Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazine10 funds for your ISA

Time is running out to use up your annual ISA allowance. This year the figure stands at £20,000 which is the maximum you can invest across all types of ISAs; and the deadline is 11.59pm on 5 April.

You don’t have to pay any tax on capital gains and dividend income if your investments are held inside an ISA wrapper. If you’re serious about investing, using as much of your ISA allowance as possible each year has to be a priority.

HOW SHOULD YOU FILL YOUR ISA?

Over the coming weeks in Shares we’ll give you some inspiration in the form of fund, stock and investment trust suggestions.

Our articles are designed to give you a head start so you can then go off and research the products further and decide if they’re right for your investment strategy.

We appreciate that everyone has different personal circumstances, so we will split the suggestions into three groups – ideas for people with a lower appetite for risk; ideas for medium risk appetite; and ideas for anyone who is happy with higher risk selections.

All the suggestions are aimed at long-term investors. You won’t find short-term trading ideas.

THIS WEEK’S 10 IDEAS

This article focuses on actively-managed funds. We’ve picked a broad range of products giving exposure to major geographies and different sized companies, as well as choosing some based on the fund manager’s skills and track record.

The next article in our three-part series will be stocks on 15 March, followed by investment trusts on 29 March.

If you don’t manage to take advantage of any unused ISA allowance before 6 April, either because you didn’t have time or any spare cash, all of our selections are valid ideas for investing in an ISA later in the year. The 2018/2019 ISA allowance limit stays the same at £20,000.

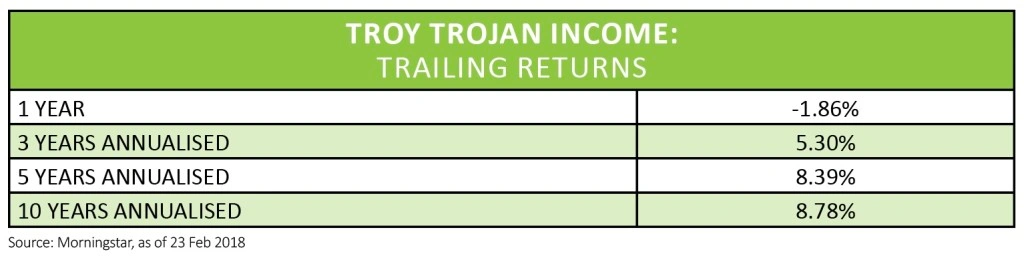

TROY TROJAN INCOME (GB00B01BP176)

This fund is run by Francis Brooke who has consistently applied a well-defined, conservative and low turnover approach, says Morningstar.

It has a bias towards large and mid-cap stocks with a focus on quality, low capital intensity and typically low cyclicality of earnings.

In a nutshell, you’re more likely to see healthcare and consumer staples businesses in its portfolio than high risk sectors like mining.

The portfolio currently includes Lloyds Banking (LLOY) which last week reported a 24% rise in annual pre-tax profit to £5.3bn; and pharmaceutical giant GlaxoSmithKline (GSK).

‘The managers view risk as the potential for permanent capital loss and rightly take pride in this strategy’s capacity to provide protection in more volatile periods,’ says research group Square Mile.

We believe Troy Trojan’s conservative approach makes it suitable for investors with a lower appetite for risk, even though it invests in equities which are riskier than cash.

It is an ideal fund to help form the backbone of a diversified portfolio. It’s the sort of product where investing little and often could really pay off over time. Set up a direct debit to feed your ISA and make use of regular investment services which are offered by most investment platform providers.

You can get on with everyday life in the knowledge you have money going to work in the markets via a fund run by an experienced fund manager who won’t take excessive risks.

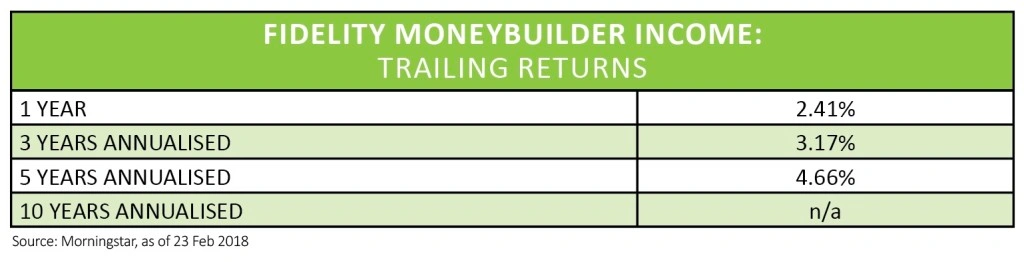

FIDELITY MONEYBUILDER INCOME (GB00BBGBFM09)

Investment grade corporate bonds epitomise low risk investing. Highly rated companies issuing debt are less likely to face any real credit risk or default compared to lowly rates one. This also means that yields are going to be lower than the riskier high yield or ‘junk’ bonds.

Fidelity Moneybuilder Income is a bond fund and has been managed by Ian Spreadbury since its inception in 2005. The asset manager believes corporate bond markets are inefficient which can be exploited by bottom-up fundamental analysis of companies.

Spreadbury is well supported by a group of credit analysts, a quantitative analyst team and fixed income dealers. The diversified portfolio tends to consist of between 250 and 300 positions.

The manager is able to hold up to 5% of the portfolio in non-investment grade bonds, i.e. those rated below BBB-. The fund can also hold 20% in non-sterling bonds, although these are usually hedged back into sterling.

According to research house Square Mile, this fund is ‘suitable for investors seeking a secure but variable income stream with a relatively defensive returns profile’.

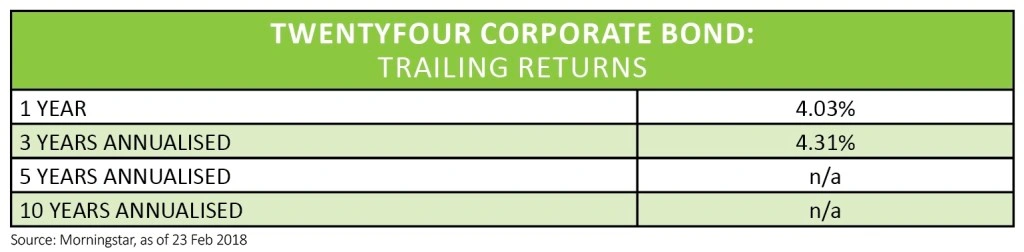

TWENTYFOUR CORPORATE BOND (IE00BSMTGJ19)

Jake Moeller, head of research for UK & Ireland at Thomson Reuters Lipper, says ‘TwentyFour is a vibrant fixed income specialist that made a shrewd hire in (fund manager) Chris Bowie’.

The fund launched on 3 February 2015 and aims to beat the median return of the Investment Association’s (IA) UK Corporate Bond sector by investing primarily in investment grade bonds.

Like Fidelity’s aforementioned bond fund, TwentyFour’s product can go outside the safety of the investment grade universe by investing up to 20% in high yield or floating rate notes which should help boost yields but not take on excessive risk.

Floating rate bonds are perfect in an environment when there is a real possibility of interest rate rises as their coupons should also rise to match any increase. This also offers a level of protection against inflationary forces in the long-term.

Moeller adds that given the dominance of large funds in this space ‘this nimble fund has much to offer’.

Like most funds aimed at the lower risk end of the spectrum, TwentyFour’s bond fund is aimed at capital preservation and income.

INVESTEC UK ALPHA (GB00BJFLDM36)

It is only worth investing in an actively-managed fund if you think the product can beat the market, otherwise you might as well own a passive ETF. Investec UK Alpha seeks to outperform the FTSE All-Share index by 3% to 5% each year.

‘(Fund manager) Simon Brazier arrived at Investec in late 2014 with a strong track record managing core UK equity funds, having delivered outperformance at both Schroders and Threadneedle,’ says Morningstar associate director Simon Dorricott.

‘The consistency of Brazier’s Threadneedle UK fund returns was particularly impressive; his approach has proved resilient through different market conditions. The fund’s risk-adjusted returns were also strong.’

Brazier enjoyed a good start at Investec with the fund outperforming the benchmark by 6.5% in 2015. However, 2016 and 2017 underperformed the benchmark – partly because part of the portfolio contains UK domestic stocks which have been out of favour since the EU referendum vote in June 2016.

You shouldn’t judge a fund merely on a few years’ performance. We’re picking the product because of Brazier’s solid track record over a much longer period.

He’s big on meeting company management and places a large emphasis on analysing a company’s track record, strategy and allocation of free cash flow.

Top holdings include banking group HSBC (HSBA). The fund is also allowed to hold a few overseas listed stocks, which explains why payments giant Visa appears in the portfolio.

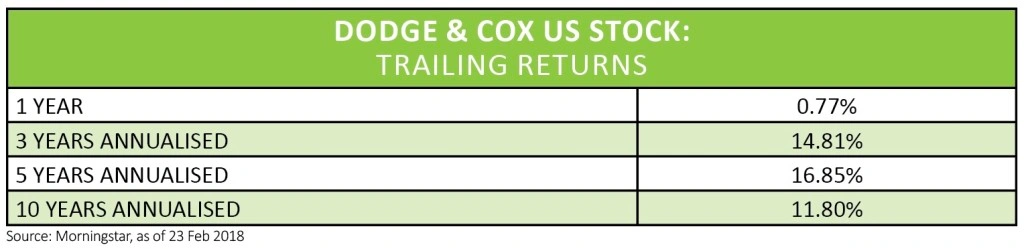

DODGE & COX US STOCK (IE00B50M4X14)

Fund house Dodge & Cox may be relatively unknown outside the US but it has a rich history on the other side of the pond. The strategy behind its US Stock fund dates back to the 1960s.

While some may argue that US equities are overheated given the length of time the markets have enjoyed a bull run, Dodge & Cox’s fund aims to find attractively valued higher quality growth stocks. Long-term growth in earnings and cash flow is recognised as being a key driver of share prices.

Moeller at Lipper comments: ‘The fund’s long-term track record of beating the S&P 500 by identifying undervalued growth is enviable’.

Top holdings include some of the biggest US financial institutions such as Bank of America, Wells Fargo and Goldman Sachs. It also has tech heavyweights such as Google’s parent company Alphabet and Microsoft.

Portfolio turnover tends to be low which means fewer costs for the investor. While building the portfolio of between 60 and 100 holdings around a core of high quality growth stocks, cyclical stocks will be considered if the valuation is viewed as attractive.

FP CRUX EUROPEAN SPECIAL SITUATIONS (GB00BTJRQ064)

Europe is really exciting from an investment perspective at the moment. After years of disappointment, the region is now delivering decent earnings growth, helped by brighter economic prospects. It also benefits from having little political noise and equity valuations aren’t excessive.

FP Crux European Special Situations has been run since launch in 2009 by highly-respected fund manager Richard Pease. He’s an expert on Europe and focuses on market-leading companies with exceptional management and a strong financial position.

These companies should be in a position to generate excess cash which can be reinvested to accelerate growth or returned to shareholders through dividends.

Nearly three fifths (57.7%) of the portfolio is invested in companies worth more than €10bn. One third of the portfolio is in the €1bn to €10bn market cap range; and just below 5% is in the small cap space. The biggest holding is real estate company Aroundtown.

‘We believe this fund’s consistency of management and approach gives it significant appeal,’ says Muna Abu-Habsa, an analyst at Morningstar.

‘The fund has remained less volatile than most of its peers over various time periods and the manager has skilfully made those bets pay as the fund is ahead of its index and peers over his tenure so far.’

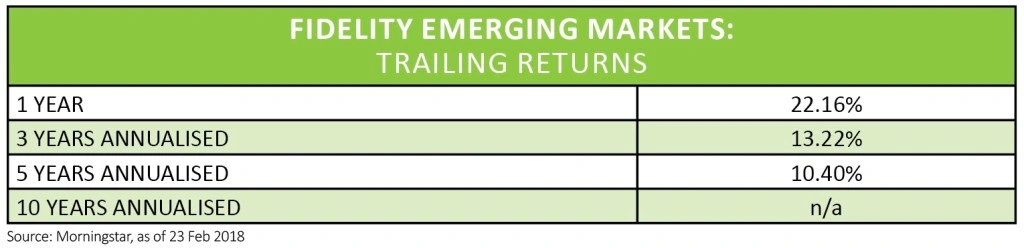

FIDELITY EMERGING MARKETS (GB00B4NTG252)

Fidelity’s product is managed by the experienced Nick Price who leads a team which is responsible for their respective regions.

Research house Square Mile comments: ‘This is a fund that can go through periods of feast and famine’. Moeller at Lipper says it is a high conviction portfolio ‘so expect volatility’.

There are many risks associated with investing in emerging markets such as geopolitical, economic or currency, which is why it is crucial to invest using an experienced manager.

Emerging markets can offer scope for considerable capital gains but investors must recognise this could be a volatile part of an investment portfolio.

Fidelity’s fund will typically hold about 75 stocks although Price can own up to 120 stocks at any given time.

The top holdings include fairly well-known names such as South Africa’s internet and media company Naspers, Taiwan Semiconductors and Alibaba. Less known among the top holdings include Russian bank Sberbank and Inner Mongolia Yili Energy.

Dorricott at Morningstar comments: ‘We consider the fund a strong offering based on the manager’s process and the solid team behind him’.

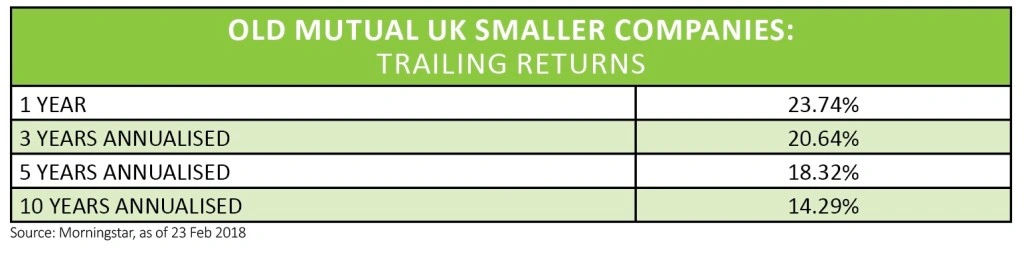

OLD MUTUAL UK SMALLER COMPANIES (GB00B1XG9599)

Smaller companies can be extremely attractive investments over the long term as growth can be higher and faster than larger companies, potentially resulting in very decent capital gains.

However, small caps can also be bad investments if you pick the wrong ones. Working capital issues, insufficient cash flow and setbacks on contracts or other issues can often have a major negative impact on a small business.

As such, it is often worth using the skills of an experience fund manager who is able to spot the winners and avoid the losers.

Dan Nickols runs Old Mutual UK Smaller Companies and is highly rated as a small cap stock picker.

‘He is well experienced in researching UK small cap equities with a career spanning over two decades,’ says Simon Molica, a fund manager at investment platform provider AJ Bell.

‘The investment process is flexible by design which Nickols utilises through his pragmatic approach and can be demonstrated by his inclusion of both growth and value names.’

Molica says the slightly elevated fees are justified for accessing a well-experienced fund manager with a ‘tried and tested’ approach. Ongoing costs are 1.03%.

The portfolio’s top holdings include beverages group Fevertree Drinks (FEVR:AIM) and media events company Ascential (ASCL).

POLAR CAPITAL GLOBAL TECHNOLOGY (IE00B42W4J83)

Polar Capital Global Technology is managed by two very experienced professionals in the tech space, Nick Evans and Ben Rogoff. As technology is an ever-evolving industry, the managers have to keep abreast of all the developments in the sector.

The managers try and see as many companies as possible, with the team attending around 800 company meetings a year. They are also in regular attendance at tech conferences.

Moeller at Lipper says Polar Capital is a ‘genuinely innovative fund house’. He adds: ‘It sees through high-level themes to invest in companies that are genuine technology innovators or established technology leaders’.

Finding the next generation of tech leaders may seem a tall order but if the managers succeed then an investor may be rewarded with considerable gains on their initial investment.

The fund is a great way to access many of the really big names in global tech through a single product, such as Alphabet (Google), Microsoft, Facebook and Apple as well as the Chinese powerhouses Tencent and Alibaba.

You’ll also get exposure to tech stocks further down the market cap spectrum. After all, many of the undiscovered opportunities in this sector will tend to be smaller companies.

Square Mile says the fund managers have a strong sell discipline, setting a price target for each stock.

MAN GLG JAPAN COREALPHA (IE00B62QF466)

Japan is one of our preferred geographies from an investment perspective in 2018 thanks to an improving economic backdrop and attractive corporate valuations.

We prefer active management strategies rather than passive ones in Japan as the country’s main stock market index contains some zombie companies.

Easy credit is keeping many businesses alive – just look at the fact that zero public companies in Japan went bust in 2016. As such, you may be better served using the services of a fund manager who can avoid ‘the walking dead’ and only back higher-quality businesses.

Man GLG Japan CoreAlpha has a large cap bias and is led by fund manager Stephen Harker who has been investing in Japan for more than 30 years. It buys unloved stocks and sells them when they become popular. It is difficult to predict when the latter will happen for each investment, so you’ll need to be patient with this fund.

‘The team’s investment philosophy and process is exceptionally well defined, in that they purely focus on large cap and contrarian ideas which results in a strong value tilt,’ says Molica at AJ Bell. ‘The price to book multiple is their favoured valuation metric in which to identify undervalued opportunities.

‘The team’s ability to stick to this discipline rigorously through time is encouraging, which they have demonstrated over and over again. The resulting portfolio is long term and concentrated in nature.’ (DC/DS)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Virgin Money results beat forecasts but doubts over ability to perform

- Lithium miner Bacanora prepares for substantial fundraise

- Greggs’ nourishing performance

- How did investors react to the latest batch of FTSE 100 results?

- Will there be a bidding war for Sky?

- RIT Capital Partners reveals stellar gains since 1988’s flotation

- Triple Point eyes listing upgrade and £200m new cash

- IntegraFin to be valued at c£650m at IPO

- Threads expert Coats impresses on margins and profit guidance

- Productivity growth hits its highest rate since the financial crisis