Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineNon-Standard Finance continues to grow in sub-prime

The speciality lender sector on the market is full of risks. Failure on the part of borrowers to repay loans being among the most prominent. But Non-Standard Finance (NSF) is a firm growing fast, consolidating the sub-prime lender market at pace.

Chief executive John van Kuffeler tells Shares the company mitigates the the risks of rising impairments by meeting the borrower in person.

Its Everyday Loan business, which is an unsecured branch based lender, is planning to open 53 new branches by the end of the year. This business interviews customers one-on-one, building a relationship and according to van Kuffeler, reducing the risk of impairments.

It is also increasing its focus on the guaranteed loans market, in which an approved third party backs the borrower.

It is also increasing its focus on the guaranteed loans market, in which an approved third party backs the borrower.

The CEO was formerly the chair of beleaguered Provident Financial (PFG) and has capitalised on his former company’s failure to revamp its home collection credit business. He’s taken at least 400 agents who used to work for Provident, following the company’s profit warning in June, decision to force its agents to become full-time staff and axe 2,000 jobs.

Buy and build

The company is a consistent buy-and-build player, its latest acquisition is George Banco, announced on 3 August. The business is the second-largest player in the UK guaranteed loans market.

The deal is expected to complete next month and be earnings enhancing in its first year following completion. The business cost £53.5m.

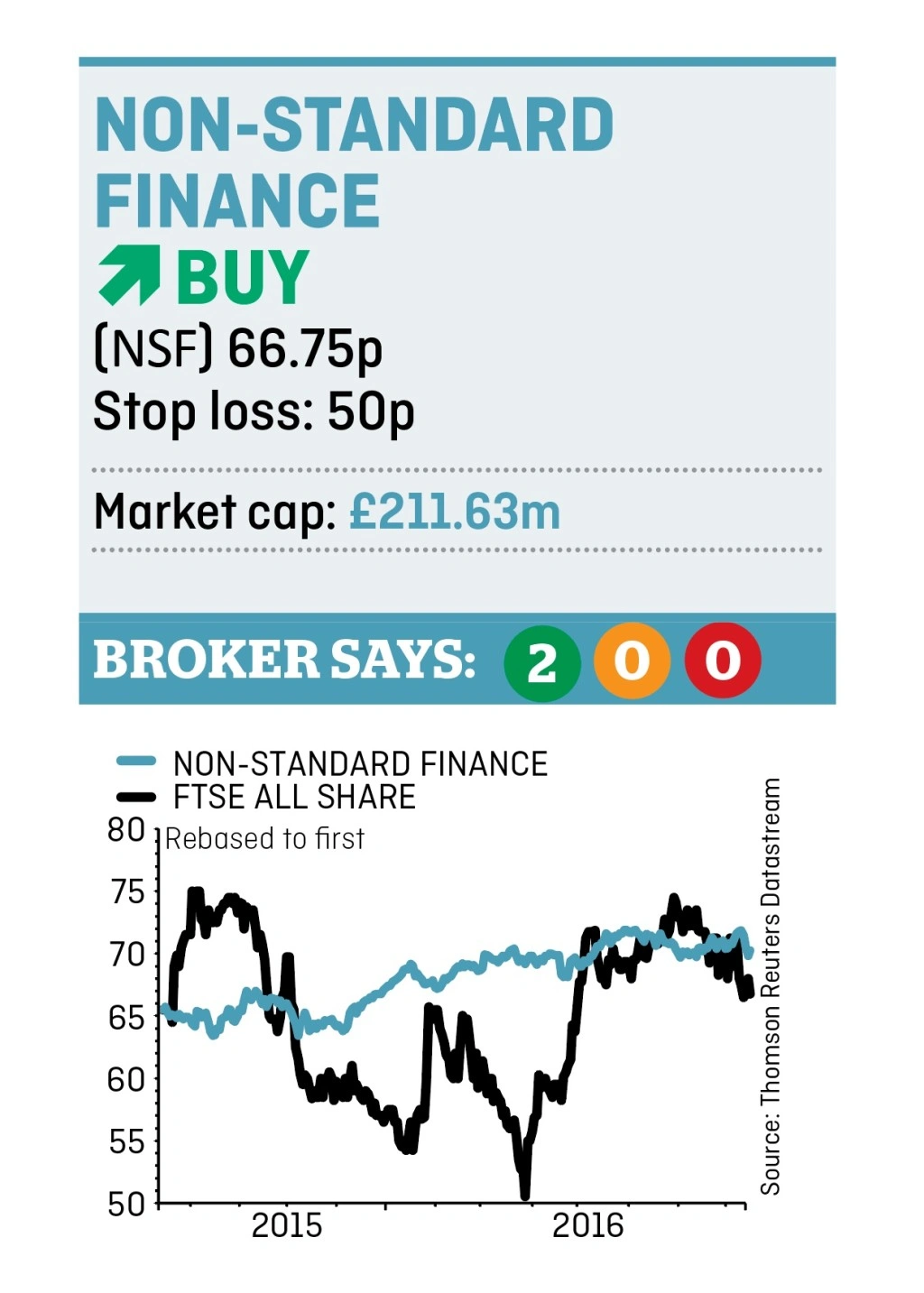

JP Morgan puts a target price of 92p on the stock, implying 37.8% upside.

Non-Standard Finance achieved the unlikely double of increasing profitability while continuing to invest significant sums in the business when it released its half year to 30 June results recently. The firm’s pre-tax profit improved by 26% to £5.4m, while earnings per share were up 15% to 1.35p.

Growing footprint

The company currently has three brands in its stable - Everyday Loans, Loans at Home and TrustTwo - and is soon to add George Banco to that list. With £260m of debt capacity available according to house broker Shore Capital the business is well positioned for further M&A activity.

The UK sub-prime lending market remains pretty fragmented. It is estimated to serve around 10m people. Growth is slowing in the UK and disposable income is getting squeezed by inflation, this backdrop should be helpful to providers of alternative finance, most of which are also highly cash generative.

The valuation does not look too demanding. The shares trade on a forward looking price to earnings ratio of 12.8 using estimates from Gurjit Kambo, analyst at JP Morgan Cavenove. The prospective dividend yield is 3.5%.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.