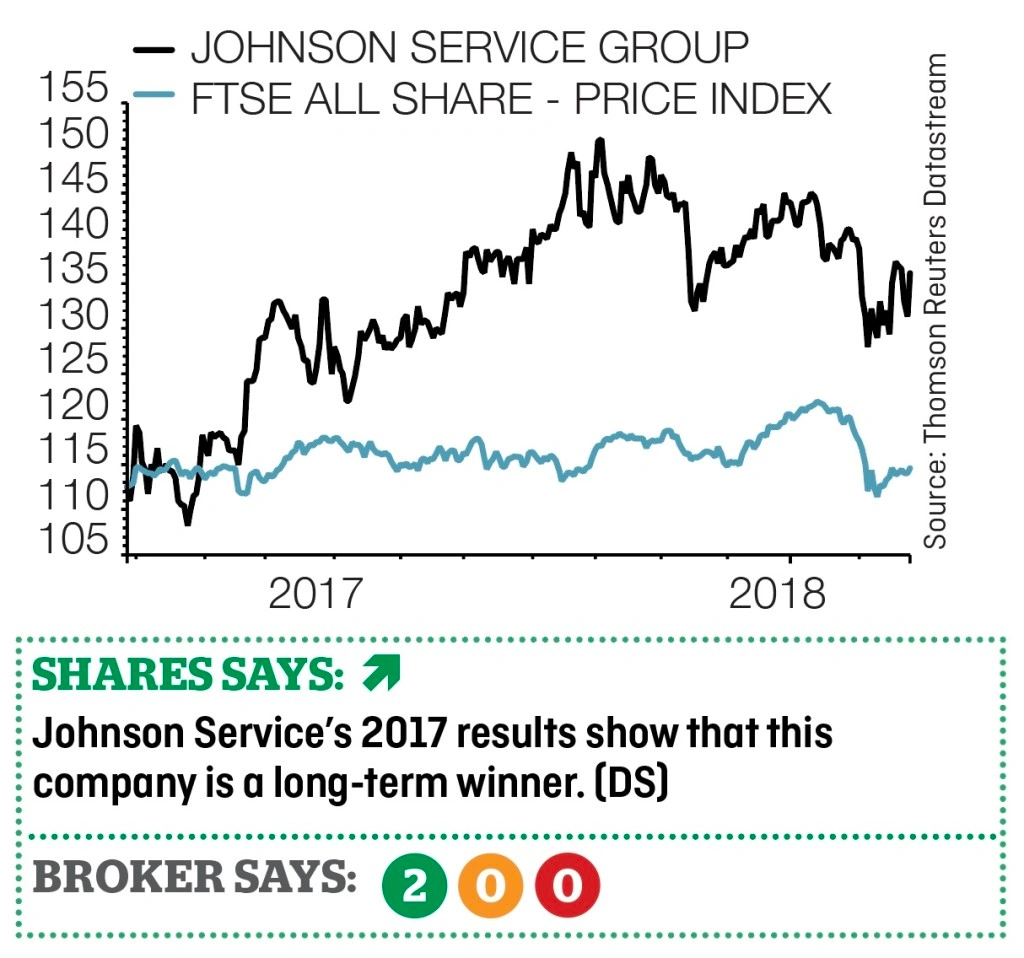

magazineJohnson Service can still clean up

Johnson Service (JSG:AIM) 136.2p

Loss to date 3.9%

Original entry point : Buy at 141.74p, 14 September 2017

Our bullish stance on textile rental firm Johnson Service (JSG:AIM) may not have been rewarded by share price gains yet but we’re still backers of this business. Its 2017 results released on 27 February show a company improving revenue and profit while reducing its net debt at the same time.

Its revenue was up 13.3% to £290.9m while adjusted pre-tax profit improved 17.5% to £39.7m (both on a year-on-year basis).

Chief executive Chris Sanders tells Shares his company’s share of the UK’s hotel, restaurant and catering laundry sector is 27%, or £168m a year.

Johnson has big ticket clients such as BMW and Ford for which it provides and services work wear. Sanders says that the average value of contracts are £36 per week. The company has 34,000 clients ranging from the aforementioned international names to small guest houses.

Sanders also tells Shares that while the average client contract is agreed for three years, it typically retains customers for around 15 years. This implies good visibility on future revenue.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Virgin Money results beat forecasts but doubts over ability to perform

- Lithium miner Bacanora prepares for substantial fundraise

- Greggs’ nourishing performance

- How did investors react to the latest batch of FTSE 100 results?

- Will there be a bidding war for Sky?

- RIT Capital Partners reveals stellar gains since 1988’s flotation

- Triple Point eyes listing upgrade and £200m new cash

- IntegraFin to be valued at c£650m at IPO

- Threads expert Coats impresses on margins and profit guidance

- Productivity growth hits its highest rate since the financial crisis