Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineDigital disruption: how to invest in game changing companies

Disruption is everywhere. Changes to established industries and employment dynamics are shaking to their foundations almost every aspect of life.

Customers are constantly looking for cheaper, faster and better services, and providers like Amazon, Netflix, WhatsApp, Uber, Airbnb, and many others, are among the companies with a solution.

The transition is happening in so many places; from transport to energy, communications to healthcare, manufacturing, entertainment, education and even government.

‘This can be challenging, yet it can also bring significant opportunities,’ states Melissa Gallagher, head of investment trusts at Allianz Global Investors.

Disruption implications

When Walter Price, fund manager at Allianz Technology Trust (ATT), first met the Airbnb team he was so impressed that he dumped his stakes in online competitors Expedia and Priceline.

‘Airbnb is an experience more than just a room, so we thought it was a disruptive model, quite a strong model,’ he says.

Even something as simple as the ice cream industry is being disrupted. US-based Eden Creamery makes healthy and natural foods and owns the Halo Top ice cream brand. It has taken around taken around 5% market share, according to Simon Gergel, fund manager of Merchants Trust (MRCH).

‘You can now go through the internet direct to consumers with products that aren’t necessarily in (US supermarket giant) Walmart, allowing disruption of an industry that’s traditionally been very stable and quite highly rated,’ Gergel says.

For example, Harry’s Razors is among the brands taking on the virtual duopoly of men’s shaving held by Gillette and Wilkinson Sword, using the online-only sales channel.

Digital divide

Many experts now think digital disruption has become a binary issue for organisations; adapt or die.

‘Companies are seeing a digital divide, where their fortunes are increasingly determined by the extent to which they succeed or fail to embrace digitisation,’ says Allianz.

‘Those companies that adapt are likely to prove more productive, command higher margins and deliver out-sized growth compared to those that cannot.’

Transformation leaders

There’s no doubt that, when it comes to disruption, Facebook, Amazon, Apple, Netflix and Google (owned by Alphabet) – otherwise known as the FAANG stocks – will have the biggest implications for the majority of investors.

That’s reflected by their vast market values and massive influence on wider stock markets. If we switch the much smaller Netflix for Microsoft, also a highly disruptive enabler ($84.6bn market cap versus $641.9bn respectively), the group represents the five biggest companies on the S&P 500, worth a combined $3.31trn.

Put another way, they represent 13.6% of the index’s value. Considering the S&P 500 makes up something like 70% to 80% of the value of all US stocks, it means these five companies alone are worth between 9.5% and 10.9% of all US stock market value.

Most experts see the US and China leading digital disruption across the globe.

China’s Alibaba is already an online retailer of phenomenal scale, while Tencent’s WeChat platform is taking users far beyond social media.

‘It allows users to talk to their mates, order a taxi, buy a cinema ticket, music or clothes all without the need to visit a third party website,’ explains Chris Sanderson, co-founder of the Future Laboratory, a consultancy that helps organisations prepare for 21st Century demands.

Bubble, what bubble?

This all sound very exciting but many investors are increasingly concerned about runaway valuations. This year the share prices of Facebook, Amazon, Microsoft and Alphabet have each made 30% to 50% gains.

More generally, technology companies recently helped power the S&P 500 index to a record close of 2,594.38 (8 November 2017), fuelling talk of a new tech bubble.

‘Investors always revert back to the dotcom crash,’ says Allianz’s Walter Price.

Yet Price and other fund managers, such as Polar Capital Technology Trust’s (PCT) Ben Rogoff and Herald Investment Trust’s (HRI) Katie Potts, dismiss any notion that we are heading for tech collapse 2.0, in other words a repeat of the massive crash of 2000 to 2003.

Earnings-backed rally

There is a major difference between current ambitious investment multiples versus those of the late 1990s – real earnings.

‘In the technology bubble of the late 1990s, there were no earnings and stock market valuations were based on clicks or eyeballs, or any variety of unusual valuation metrics,’ Price says. This time round technology share prices are rising with earnings upgrades that are outstripping an otherwise low growth environment.

‘While valuations have trended higher, the investment backdrop remains favourable and the prevailing inflation rate remains broadly supportive of current equity valuations,’ says Polar Capital’s Ben Rogoff.

‘Fortunately, the US is experiencing its fastest pace of earnings growth in five years with S&P 500 earnings forecast to increase 10% this year, with potentially more to come in 2018 if the new administration delivers on its tax reform pledge.’

It’s all a far cry from the euphoric ratings of 18 years ago, when Microsoft was valued at nearly 50-times earnings, and Intel and Oracle sported three-digit PEs (price to earnings ratios).

Today Microsoft trades on 23.5 times forecast earnings for its current financial year, according to Reuters data; Alphabet and Facebook trade on 25.8 and 27.0 PE ratios respectively.

The forward PE of the S&P 500 even after its record run stands at 18.2, hardly eye-popping. Even the Information Technology sector part of that index is on a PE of only 19.2.

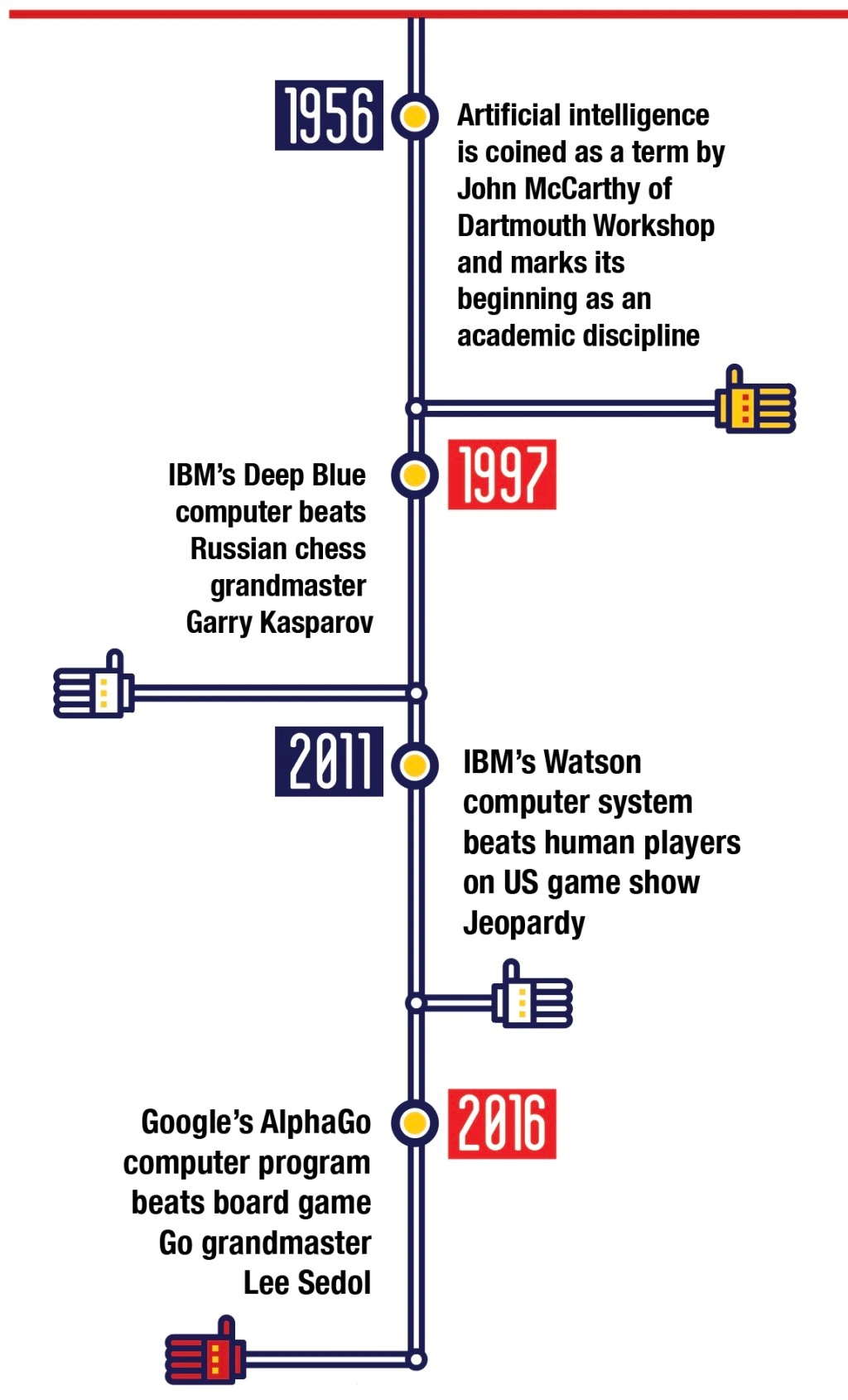

Fourth industrial revolution

‘We are at the beginning of something, not the end,’ says Walter Price at Allianz Technology Trust.

Topics including cloud computing, artificial intelligence (AI), robotics and automation, cyber security and auto technology are some of his pet themes.

‘We are embarking on a revolution,’ he says, ‘the digital revolution’ after steam, electricity and computers.

Concepts such as cloud computing and AI have been around for several years but what’s changed is cheap and plentiful processing power, points out Ben Rogoff. Driving down hardware costs – such as PCs, servers and network infrastructure – has also helped.

‘The new technology cycle appears to have entered a more pernicious phase,’ says the Polar Capital Trust manager. ‘This is likely to prove the beginning of the end of traditional IT with disruption likely to prove significantly greater than witnessed thus far.’

Closer to home

For investors, the disruption investment opportunity raises questions. What will it mean for individual companies, industries and nations? What are the implied risks, rewards and valuations; and how should you position your portfolio?

It is arguably a mistake to think the UK is going to create a technology giant to compare against Google or Facebook – most experts believe it highly unlikely or impossible. But there are plenty of good disruptive businesses listed in the UK; the secret is to hunt for niches.

That doesn’t mean putting money into a crowdfunding initiative involving a Silicon Roundabout start-up. You already have lots of innovative companies listed on the London Stock Exchange.

Just look at the way ASOS (ASC:AIM), Moneysupermarket (MONY) and Rightmove (RMV) have harnessed the internet to shake-up commonplace tasks like buying clothes, an insurance policy or finding a new home.

Industry disruption is ‘majorly important to what we do,’ says Paul Jourdan, one of the founders of Amati Global Investors, a small cap fund manager.

‘I don’t think we should be chasing the next FAANG,’ he says, preferring to seek out UK companies that are ‘changing the way we work, changing our lives’.

He typically looks for opportunities where a company has deep domain expertise within a niche, high growth potential, decent market advantage and has the right kind of financing.

Jourdan’s favourites include virtual queuing specialist Accesso Technology (ACSO:AIM) and gaming services group Keywords Studios (KWS:AIM).

Take aim at disruption

Jourdan is also a fan of Frontier Developments (FDEV:AIM), the online games designer using the internet and social media to publish and promote its products.

Frontier is among the stocks that feature in Herald Investment Trust’s portfolio. ‘In the UK, AIM continues to be dynamic in the micro-cap space,’ says Herald’s fund manager Katie Potts.

Jourdan at Amati also believes AIM offers plenty of opportunities for UK investors to tap into disruptive themes. ‘They are becoming less rare,’ he says, ‘there are more of them.’

Robotic process automation is one emerging area to shake up how organisations do simple administration, freeing up more time for staff to add value elsewhere.

It’s a theme that has rapidly turned Blue Prism (PRSM:AIM) into an AIM sensation, with its share price soaring by more than 1,000% since joining the stock market at 78p in March 2016. Katie Potts has a stake in Blue Prism, so too does Allianz’s Walter Price.

Polar Capital’s Rogoff admits to holding a modest stake in advanced driver assistance systems designer Seeing Machines (SEE:AIM). It has gradually adapted its original kit for big mining trucks and now has consumer cars, trains and planes in its sights.

Price at Allianz says the growth in technology is coming from the creation of new markets, rather than simply GDP growth.

Investors need to find companies generating organic growth by creating new markets or stimulating significant change in old markets.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- The winners and losers on the stock market from Hammond’s Budget

- Lower living costs and higher wages centre stage at this year’s Budget

- What's going on with Royal Mail?

- Accrol: back and kicking up a stink

- Black Friday to bring further retail woe

- EasyJet takes advantage of rivals’ struggles

- Worldwide dividends surge in record high third quarter

- New clean energy fund heading to the market with 4.5% yield

- Ocado growth story turning sour

- Boku hopes to make its mark