Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazinePhoto-Me: putting investors in the picture

One of the stock market’s more unusual investment opportunities, yet highly profitable and awash with growth angles, is Photo-Me International (PHTM).

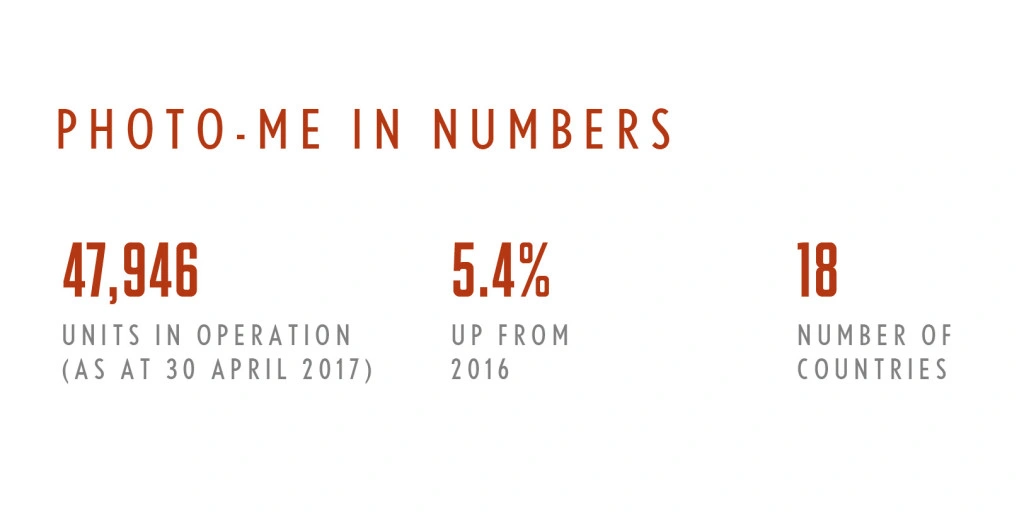

The £644m business operates, sells and services a wide range of instant service equipment. As of 30 April, it had a staggering 47,946 units in operation in 18 countries including France, the UK, Japan and the US.

Generating 90% of its profit outside the UK, Photo-Me’s Brexit-busting credentials should interest income and growth seekers.

In a recent sit-down with Shares, finance director Gabriel Pirona explained how Photo-Me uses the stable cash flow from its long-established photobooth operations to develop complementary products to power growth.

Yes, it operates in some mature business segments

and geographic territories, yet this is a highly entrepreneurial business with myriad competitive strengths and a bright growth outlook.

Competitive strengths

Pirona stresses Photo-Me’s focus on getting the best yield from its estate of unattended vending machines and highlights low fixed costs.

‘We have the same engineers, around 700 globally, and the customers are the same type of customers,’ says Pirona. The company benefits from economies of scale with a geographical coverage that allows it to run machines with superior levels of up-time and at a lower cost than smaller rivals.

Other key competitive strengths include brand recognition – household name brands include Photo-Me in the UK as well as Photomaton and KIS in France – and long-term ties with retail venue/sports location/public area site owners in target markets and relentless investment in technology and innovation.

Bright growth picture

Pirona highlights three key areas of growth; Identification (photobooths and integrated biometric identification solutions), Laundry (unattended laundry services) and Kiosks (high-quality digital printing).

Photo-Me has pricing power, being the market leading photobooth operator in France, the UK and other Continental European countries.

‘We’re the number one worldwide photobooth operator,’ he explains. ‘Identification (ID) standards are evolving, the booth is evolving and we’re taking it up the added value chain by adding new services to the photobooth.’

Population growth, increased travel linked to GDP and increasing demand from governments for improved, digitalised security ID, given rising levels of terrorism and fraud, are long-term growth drivers for Photo-Me.

It is taking advantage of the growing market for secure applications for passports, driving licences and other forms of ID.

For instance, Photo-Me’s encrypted photo ID upload technology has been adopted by the Irish government for its new online passport application service – ‘we reduce the fraud rate through that’ – expected to be in 300 photobooths by the end of 2017.

In France, the bulk of its estate has been upgraded to enable secure transfer of digitised photos and e-signatures to ANTS (Agence Nationale des Titres Sécurisés, a national agency linked to the French Ministry of Transport) servers for driving licence applications.

Secure transfer of photo ID and biometric data direct to government servers is also being trialled in China and progressively rolled out in Germany. Progress is slow in the latter as ‘the production of passports is completely decentralised’.

Bears may point to people taking their own photos via mobile phones as heralding the demise of the photobooth long term. For example, the UK Home Office has already started to allow certain types of photos from mobiles for passport applications.

The good news for Photo-Me is that it has proved very difficult for individuals to provide ‘compliant’ pictures, while the shift towards biometric security equipment rather than mere image capture plays to its technological R&D strengths.

‘We are adding new services to the photobooth and we could make the booth a banking front-end,’ says strategic thinker Pirona.

Awash with potential

Photo-Me’s new SpeedLab digital printing kiosks are being deployed in Europe and the UK, yet it is the laundry arm that should command investors’ attention.

Last year, 1,103 laundry units were deployed and Photo-Me is on track to achieve its target of 6,000 owned and operated units by 2020. It is rolling out its unmanned Revolution-branded laundry business in supermarket car parks and petrol forecourts across France, Belgium, Portugal, Ireland and the UK.

Burgeoning demand, competitive pricing and ‘very limited competition’, plus management’s ability to find attractive locations, mean ‘the laundry business is clearly the accelerator of our growth’, says Pirona.

‘A new smaller footprint unit but with the same revenue potential has just been developed. In Continental Europe this will allow more rapid deployment as it has reduced planning requirements,’ adds Progressive Equity Research.

‘The group is also building on its leased laundrette business where it acquires and refurbishes laundrettes to provide a much more attractive customer offering. It recently entered the market in Japan which the group believes is the largest addressable laundrette market globally.’

Hidden gem

Photo-Me’s formidably strong cash position has enabled the business to move quickly on acquisitions when opportunities emerge.

Recent deals include the acquisition of the Fowler (UK) Laundry business, as well as ASDA’s in-store photobooths.

Group revenue growth is accelerating and is mainly organic gains, says the finance director.

Photo-Me’s pre-tax profit grew by 19.7% to a record £48m in the past financial year on sales up 16.7% to £214.7m with a helping hand from weak sterling.

Underpinned by record operating cash flow, the dividend rose 20% to 7.03p. Photo-Me finished the year flush with £39.2m in net cash and is committed to upping this year’s dividend by the same percentage.

Progressive forecasts £225.3m revenue in the year to 30 April 2018 and £236.6m in 2019. Photo-Me is expected to pay 8.44p dividend for the current financial year, implying an attractive 4.9% yield. This is an essential stock to own. (JC)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.