Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineBoom time for recruiters

Recruitment companies tend to do well in strong economic conditions. Corporates feel more compelled to hire people and individuals feel confident enough to move jobs, seeking new opportunities.

Upgrades to global growth forecasts last month by the International Monetary Fund (IMF) strengthen the outlook for recruiters. The new global forecast has been lifted from 3.7% to 3.9% for both 2018 and 2019. It also constitutes faster expansion than previous years (3.7% in 2017; 3.2% in 2016).

Growth is widespread. The IMF says 120 economies, accounting for three quarters of world GDP, have seen a pick up in growth in year-on-year terms in 2017, the broadest synchronised global growth upsurge since 2010.

This presents a strong backdrop for recruitment companies with interests in multiple countries. Fortunately for UK investors, the majority of the mid and large cap London-listed recruitment agencies have global interests and aren’t solely dependent on the UK to make money. The IMF didn’t upgrade the UK’s growth forecasts for 2018, leaving them flat at 1.5%.

While the IMF noted that advanced economies were doing well, these regions paled in comparison to developing powerhouses in Asia. China has been the growth story of the last decade but is now being challenged by India as the country’s reforms bear fruit. The fund says ‘the region [Asia] continues to account for over half of world growth’.

PAGEGROUP’S GLOBAL ADVANTAGE

Recruitment consultant Pagegroup (PAGE) has operations in 36 markets across the globe and 82% of its revenue comes from outside the UK, a point of note considering the IMF’s pessimistic view of the

UK’s growth prospects.

Pagegroup has transformed significantly since it started as a business. It used to only place accountants. Now the company has candidates from a wide variety of professions. Steve Ingham, CEO, says ‘now we can adapt our model to what suits the market’.

Like most of its peers, it grows organically. Ingham says this is because the markets it is targeting tend to be under-penetrated by recruitment firms so it’s ‘difficult to buy something that isn’t there’.

Its recent fourth quarter results to 31 December 2017 show the company’s profits up 19.3% in Europe, the Middle East and Africa and 14.9% in Asia Pacific. However, the company’s profits were down 2.8% in the UK.

Kean Marden, an analyst at investment bank Jefferies, upgraded his stock rating on Pagegroup from ‘hold’ to ‘buy’ following the fourth quarter results.

He comments: ‘Industry penetration in Germany and the US is increasing, China is now Page’s third-largest individual country, and the Brazilian economy is slowly improving. If synchronised global economic momentum persists then we believe full year 2018 net fee growth could comfortably

reach 12%’.

HAYS IS THRIVING OUTSIDE OF THE UK

Hays (HAS) is the largest UK-listed recruiter with a market

cap nudging £3bn.

Finance director Paul Venables says that outside of the UK all aspects of the economy are good and ‘this is the third year of that trend’. He adds that constraints on capital investment by the company’s clients are lower which creates a ‘more supportive environment’.

Similar to Pagegroup, the vast majority of Hays’ fees come from outside the UK at 77%.

Venables is not overly concerned about a misjudging of the economic landscape. He views any problems will be of a geopolitical nature.

Concerns include the maverick US president Donald Trump and his relations with North Korea as well as the enduring Brexit saga. He is not alone among senior recruitment employees in thinking these as the main risks.

REAPPRAISING THE OPPORTUNITIES

Venables says that at one time US multinationals would have put Europe at the low end of their growth opportunities. ‘Now they see it as the biggest market and are piling in’.

Further evidence of a sector-wide uplift was provided when Hays released its quarterly results to 31 December 2017.

Recruiters are judged by net fee income which is another way of saying gross profit. Hays’ net fee income for Asia Pacific grew in the three month period by 16% while Continental Europe and the rest of the world went up by 17%. Even the UK was positive with 1% growth. Twenty four of its 33 markets grew by in excess of 10% in net fee income terms.

CASH MACHINES

Recruitment companies can be highly cash generative and Hays is certainly no exception. After paying £94.3m in special and final dividends in November 2017 the company still had a £35m cash position at the start of 2018.

HSBC analyst Matthew Lloyd says Hays is a ‘well-managed staffer’ with strong potential for earnings upgrades if UK performance is not as poor as widely modelled.

Robert Walters (RWA) is another major recruiter on the UK stock market although perhaps not of the scale of PageGroup and Hays. Chief executive Robert Walters says: ‘The best thing we did was go international a few years ago and, as we are organically grown, that has taken time and effort.’

While it was certainly a good move, the company is perhaps the odd one out of the major players on the UK stock market as it has almost a third of its profits coming from the UK. However its fourth quarter results show that its net fee income was up by 13% in the

UK on a year-on-year basis.

Its fastest growing market is Japan and the Asia Pacific region achieved the highest proportion of net fee income in its fourth quarter at £33.6m. On a group basis it achieved £90.5m in the three month period.

Investment bank Liberum upgraded its 2017 pre-tax profit forecast for Robert Walters by 10% in December to £38.5m after an unusually strong end to the calendar year.

The positive trend in October and November continued into December with the company announcing 22% constant currency net fee income growth in the fourth quarter of 2017.

SMALL CAP RECRUITERS

While no way near the scale of the aforementioned companies, Empresaria (EMR:AIM) should be another beneficiary of global growth given its coverage. It estimates that 80% of its adjusted operating profit comes from overseas.

The company has 21 brands in 19 countries although unlike its larger peers Empresaria has not found operating in certain parts of Europe plain sailing.

Finance director Spencer Wreford says new legislation in Germany regarding how long a temporary worker can be employed has negatively impacted the company although he remains upbeat. ‘There’s a huge opportunity in the German markets as despite the legislative issues it’s a young market,’ he adds.

The company has exposure to some very high growth markets with limited recruitment sector penetration such as Thailand, Vietnam, Malaysia and the Philippines.

Ian Jermin, analyst at stockbroker Allenby Capital, comments: ‘Empresaria continues to demonstrate the strength of its diversified business model and we continue to look forward to further growth in 2018’.

DIFFERENT VIEWS ON THE SECTOR’S HEALTH

While many people in the recruitment sector believe we are seeing a broad upsurge in global growth, not everyone thinks it is that simple.

Steve Ingham at PageGroup doesn’t believe the whole world is on the up; he should have a good idea considering how many markets the company is in.

He says: ‘The UK is a challenge and Australia is reasonably challenging.’ He also sees tough times in Brazil, particularly given uncertainty around the country’s election this year.

Conversely, Spencer Wreford at Empresaria says: ‘All economic indicators are positive for the first time since the global financial crisis. You’ve got alignment with the largest markets and emerging economies are showing positive GDP forecasts. Even the UK is positive if just barely.’

He concludes that these positive economic indicators ‘should mean a great market for recruitment’.

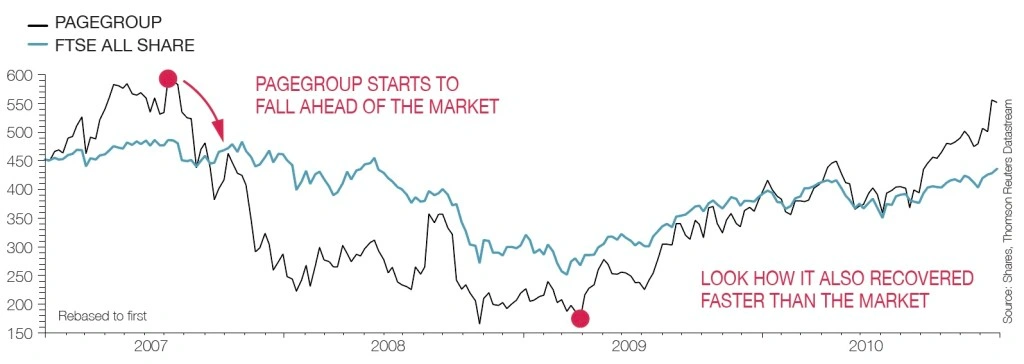

ARE RECRUITERS LEADING INDICATORS FOR THE MARKET?

Recruitment companies should in theory see a rising share price from increased economic activity in their markets. However, the opposite lies true if economic activity eases back.

Recruiters are likely to be among the first to know when life is getting tougher for companies as holding off hiring new people is an easy way to save money. As such, we believe there is a strong chance that shares in recruitment companies will fall before you see the situation reflected in economic data.

That was certainly the case in 2007 when Pagegroup’s share price started falling well before the broader market as the subprime mortgage crisis began. It also started to rise ahead of the FTSE All-Share’s recovery after the global financial crisis, perhaps a reflection of recruiters being among the first to see initial signs of increased activity among corporates.

So if you see shares in recruiters start to fall in tandem, don’t rule out a broader market decline soon afterwards.

OUR TOP PICK OF THE LISTED RECRUITMENT COMPANIES

Hays (HAYS) is our pick of the UK-quoted recruitment firms. At 202p, the global powerhouse trades on 18.4-times 2018’s forecast earnings per share of 11p. The dividend is forecast

to be 3.7p in 2018, implying a 1.8% yield.

Liberum forecasts the company will have £103m net cash position at the end of its financial year on 30 June 2018. That provides firepower to potentially pay even greater dividends than is currently forecast, assuming business goes well in the current year.

Unlike some of its main competitors, it is still maintaining positive net fee income growth in the UK and its performance in its other markets is stellar. For example, in the three months to 31 December 2017, it reported 16% organic net fee income growth at constant currency in Asia Pacific; and 17% growth for Continental Europe and

‘rest of the world’.

Liberum comments: ‘We continue to see Hays as our preferred large cap recruiter given its greater discipline diversity and exposure to the more defensive contract market’.

ONE FOR INVESTORS WITH AN APPETITE FOR HIGHER RISK

Empresaria (EMR:AIM) benefits from having global exposure.

At 110p, the company trades on 8.7 times 2018’s forecast 12.6p earnings per share, supported by a 1.2% prospective dividend yield. Its equity rating is lower than many of the other recruiters due to recent volatile trading conditions and a large increase in net debt to £15.9m at the 2017 half-year stage versus £10.2m a year earlier.

A recent trading update flags strong performance in various parts of the world including the UK with professional services; Japan with the IT sector; and Chile with the retail sector. In contrast, it’s having a tough time with the technical and industrial sector, although not disclosing the countries in which it is experiencing issues.

It has had some problems with a few of its markets underperforming such as the Middle East but it has taken action to remedy this situation.

ONE TO AVOID

We are not fans of Staffline (STAF:AIM) mainly due to its sole UK focus. Its two divisions Onsite and PeoplePlus are both UK-focused and the business is low margin at around 4%.

This means that it has to fill lots of roles to make money and while the business is doing fine at the moment, any decline in the UK economy could have devastating effects.

Investment bank Berenberg describes its outlook as ‘challenging’ and expects cost cutting to help support margins. (DS)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- BP wins the battle of the oil majors

- Shoppers keep calm and carry on

- Four important stories from the past week: Capita, Purplebricks, BT and Vodafone

- Ocado story sours again

- Tesco impresses with profit and dividend guidance

- Weighing up the impact of the market sell-off

- Why Royal Mail’s pension breakthrough is such a big share price catalyst