Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

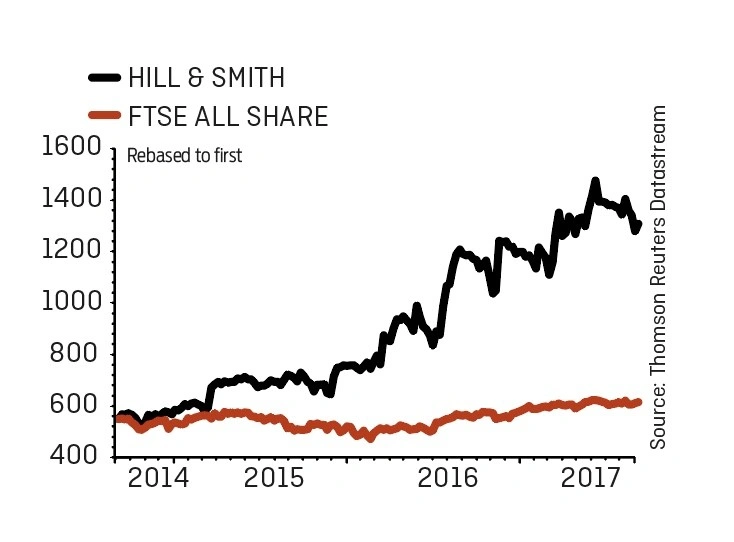

magazineHill & Smith is a dividend growth hero

An infrastructure engineering business might sound about as boring as you get but Hill & Smith (HILS) is a capital growth and income returns story worth knowing. The FTSE 250 member designs, manufactures and supplies a wide array of specialised products needed when new roads and bridges are built, or when big utility projects go up.

Perhaps best-known for its roadside crash barriers, you may have seen them hugging sharp bends in roads, or along the central reservation of motorways, for example. Other bits of kit supplied include street lighting, bridge-side fencing and pipe network support struts used by water companies. It also has a galvanising business that provides zinc corrosion coating protection against rust.

This is a company that has roots as deep as pre-Victorian times, when it was called Hill’s Ironworks. Then it made things like piston rods and wrought iron fencing.

Dull but profitable

At first glance Hill & Smith may sound like a low-tech commodity kit manufacturer, but that is not the case. Its products need to meet stringent safety regulations both here and abroad, and that means they are not easily replaced by cheaper alternatives.

About 78% of sales and 86% of underlying operating profit (on 2016 full year results) comes from the UK and North American markets. The Trump administration’s large infrastructure project investment plans suggests that there is plenty of scope for growth in the US, while Hill & Smith is barely scratching the surface of potential opportunities in places like the Middle East and Asia-Pacific.

Which helps explain the company’s long-run appeal and recent record-breaking operating performance metrics.

Figures for the half year to 30 June 2017 show revenue of £291.8m for the six months compared to £259.3m for the same period a year ago. Operating and pre-tax profit jumped 67% and 73% respectively, although the underlying growth (stripping out one-offs and currency impacts) came in at 21% and 22% apiece, to £38.8m and £37.4m respectively.

The balance sheet is also strong. Underlying operating profit covered net underlying finance costs 27.7-times, according to the company, while net debt of £109.1m is covered nearly 2.3-times by net assets.

And, while cash thrown off by operations declined from £25.6m to £18.7m, first half on first half, it comfortably covered the £10.6m of tax and interest payments for the period. That made £6.7m in dividend payments affordable too.

Enviable income

The payout is important. True, the 2.2% yield based on a forecast 28.5p dividend for 2017 may not stand out. This is partly down to the strong share price rally over the past 18-months or so, as investors piled in on suppliers exposed to big infrastructure spending, particularly in the US.

The underlying income attraction here is the growth rate of the dividend. Hill & Smith has increased its payout every year since 2002, typically in the high single-digits or better. The first half dividend was hiked 11% to 9.4p, which may imply analyst assumptions for the full year payout of 28.5p to 29p per share may be pitched a little on the low side.

Managing the cycle

Perhaps the biggest threat to the company is cyclicality. The company can clearly trade well during periods when national governments are willing to bankroll large infrastructure projects but what happens when the public purse strings are tightened?

Notably, 2009 full year results, which reflect a lot of the fallout from the global financial crisis, do show single-digit declines in revenue and flat underlying operating profit. But pre-tax profit rose and the dividend jumped 15%. This suggests that management know how to manage their way through difficult end markets, streamlining operations and cutting costs to meet a challenging economic backdrop.

There is little evidence of stiffening end markets for now, notwithstanding the current unknowns around Brexit negotiations. At the current £12.88, the stock is trading on a price to earnings (PE) multiple of 17.3 based on Investec’s 74.6p of earnings per share next year. That may not look a screaming bargain but it compares favourably with the 18.9 forward PE of Hill & Smith’s peer group, according to Reuters Eikon data.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.