Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineOfficial stats expose great pensions divide

We all know that saving early and often is the key to enjoying a prosperous retirement. But just how much difference can saving in a private pension, such as a SIPP, make to your income in old age?

Figures published by the Office for National Statistics recently shed some light on the different outcomes experienced by those who do save, and those who don’t.

Significant differences

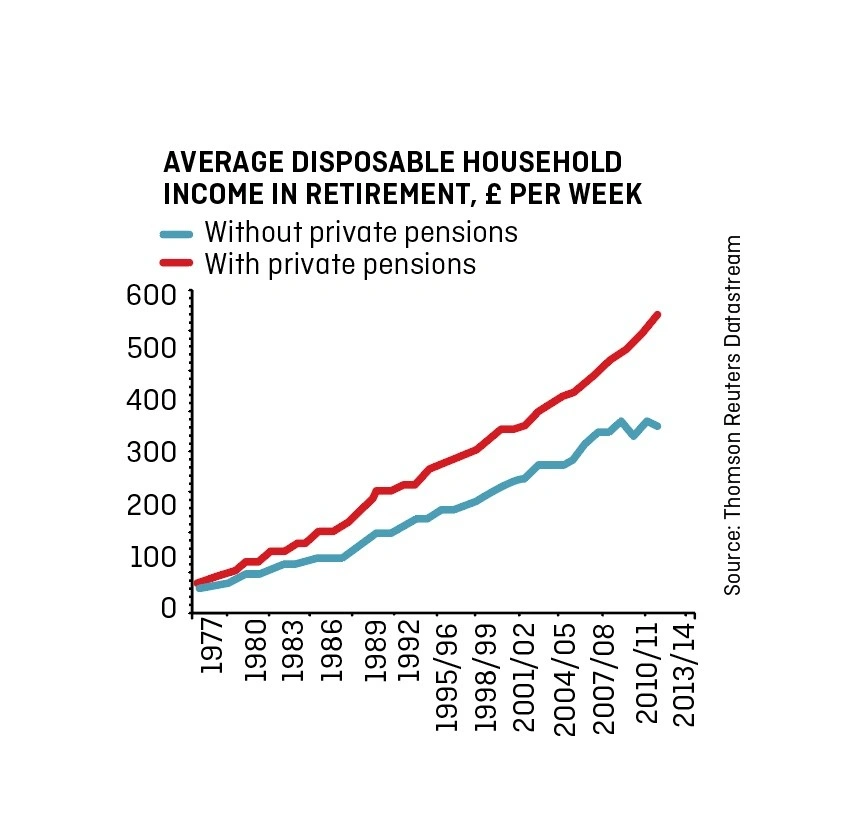

And the difference is significant. In 2015/16, the average disposable weekly income in retirement for a household that saved in a private pension was £534.75 versus just £331.33 for those who hadn’t built up their own pot. That’s a 60% higher income for those who sorted their own retirement compared to those who didn’t and relied on the state.

We can also see from the graph that the difference between the pension ‘haves’ – those who set aside money in a private pot – and the pension ‘have nots’ has grown sharply since 2010.

This is likely to, at least in part, reflect the contraction of the state as post-financial crisis austerity cuts reduce the ability of the state to fill the income void for those who don’t save privately.

But it isn’t all doom and gloom. Membership of private pensions has risen steadily in recent decades, with 79% of retired households now having some private pension income compared to only 45% in 1977. This trend is likely to continue and accelerate as automatic enrolment – which requires all employers offer a workplace pension to staff – is introduced across the country.

For the majority the auto-enrolment minimum total contribution of 8% won’t be enough and the state pension, while providing a useful base income, is not sufficient to cover most people’s costs. This will particularly be the case for those who still have a mortgage to pay off in retirement or need to pay for long-term care.

Long-term care is particularly topical at the moment, with independent estimates suggesting one in four people will need care at some point in their lives and costs sometimes running into tens of thousands of pounds.

Taking ownership

Auto-enrolment only solves the coverage part of the pensions problem. If you want to enjoy a comfortable retirement, you need to take ownership of your retirement and save as much as you can, taking advantage of all the savings perks currently available.

Tom Selby,

Senior Analyst, AJ Bell

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.