Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineDechra's animal magic M&A

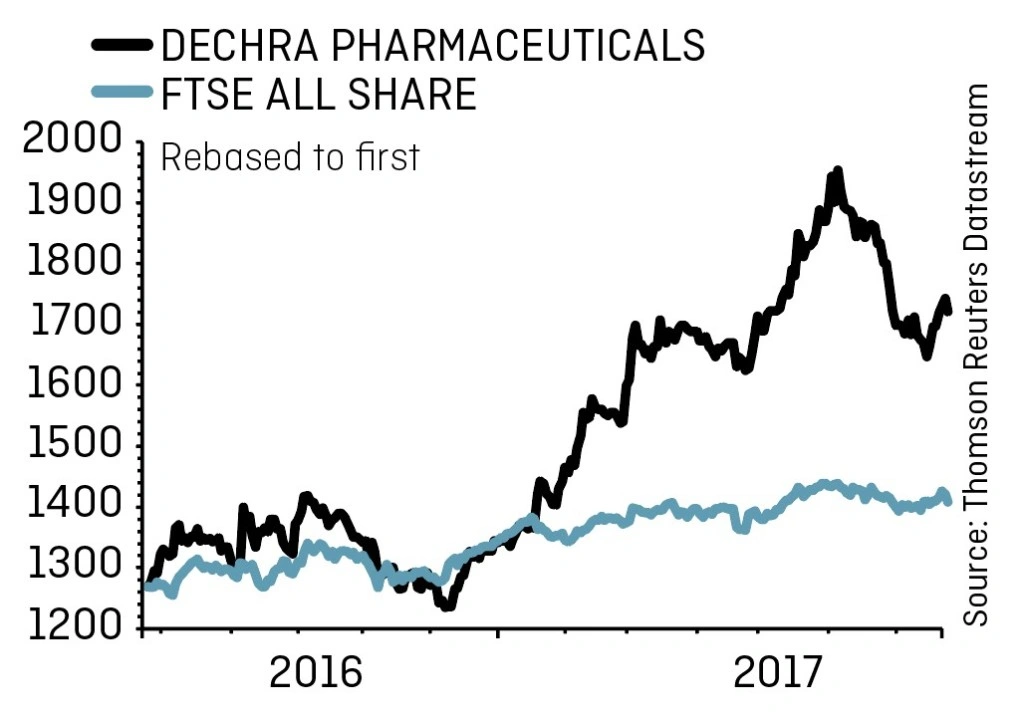

DECHRA PHARMACEUTICALS (DPH) £17.29

Stop loss: £13.83

Market value: £1.6bn

Recent M&A activity has super-charged Dechra Pharmaceuticals’ (DPH) growth prospects and this

should continue to justify a premium valuation.

In the year to 30 June 2017 the veterinary products developer delivered sales growth of 28% underpinned by a 93% advance in the US and the newly acquired Putney – a US speciality drugs developer – should help sustain this momentum.

The deal, which completed last year, will provide immediate access to a high quality product range that complements Dechra’s therapeutic focus areas and adds a new product pipeline.

AMERICAS FOCUS

North America and Western Europe account for approximately half of the global animal health market sales, according to consulting firm Vetnosis.

Stockbroker Stifel analyst Max Herrmann says Putney is a key driver of sales in North America and highlights ‘rapid growth from new product launches.’

One of these products is the antibiotic for dogs Amoxi-Clav, which treats soft tissue infections. This treatment recently secured approval from the US Food & Drug Administration.

Earlier this year, N+1 Singer analyst Chris Glasper noted that Dechra had made it into the top ten of global veterinary pharma groups by sales, flagging acquisitions and organic growth for further momentum.

‘A pipeline of new novel and differentiated generic products is now starting to deliver, with management targeting more than £50m revenue from 45 projects,’ comments Glasper.

Dechra is also expanding into other markets, acquiring Mexico’s Brovel, a manufacturer of pharmaceuticals for dogs, horses and cattle, last year.

It believes it can take advantage of the ‘significant’ Mexican animal health market and use it as a springboard to access other Latin American markets in the future.

VALUATION SHOULD NOT PUT YOU OFF

The biggest obstacle for a prospective investor in the shares is valuation. Dechra trades on a trailing price-to-earnings ratio (PE) of based on N+1 Singer’s forecast earnings per share of 28.9 for the year to 30 June 2017.

However, according to SharePad, this is lower than the average trailing PE of 36.2 times over the last five years, a period which has seen the shares advance more than 250%.

If you had allowed yourself to put off by the high PE over this timeframe you would have missed out on substantial gains.

Investec analyst Dr Andrew Whitney defends Dechra’s premium, highlighting a ‘robust earnings story, an improving cash flow yield and a rich pipeline.’

Pre-tax profit is expected to jump from £71m to £82.7m in the year to June 2018, while sales are forecast to surge from £339.6m to £372.4m over the same period.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.