Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineSix ways to sharpen your investing skills

By Daniel Coatsworth and Tom Sieber

Investing is a continuous learning process. We’re passionate about helping individuals to better understand how the market works and how to spot opportunities and avoid mistakes.

This article details six ways in which you can sharpen your investing skills and get an edge over many other investors. We’ve included lots of topical examples to help you better understand how certain scenarios are playing out in markets at the moment.

DEALING WITH A PROFIT WARNING FROM ONE OF YOUR INVESTMENTS

Keeping a level head and remaining calm is vital when discovering one of the stocks in your portfolio has issued a profit warning and its share price has collapsed.

A profit warning is a broad term to describe a situation when a company is forced to downgrade its earnings guidance. It might have lost a contract, suffered higher than expected costs or experienced a difficult trading period, to name three examples.

What to think about

Understanding the cause of the profit warning is paramount for deciding whether to keep hold of the shares or to get out quickly in case the shares fall further.

One would assume the problem is either the fault of the company such as mismanagement; financial pressures; contract problems caused by a customer; something changing in its industry; or an external event out of its hands such as economic weakness or weather disruption.

Ideally you want to be able to judge whether the problem can be fixed in a reasonable amount of time and what’s required to fix the problem. Equally, you want to know if the risk of owning the shares has increased – specifically, have the chances of permanently losing money increased?

Even if a problem can be fixed quickly, has the company adequate financial power to survive a short-term hit to profit and cash flow? We discuss the problems associated with debt later in this article; for now, think about whether a reduction in cash flow might cause problems paying monthly debt repayments which could put the company in real trouble.

Why Provident's problems are relevant

There are plenty of examples of companies which have issued patchy trading updates which hinted at problems that later manifested themselves in the form of profit warnings. Quite often the clues are laid out well ahead of the share price collapse.

Doorstep lender Provident Financial (PFG) saw its share price fall by two thirds last week after issuing its second profit warning in three months. The first warning was caused by operational changes disrupting the normal flow of business.

Analysts started to question if the dividend would be cut as the company had suffered quite a hit to its earnings. The share price fell nearly 18% on the day to £23.61. At that time, we were told earnings would be lower than previously expected. The company reassured shareholders that it was confident problems would be fixed.

Based on that evidence, you could have taken the view that the dividend may have to be temporarily cut – an outcome that would be bad for the share price on the day such an announcement was made.

Investment bank Liberum raised concerns at the time that operational changes could result in long-term damage to the business. It was also worried about rising impairments, the threat of regulatory intervention to Provident’s industry and the company being over-optimistic with regards to fixing its problems.

With that in mind, it seemed clear (at least in our opinion) that Provident was a ‘sell’ at £23.61 in June. If you’d shared that opinion and exited after the first warning, you would have avoided significant losses in the process as the shares now trade at a mere 900p, following the second profit warning on 22 August which caused its shares to fall 66% in value on the day.

In hindsight there were plenty of clues not to own Provident shares before the big slump last week.

Examining the facts

Sometimes it’s not always easy to spot the severity of the problems without subsequent trading updates to show how a company is dealing with issues.

Other times you might be able to make a judgement with relative ease with regards to the state of affairs. For example, GB Group (GBG:AIM) issued a profit warning last year amid a contract delay.

GB Group said the roll-out of a Government project had been slower than expected. Its share price fell by 26% to 254p on the day.

In reality, analysts hadn’t expected the Verify project (which validates citizens for online interaction with Government services) to make a big contribution to earnings for a while.

Stockbroker FinnCap said at the time that it expected little impact to group profit in either 2017 or 2018 as a result of the delay. Therefore the 26% share price decline was totally unjustified, in our view. As such, we didn’t believe investors should get rid of the shares; in fact, we said at the time to take advantage of the price weakness and buy more stock. That proved the correct call as today they trade much higher at 398.5p.

UNDERSTAND THE MATHS

It’s always a relief when a share price starts to recover from a bad period. Investors should be happy that any losses are being narrowed and hopefully the share price will claw back all the lost territory.

Unfortunately a lot of people underestimate how far a share price needs to travel in order for you to get back to the level it traded before the bad period.

For example, let’s say a share price fell 30% on a profit warning, dropping from 100p to 70p. You would be wrong to assume it needs to rise by the same amount, namely 30%, in order to get back to 100p. That would only take you to 91p.

In fact, that share will need to rise by 43% in order to hit the 100p original price.

The greater the fall, the bigger the recovery required. For example, imagine a share price halved from 100p to 50p, equal to a 50% decline. You would need the share to double, or increase by 100%, in order to get back to 100p.

With this in mind, try not to get overexcited when a share price starts to recover. You may have to wait longer than you think in order to get back on track.

For those investors who incurred a 66% loss on Provident Financial on 22 August when it issued a profit warning, you will need the share price to recover by 196% in order to get back to the £17.45 trading price on the eve of the bad news.

THE WARNING SIGNS TO LOOK FOR IN COMPANY ACCOUNTS

Investors would normally expect the financial results from their investee companies to be trustworthy. Unfortunately, short of outright fraud, there are several measures companies can take to present their financial results and make them look better than they actually are.

Investment bank Liberum has identified 13 accounting red flags in order to spot companies which might have problems now or in the future. Spotting red flags could help you identify companies which are heading towards a profit warning, and enable to get out before disaster hits the value of your investment.

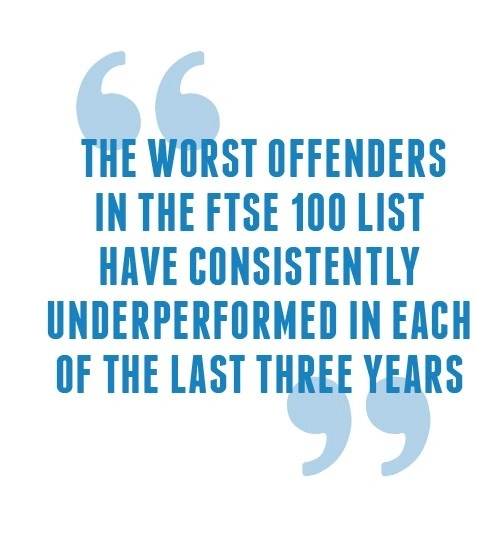

Having previously run this checklist against FTSE 100 companies, analysts Sebastian Jory and James Ashley are now using the flags to examine mid-caps, after dicovering the worst offenders in the FTSE 100 list have consistently underperformed in each of the last three years.

Applying this practically, oil services business Wood Group (WG.) triggers five of the 13 red flags. It has seen a build-up in short-term and long-term receivables days and cash dividend cover is down significantly on its five-year average of 2 times at 0.2.

Capital expenditure is a long way behind depreciation and if operating leases were capitalised it would prompt a material increase in its net debt to earnings ratio.

We now present a guide to 13 of the most important red flags and what they mean.

BE DISCIPLINED

Having decided your goals and limits do not be tempted to abandon them at the first sign of success or failure.

Do not be afraid to sell an investment if it has generated a far higher return than you originally expected, even if it continues to rise in value.

Many people believe a good principle is to ‘run your winners’. We often prefer to lock in a profit on an individual stock when times are good. After all, no one ever lost money from cashing in a profit – but plenty of investors have lost out when they held a stock for too long and it subsequently fell back in value.

Equally if an investment is not working out then you should be prepared to walk away rather than hold out in the forlorn hope of a turnaround in fortunes.

Emotion is the enemy of successful investment. This means you should not keep buying your favourite share in the expectation it will rise indefinitely but nor should you sell at the first sign of trouble. Always take time to weigh up the pros and cons before you transact.

A topical example

When housing and social care provider Mears (MER) warned the Grenfell Tower tragedy would delay some contracts as clients review safety practices (15 Aug) it prompted a share price decline which has seen the stock fall some 10% to 430p. Yes, this news is a setback but don’t forget Mears has a strong record of generating healthy total returns from capital gains and dividends over the long-term.

According to SharePad the total return over the last two decades is 4,570%. It also announced a 5% increase in its first half dividend at the same time as delivering its warnings which suggests management are confident on the longer-term outlook.

Analysts at Liberum share this confidence pointing to increased pressure for better funding for social housing and adding the long-term drivers for the sector including lack of supply and increasing regulation on the private sector remain intact.

Losing fans fast

Another example is takeaway franchise Domino’s Pizza (DOM) which has endured a more dramatic sell-off.

Its shares have lost a quarter of their value since the beginning of 2017 to trade at 267p. This broke a three-year run of steady gains in the share price.

The market seems to be increasingly fearful that the company has reached saturation point as sales in the UK start to slow. A prized growth stock which can no longer deliver growth is susceptible to a lower equity rating and thus its share price could fall. In such a situation you should question why the shares are now worth owning.

DON’T UNDERESTIMATE THE DANGERS OF DEBT

Most listed companies will use debt at some point either to invest in expanding their business or perhaps in acquiring a rival. There is nothing wrong with debt per se but too much of it can be extremely damaging for a company and can leave shareholders counting heavy losses.

We’re in the middle of a bull run for many stock markets around the world including the main ones in the UK. It’s precisely at times like these that investors often forget to think about how a company could survive in tougher times. Debt can be a killer for corporates.

Essentially when a company is borrowing money it is assuming the return from investing that cash will outweigh the cost of servicing the debt.

When earnings are rising, debt can help boost growth and keep a company from either having to dilute shareholders by issuing more shares or alternatively allowing it to retain more of its capital to return through dividends.

If earnings and cash flow come under pressure for some reason then the situation can get ugly fast for a company which has been tempted to add substantially to its borrowings in the good times.

It can lead to breaches of debt covenants (an agreement between a lender and a company on the ratio between earnings and debt) and/or for a company to fall behind on interest payments.

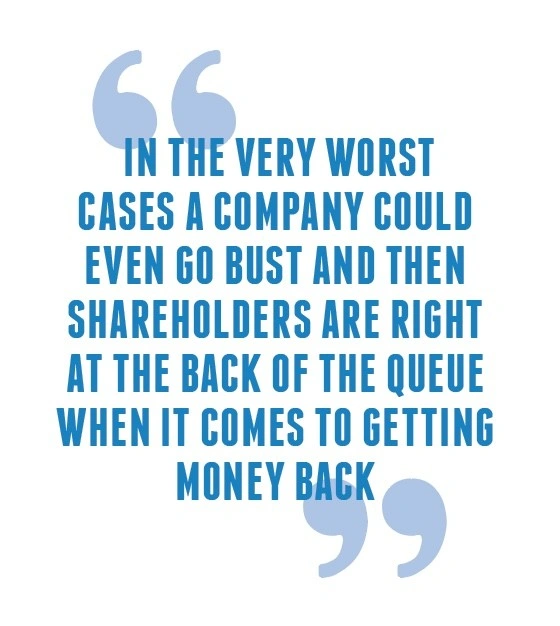

In this scenario, the company may end up being run in the interests of creditors rather than shareholders as debts are paid down.

In the very worst cases a company could even go bust and then shareholders are right at the back of the queue when it comes to getting money back.

The downside of coming out of private equity ownership

Companies which have been owned by private equity and subsequently join the stock market often carry significant debt. Roadside assistance and insurance provider AA (AA.) is a great example. It listed in June 2014 with debt of £3.4bn, although this has since been reduced £2.8bn and the company has reduced its interest payments substantially.

High levels of debt can only, in our view, be justified at companies with very reliable and consistent earnings – but even they are not immune from problems in harder economic times.

Obvious companies which are better placed to cope with higher debt include utility providers where the level of earnings is effectively controlled by a regulator. Another example is funeral specialist Dignity (DTY) where demand for its services is unlikely to fluctuate too wildly.

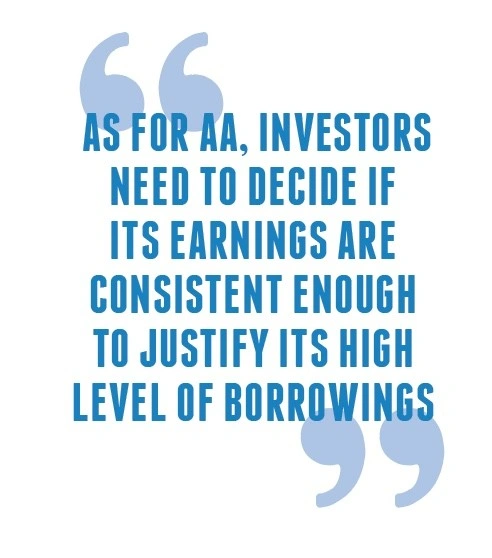

As for AA, investors need to decide if its earnings are consistent enough to justify its high level of borrowings. Yes, it enjoys recurring revenue from membership subscriptions, but trading hasn’t been entirely smooth since it joined the stock market.

Lesson learned from commodities cycle

Miners took on lots of debt when metals and energy prices were rising five to 10 years ago. They have subsequently been hit very hard after a slump in commodity prices put their earnings and cash flow, and thus their ability to service debt, under pressure.

Once a member of the FTSE 100, platinum miner Lonmin has breached its debt covenants numerous times and launched many rescue share placings this decade. It is now a small cap company with a market cap of less than £250m.

Oil explorer Tullow Oil (TLW) was a constituent of the FTSE 100 until early 2015. Tullow’s big debt pile has meant its fortunes are highly correlated to the oil price and since prices began to crater in mid-2014 it has lost more than 80% of its market value and its prized FTSE 100 status. Despite a $750m rights issue in April net debt still totals $3.8bn.

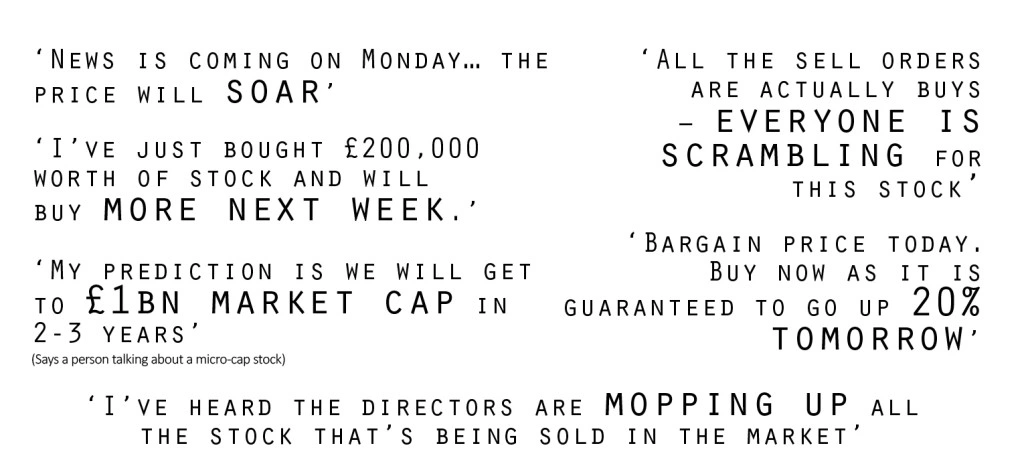

BE CAREFUL WHAT YOU READ… IT MAY NOT BE TRUE OR IT COULD BE MISLEADING

Social media services like Twitter and a variety of investment-focused internet bulletin boards can help you gauge the market mood about certain stocks. They can throw up investment ideas and help you engage in a network of like-minded individuals who are interested in getting a good return from stocks, funds, bonds and more.

As much as they are useful, it is also worth pointing out these online communities can also be dangerous places, principally because the information being disseminated isn’t always factually correct. It is more likely to be opinion and often ill-informed.

The accompanying graphic includes a selection of comments (based on our experience of using Twitter and bulletin boards) which illustrate the type of remarks that should trigger alarm bells.

Essentially we’d be very dubious about anyone saying they’ve heard news is about to be announced; that a certain stock is guaranteed to make you money; or that a company is a surefire takeover candidate.

A company is bound by listing rules to publish price-sensitive information as soon as they have it, so why would a random person on Twitter know about it first? No stock is guaranteed to make you money. Finally, takeover potential is pure speculation.

We suggest you build a list of reputable commentators on Twitter or online message boards based on their previous remarks and analysis, rather than trust the word of anyone discussing a stock or fund in which you might have a shared interest.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.