Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineSUMMER SIZZLERS

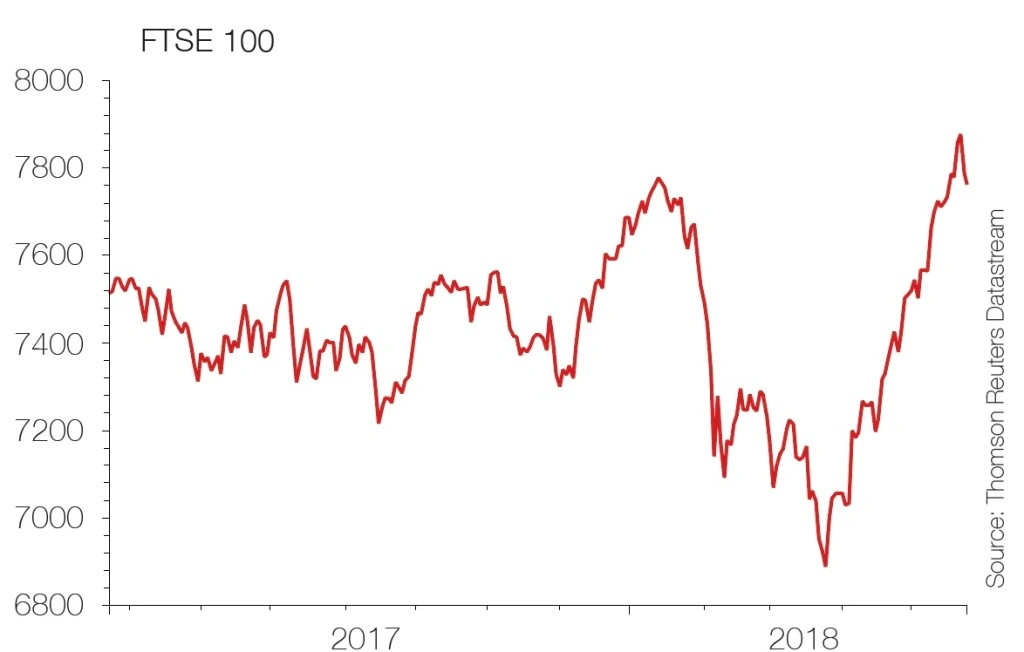

Geo-political tensions aside, the trend for UK stocks has been firmly positive so far in 2017 as investors have shrugged off another electoral shock and ongoing Brexit fallout. That pushed the FTSE 100 index to within touching distance of record 7,547.63 highs until the recent North Korea inspired wobble. Other indicies have performed even more strongly with the FTSE 250, FTSE Small Cap and FTSE AIM All-Share up by 8.7%, 10.4% and 17.6% respectively as we write.

We have run a very simple screen to identify the 100 best performing London-listed stocks. Because smaller companies can be driven higher by just a small number of trades and may be rising from a very low base we have limited our selection to companies valued by the market at £100m or more to ensure we are capturing genuine momentum.

Trend is your friend

Happily, several of the stocks on the list are already constituents of our Great Ideas portfolio. Names like litigation finance provider Burford Capital (BUR:AIM), flavour and fragrance specialist Treatt (TET) and housebuilder Countryside Properties (CSP). We have identified five more stocks which we think can sustain their recent soaraway performance.

Our selections encompass software firm WANdisco (WAND:AIM), cards, gift bags and crackers maker IG Design (IGR:AIM), specialist marketing company Next Fifteen Communications (NFC:AIM), Impax Asset Management (IPX:AIM) and private healthcare provider NMC Health (NMC).

‘Momentum’ investing works on the principle that the ‘trend is your friend’ and typically means buying assets which are enjoying consistent price appreciation. To put it more simply it involves buying what is going up.

Need for catalysts

If a share is going to keep on rising it requires catalysts to maintain investor interest. This could be a drugs trial, drilling result, new contract or positively-received trading or strategy update.

There is a well-worn investor adage that ‘elephants don’t gallop’ but some big names have proved this wrong in 2017. Some due to merger and acquisition (M&A) activity. Payment processing firm Worldpay (WPG) up more than 40% and subject to a recommended £9.3bn frim US rival Vantiv.

The positive outlook which has driven housebuilding stocks like FTSE 100 constituent Persimmon (PSN) and its smaller counterpart Countryside now looks cloudier after reports the Government may scrap the Help to Buy scheme and signs a malaise in the London property market is spreading beyond the capital.

The positive outlook which has driven housebuilding stocks like FTSE 100 constituent Persimmon (PSN) and its smaller counterpart Countryside now looks cloudier after reports the Government may scrap the Help to Buy scheme and signs a malaise in the London property market is spreading beyond the capital.

In contrast, the names we highlight in the remainder of this article still have fuel in the tank and clearly identifiable catalysts which can drive their shares higher.

What is behind the share price momentum?

A massive rebuilding job of investor confidence is the short answer. Two key points have dictated that success; cash and growth. Data replication technology designer WANdisco has attacked its cost base with gusto slashing previously eye-popping cash burn to close to nothing. The company used $600,000 to fund the business in the six months to 30 June, versus $5.3m for the same period in 2016, leaving $9.9m of net cash on the books. Management expects to end the year with positive cash flow from operations.

But that the growth gates have finally opened is just as important to the firm’s long-run chances of success, and an even higher share price. Developing a blue-chip channel partners (including Amazon Web Services, IBM, Oracle) rather than chasing business itself is making all the difference. This has led to its biggest ever single contact worth $4.1m for its Fusion platform, its first ever healthcare deal ($0.65m), and a maiden online retailer agreement, a $2m contract in the US.

These cut downtime in the event of power outages or cyber attacks, for example, hugely important issues for high volume internet business users such as online retailers and banks.

What are the near-term catalysts?

Clearly more new contracts will feed the current optimism, while news of new channel partners of scale will also help. But above all, investors will want to see firm evidence that upbeat talk is translating into meaningful revenue growth. That Fusion booking (future contracted revenue) jumped 173% in the first half is highly encouraging and investors will get more detail at interim results expected in early September.

‘The world has changed – and WANdisco with it,’ rightly predicted analysts at investment bank UBS in January. They also presumed that the shares ‘are due a pause’ after doubling to 400p-odd in 10 days. That latter comment has proven to be a tad too cautious – the stock has since doubled again despite a consensus target price of 465p.

What is behind the share price momentum?

Gift packaging, stationery and creative play products maker IG Design’s (IGR:AIM) strong results and earnings upgrades have driven share price momentum in 2017. Record full year results (27 Jun) were ahead of previously upgraded estimates, a 31% revenue surge to £311m spearheaded by growth in the US and Continental Europe. An especially strong cash performance shifted the balance sheet to a cash positive, debt free position. Brexit-buster IG Design is predominantly an overseas earner with growing geographic and customer diversification. Last year’s acquisition of home décor-to-lifestyle products business Lang in the US added product and augmented a customer roster that includes Costco, Target, Walmart, Tesco (TSCO) and Aldi.

What are the near-term catalysts?

For the year to March 2018, Edison Investment Research’s upgraded forecasts point to normalised pre-tax profits of £20m (2017: £17.1m) and a 5.5p dividend ahead of £22.5m and 6.5p thereafter. Although the shares have re-rerated, further earnings upgrades are likely given current momentum with value retailers in Europe and the US. New customer wins and upside from licensed products (Peppa Pig, Star Wars, Paw Patrol) could spark upgrades. A dramatically strengthened balance sheet means management has flexibility to invest in best-in-class manufacturing and bolt-on acquisitions. An additional catalyst might be dividend surprise, last year’s 80% total dividend hike to 4.5p increased ahead of analysts’ forecasts.

What is behind the share price momentum?

This company’s focus on environmental assets has clearly paid off this year with its assets under management (AUM) hitting £6.9bn at the end of July, around a 50% increase since the start of its financial year on 1 October 2016. Even President Donald Trump’s declaration to withdraw from the Paris Climate Accord should not dent the firm. Impax’s chief executive Ian Simm says Trump’s move has done little to sate investors’ appetite for ‘investments in companies that provide solutions to environmental challenges’.

The firm is riding the wave of increased investor interest in sustainable and environmental assets. These include clean energy, waste management and water which Simm says ‘are growing more rapidly than the main economy’.

What are the near-term catalysts?

These trends show no sign of slowing and the recent publication of climate-related financial disclosures by a task force from the Financial Stability Board should also bolster the company. Stuart Duncan, analyst at Peel Hunt, thinks it should ‘stimulate interest in sectors that will benefit in a low carbon economy over the

long term’.

As more focus is being brought upon resource scarcity, population dynamics and inadequate infrastructure, the firm should expect more earnings growth from well-positioned companies in its portfolios.

What is behind the share price momentum?

The digital marketing firm has a bias towards a relatively buoyant tech sector in the US and strong footprint in California. The client base includes the likes of Facebook, Google’s parent company Alphabet, and IBM. A mix of organic expansion and smart deals have helped deliver strong earnings growth. In April (4 Apr) the company announced earnings per share up 38% in the 12 months to 31 January 2017 and cash from operations more than doubled to £32.8m. Year-to-date the company has made two bolt-on acquisitions and there is plenty of scope for further M&A given limited existing borrowings and the strong cash generation.

What are the near-term catalysts?

Investment bank Berenberg reckons the company can achieve organic growth in the high single-digits from its US business. It comments: ‘Given Next15’s strong positioning, it is possible to see the momentum in 2017 continue into 2018E, which could result in our forecasts being too conservative.’ Based on Berenberg’s current estimates the stock trades on 15.2 times forecast January 2019 earnings. It adds that annual M&A spend of £20m per year could boost its price target from 500p to 650p. Near-term catalysts include half year results in September and news on any further acquisitions.

What is behind the share price momentum?

Shares in NMC Health (NMC) have had a good run thanks to favourable regulatory changes, strong full year results and its looming entry into the FTSE 100.

In July, we reported that NMC has the potential to oust Royal Mail (RMG), which is becoming more likely as its market cap is at £4.5bn compared to Royal Mail’s £4bn.

In March, The Abu Dhabi government decided it would no longer charge people extra to use private healthcare.

The regulatory shake-up is expected to drive earnings before interest, tax, depreciation and amortisation (EBITDA) towards the top end of a range between $335m and $350m in the year to 31 December 2017.

What are the near-term catalysts?

Even this range may be underestimating NMC as Deutsche Bank analyst Marc Hammoud believes the private healthcare firm will hit $356m in EBITDA.

NMC also plans to increase bed capacity from 680 to 1,450 beds over the next three years and deliver specialist services such as in-vitro sterilisation to drive higher margins.

A move into the FTSE 100 at the next reshuffle in September could also boost NMC as funds set up to track the index would have to buy its shares.

In terms of M&A potential, Hammoud says if NMC deploys $500m at the average price to earnings multiple of 14.3 times, it would add an equity value of £1.60 per share, implying a valuation of £28.10.

As shares in NMC are currently £22.05, this implies 21% upside potential.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.