Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThe dangers associated with special dividends

Special dividends can put a smile on the faces of investors. They are typically generous cash gifts which are sometimes greater in value than normal dividends paid by a company.

We calculate that 120 companies currently in the FTSE 350 index have paid one or more special dividends over the past 25 years, with a noticeable increase in companies making payments over the past five years.

Unfortunately the growing number of companies paying special dividends on a regular basis can also create false hope with regards to future income levels. The payments can also be unwelcome to some investors from a tax perspective, as we explain later in the article.

WHAT IS A SPECIAL DIVIDEND?

Special dividends are typically declared when a company has excess cash to its own investment needs, or when it is sitting on a one-off lump of cash as a result of an asset or business disposal. Some or all of this excess cash is subsequently returned to shareholders.

Special dividends are different to normal (also known as ‘ordinary’) dividends which are a share of a company’s profits passed on to shareholders on a periodic basis, typically twice a year.

The increasing number of stocks paying special dividends in recent years has led many investors to believe they will always be recurring payments. Special dividends inflate the overall cash return to an investor and so the total dividend yield can look quite high on many occasions, potentially 7% or 8%.

Numerous companies, particularly those in the insurance sector, have developed a habit of paying special dividends every year on top of normal dividends. For example, Admiral (ADM) has paid a special dividend every single year since it floated on the London Stock Exchange in 2004.

DON’T DEPEND ON SPECIAL DIVIDENDS

Many investors have got used to receiving special dividends from their investments and assume they will keep getting them in the future, and as such yields will stay high.

In reality, special dividends should only ever be viewed as a pleasant surprise, rather than a sure thing.

Insurer Direct Line (DLG) and investment platform provider Hargreaves Lansdown (HL.) are two examples where investors were caught out with special dividends. Both companies had a long history of paying special dividends yet they both recently stopped paying due to issues facing their businesses.

Direct Line has historically declared a special dividend at its full year results each March but no payment was announced when its 2016 numbers were published on 7 March 2017. The business was derailed by changes to the rules governing compensation for serious injuries called the Ogden rate.

The company did increase its normal dividend by 5.6% and it did pay a 10p special dividend in September 2016. However, the total payment for 2016 was half the level of the previous year (24.6p versus 50.1p), when there were two special dividends.

Hargreaves Lansdown said in August 2017 that it wouldn’t pay a full year special dividend for the first time since joining the stock market 10 years earlier.

It said the business had to retain an additional £50m of capital after the Financial Conduct Authority, a regulator, announced plans to ‘reassess’ Hargreaves’ capital requirements.

‘The revised assessment would mean the group’s regulatory capital surplus during 2018 is insufficient to meet our risk appetite levels if we paid a special dividend for the year ended 30 June 2017 in line with market expectations,’ it added.

SPECIAL DIVIDENDS CAN MAKE UP A LARGE PROPORTION OF OVERALL INCOME

The proportion of overall dividend payments that comes from special dividends can be quite high. For example, 62% of all dividends paid by retailer Card Factory (CARD) in its financial year ending 31 January 2017 came from special dividends.

And nearly half of insurer Beazley’s (BEZ) dividends in its 2016 financial year came from special dividends.

A high weighting towards special dividends means investors could be in for a shock if something goes wrong with such businesses.

Card Factory saw its share price hammered in September 2017 after revealing a 14% drop in pre-tax profit as it struggled with the wider retail sector challenges. Yet its chief executive Karen Hubbard said special dividends were still on the menu thanks to a highly cash generative business model.

TURNING OFF THE SPECIAL DIVIDEND TAP

Beazley said in November the frequency and severity of natural catastrophes in 2017 would affect its results.

The insurer has paid a special dividend every year between 2011 and 2016 bar one, which may have led some investors to expect ‘specials’ permanently going forward. However, analysts don’t believe Beazley will pay one when it reports 2017’s full year results.

Indeed, comments at the analyst meeting after the 2016 financial results were published in February 2017 ‘strongly suggest’ special dividends are coming to an end for Beazley, barring abnormally quiet loss years, said Stockdale analyst Joanna Parsons at the time.

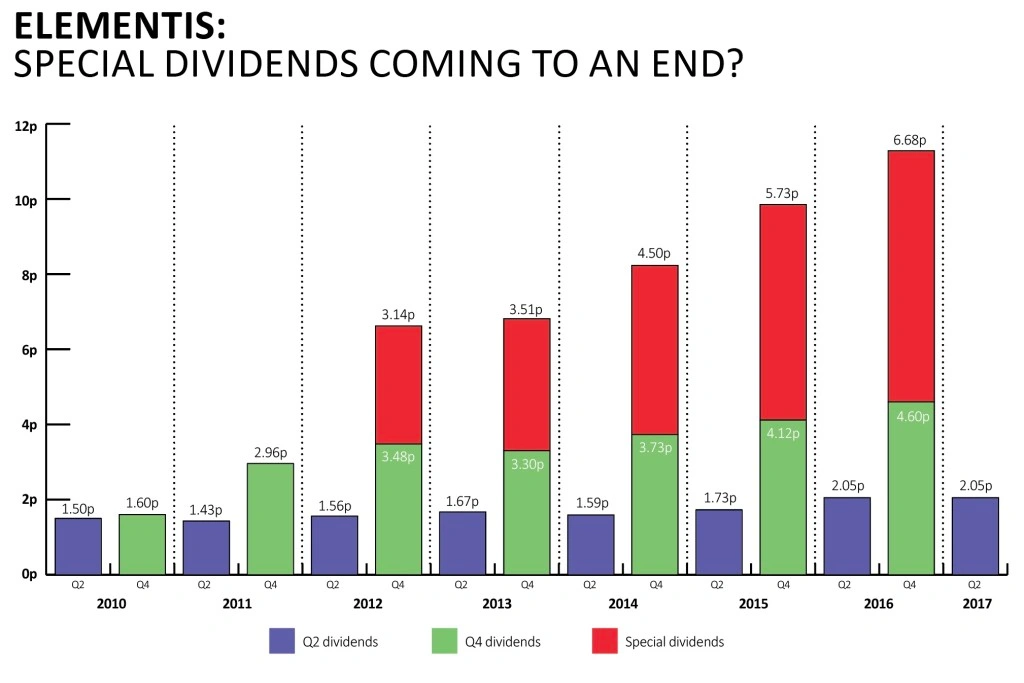

Chemicals group Elementis (ELM) may follow suit, judging by a recent shift in strategy. The FTSE 250 business has paid special dividends every year for the past five years, the latest referring to its 2016 financial year.

Stockbroker N+1 Singer forecasts the total dividend for 2017 to nearly halve to 8.5c (2016: 16.8c). That essentially means the business is going from being an approximate 4.5% yielding stock to one that only yields circa 2.3%. We’ll find out for certain when Elementis reports its full year numbers, expected to happen in early March.

A new management team was installed in 2016 and they’ve expressed a clear willingness to deploy cash to grow the business rather than keep handing it back to shareholders. Elementis has already done one such deal, being the acquisition of SummitReheis in February 2017, and further acquisitions look likely.

THE DOWNSIDES OF RECEIVING SPECIAL DIVIDENDS

The other issue to consider with special dividends is that not everyone wants them due to tax reasons.

In the UK you get a £11,500 personal allowance which is the amount of income you don’t have to pay tax on. On top, everyone is allowed to receive up to £5,000 in dividend income before you have to start paying tax on investments held outside of an ISA or SIPP (self-invested personal pension) wrapper.

From April 2018 the personal allowance rises to £11,850 but the dividend allowance falls to just £2,000. That could potentially result in some investors having to pay tax on their dividends for the first time.

As such, there are a growing number of investors who don’t want special dividends, preferring a company with surplus cash to find other ways to return money such as share buybacks or conducting a tender offer.

National Grid’s (NG.) £4bn disposal of the majority of its UK gas distribution business in 2017 attracted criticism from some investors as £3.1bn of the proceeds were paid as a special dividend and thus triggered a tax bill for many shareholders. (DC)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Is Mothercare a takeover target after share price slump?

- Dialight banking on new leadership

- Coal hits one-year high

- Eco Atlantic gets Exxon discovery boost

- The week in a minute

- Christmas boost for grocers

- Which UK-listed stocks are affected by US tax reform?

- Where to invest your Worldpay takeover proceeds