Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

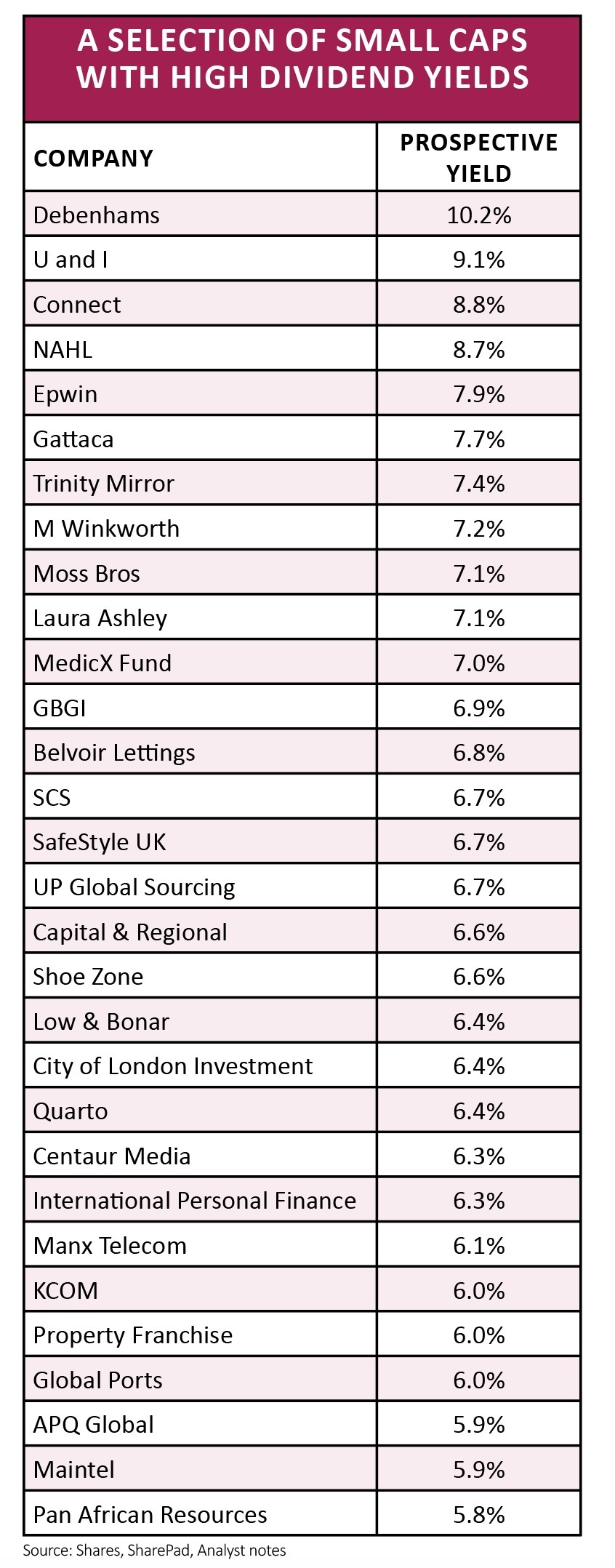

magazineSmall caps with more than 5% dividend yields

You may be surprised at the number of smaller companies which pay dividends. Many investors may assume that dividends are only the domain of mid and large caps, yet we demonstrate in this article that you can find plenty of opportunities further down the market cap spectrum.

We’ve analysed the market using data from SharePad and found more than 330 companies valued at less than £500m which are forecast to pay dividends over the next year.

Within this group, more than 50 have prospective dividend yields in excess of 5% and we’ll now focus on that segment. Just remember that dividends aren’t guaranteed to be paid and analyst forecasts aren’t always correct.

PROPERTY AND MORE

Property regeneration group U&I (UAI) has a 9.1% prospective yield, boosted by forecasts for a generous special dividend. We explain the investment case for U&I in more detail in the Great Ideas section of this week’s digital magazine.

MedicX Fund (MXF) is a specialist primary healthcare infrastructure investor and yields 7% based on a forecast 6p per share dividend for the year to September 2018. Its portfolio contains 153 modern purpose-built assets such as doctors’ surgeries.

At the moment MedicX’s dividends per share far exceed its earnings per share which is normally a warning sign that the dividend is unsustainable. Investment bank Canaccord Genuity says there is a strategy in place to improve the dividend cover.

‘The investment pipeline is £175m with £90m in Ireland offering relatively attractive yields. The successful conversion of this pipeline into portfolio investments will be an important development for MedicX, and should lead to welcome improvements in both dividend coverage levels and cost ratios,’ said Canaccord on 13 December 2017. Since then, Medicx has spent €7.8m on an Irish medical centre.

APQ Global (APQ:AIM) floated in August 2016 with an objective to invest in companies, currencies and corporate/government bonds linked to emerging markets and achieve 6% dividend yield. It has so far paid 4.5p for the 2017 financial year and said in October that it was on track to meet its 6p full year dividend target.

SERVICE BUSINESSES

Connect (CNCT) has been popular among investors over the years for its generous dividend payments, even if the share price performance hasn’t exactly been great. It operates in the highly competitive world of logistics, distributing newspapers, magazines as well as parcels through its Tuffnells and Pass My Parcel operations.

The business recently sold its books division for £11.6m to focus on its early morning and mixed freight distribution. While an 8.8% prospective dividend yield seems enticing, just consider that parcels distribution is a highly competitive business and Connect has very thin operating margins so little room for error if profits come under pressure.

Personal injury marketing specialist NAHL (NAH:AIM) currently has an 8.7% prospective yield based on 2017’s dividend forecast of 15.9p. Dividends are expected to fall in line with profit as the company adapts to changes to the regulatory set up for personal injury claims due to be introduced in October 2018.

However, the company’s policy of paying a dividend covered 1.5 times by earnings is unchanged and, based on SharePad’s data, this still implies a generous looking yield of 7.3% based on the 13.2p forecast dividend payment for 2018.

AND A FEW MORE

The meat of KCOM’s (KCOM) business is running a copper and fibre optic network in Hull and East Yorkshire, but the company also provides its corporate clients with other communications and cloud services.

This is low-growth, cash generative stuff although there’s a pension deficit to manage. Operational own goals have not helped recent performance but its home network is a cash cow capable of underpinning the dividend for the time being. Analysts forecast 6.1p dividend per share for the year to March 2018 and the same for the following year, implying a 6% prospective yield based on the latest share price.

Investors shouldn’t expect dividend growth until more of KCOM’s customers are on its fibre network, potentially creating cost savings by switching off the copper connections.

Even with a recent share price chart that flows upwards from left to right, Sunderland-based sofas-to-flooring seller ScS (SCS) offers investors an attractive dividend yield of 6.7%.

Shore Capital forecasts dividend improvement from 14.7p to 15p for the year to July 2018, ahead of 15.3p in 2019 and 15.5p in 2020. Flagging ScS’ strong free cash generation, net cash pile and committed debt facilities, as well as competitively priced products and variable costs that breed resilience, the broker believes the dividend is sustainable. (DC/TS/JC/DS/SF)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Is Mothercare a takeover target after share price slump?

- Dialight banking on new leadership

- Coal hits one-year high

- Eco Atlantic gets Exxon discovery boost

- The week in a minute

- Christmas boost for grocers

- Which UK-listed stocks are affected by US tax reform?

- Where to invest your Worldpay takeover proceeds