Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineTesco’s titanic turnaround

Supermarkets giant Tesco’s (TSCO) impressive half year results (4 Oct) confirmed its eagerly-anticipated return to the dividend list after a three-year hiatus.

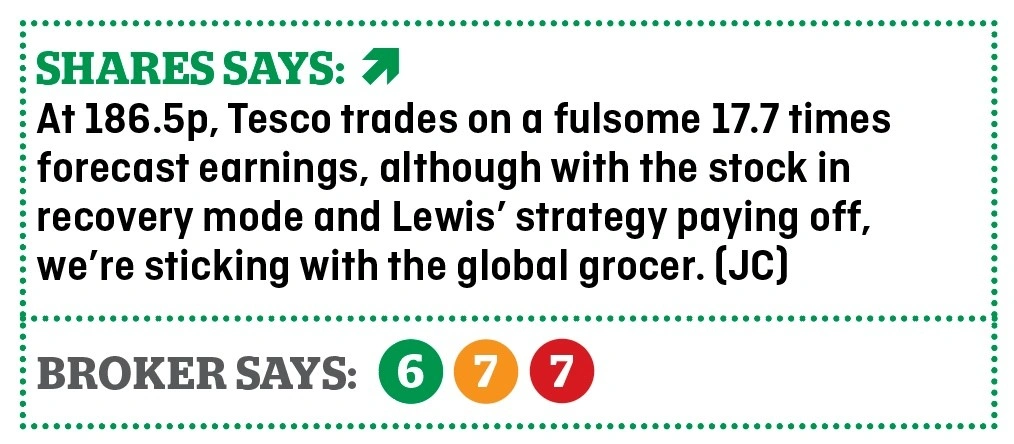

We’d hang on for further gains from the grocer’s turnaround, although we acknowledge the shares have rebounded strongly since June and concerns over a planned £3.7bn merger with wholesaler Booker (BOK) remain.

Dividend resumption

The £15.43bn cap’s half year results proved a milestone, a modest 1p payment demonstrating confidence and CEO Dave Lewis guiding towards a 3p full year dividend.

Pre-tax profits surged from £71m to £562m, operating margins rose to 2.7% and are on track to hit the 3.5-4% target range by 2019/20, while net debt reduced 25.1% to below £3.3bn.

Tesco’s sales inflation in the half was around 1% less than the rest of the market, helping it attract customers back in droves.

Ketan Patel, co-fund manager of the Amity UK fund, explains: ‘As Tesco has the largest market share of 28%, it can afford certain buying powers and can invest these savings into pricing to keep up with the hard discounters.’

In the UK and Republic of Ireland (ROI) business, like-for-like sales grew 2.1% for a seventh consecutive quarter of positive performance. We’re hoping to see continued progress when Tesco reports on Christmas trading (11 Jan 18).

Booker – potential banana skin?

Nevertheless, the medium-term outlook remains uncertain given cut-throat competition between the big players and Aldi and Lidl. The Booker merger is going through the machinations of the UK Competition & Markets Authority (CMA) and some believe Booker could prove a banana skin.

‘However, should it go ahead, we believe the deal presents good value for Tesco,’ counters Patel. ‘The merger will position Tesco as a supplier to the eating out industry and convenience, both of which offer superior growth compared to the food at home its store base serves.

As the largest UK food retailer, Tesco can leverage its scale to cut costs, reinvest in pricing and remain a competitive player and this acquisition will help increase scale.’

UBS has a ‘buy’ rating and 270p 12-month price target that implies 45% upside. For the year to February 2018, analyst Daniel Ekstein forecasts material earnings improvement to 10.56p (2017: 6.32p), ahead of 13.48p in 2019, where a 3p dividend should rise to 5p per share.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Streamlined BAE aims to fly

- Capita announces new CEO

- Online orders heat up Domino’s shares

- Can exploration make a comeback after North Sea oil discovery?

- Where next for the UK stock market?

- Energy price cap threatens Centrica’s earnings and dividend

- Polar launches new megatrends fund

- Christmas comes early for Cranswick