Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThe contrarian investor

A contrarian investor can be categorised as someone who does the opposite to everyone else. In general, they are looking to buy shares when no one else is interested in a certain stock; and sell when a stock is racing ahead and everyone is buying it with no thought to valuation or risk.

Knowing what to buy or sell isn’t always simple. You shouldn’t just buy the shares which have fallen the most; or sell what’s gone up the most. You still have to undertake thorough analysis to work out what’s really going on with a business.

That’s why we believe all investors should be open-minded, even after you’ve either bought or sold. Read on and we’ll explain why.

In this article we run through six examples of stocks where it might be worth looking at the bad points if a stock has raced ahead; or look for good points if market sentiment is negative towards a particular company.

Challenge the perceived wisdom

Once you have taken a view on a stock, whether positive or negative, it can be difficult to shift your thinking.

Behavioural finance experts call this ‘anchoring’. In other words, becoming fixed on previous information and using that information to make investment decisions that are no longer appropriate.

A good example might be continuing to buy a company which has historically delivered earnings upgrades through difficult economic conditions. What’s to say that trend will always be sustained?

If possible, you should regularly look at investments in your portfolio and ask the question; ‘would I invest in this today at the current price and given current circumstances?’

If the answer is no, or you are unsure, then you should give serious thought to exiting your position and finding a more attractive investment to replace it.

When the market turns on its darlings

When a company which was previously popular with investors hits difficulties the consequences for the share price can be significant.

So-called ‘market darlings’ can suffer big share price falls when they fail to deliver, because up until that point valuation may well have been ignored amid the focus on future growth potential. If doubts suddenly emerge about a continuation of growth at superior levels then valuation comes back into focus.

For example, mobile payments firm Monetise (MONI:AIM) was valued by the market at more than £1bn at its peak in early 2014 but agreed to a takeover at just £70m in June 2017 after the departure of major client Visa contributed to a devastating dive in its share price.

Equally when the market has lost patience with a company and sentiment towards a stock is very poor, the slightest bit of good (or not as bad as feared) news can prompt a big upwards share price movement.

On 14 June marketing services business St Ives (SIV) surprised the market following a string of earlier profit warnings. Its shares rose nearly 40% as the company’s core strategic marketing division saw like-for-like revenue growth of 7% compared to the previous financial year.

Taking a fresh look

In the remainder of this feature we take a fresh look at some of the most loved and hated London-listed stocks.

For the ‘loved’ shares, some of which Shares itself has been a long-running fan, we consider some of the key negative points about the business and for their ‘hated’ counterparts we look the underappreciated positive points. The aim is to stimulate debate and get you thinking in a different way. A good investor is someone who can weigh up both sides of the argument and not solely be influenced by how the market feels towards a particular stock.

Fevertree (FEVR:AIM) £16.05

Current market status: LOVED

Fevertree’s tonic water is increasingly the gin lover’s mixer of choice as it is considered a high quality product.

The company has succeeded in getting its products stocked in a wide range of places, from supermarkets and restaurants to airlines and pubs.

Fevertree has an asset-light, outsourced production model that means it is very cash generative and able to pay a progressive dividend.

Its share price has risen 12-fold in value since joining the stock market in 2014. It has developed a reputation for providing conservative earnings guidance to analysts and subsequently over-delivering when financial numbers are reported. That has led to a continuous stream of earnings upgrades which have fuelled significant share price gains.

WHAT ARE THE NEGATIVE POINTS FOR THE INVESTMENT CASE?

1. Could struggle to crack dark spirit market

It is betting on a repeat of its tonic water success in the dark spirit mixers category. We think that’s a tall order. The market could punish the share price if the company cannot crack this market to same degree as it has done with light spirit mixers.

Gin (a light spirit) and tonic is a refreshing drink where consumers clearly want high quality from both the spirit and the mixer, hence why Fevertree has done so well. However, dark spirits tend to be drunk neat, such as brandy, bourbon and whisky, so no need for fancy mixers.

A mixer could cover up the true taste of whisky, for example, which defeats the object of enjoying that type of spirit. Water or ice would be acceptable mixers for whisky, but you don’t need a Fevertree-branded product.

As for something like whisky and cola, surely that is the preferred drink of someone who is going after quantity over quality?

Fevertree is now selling Madagascan Cola, which it claims to enhance ‘the complex flavours’ of the finest rums, whiskies and bourbons. Convincing shophisticated whisky drinkers to start adding cola to their favourite tipple will be a hard sell, in our opinion.

2. Is the business really worth £1.8bn?

We note that Charles Rolls, one of the company’s founders and deputy chairman, last month sold £73.1m worth of shares. He cashed in £17.3m worth of shares when the company floated three years ago, plus earned £648,000 from Fevertree in pay and bonuses in 2016 alone – so hardly short of cash. Selling a large chunk now sends a negative signal to the market about the company’s future prospects.

3. Main Market plans

We’ve heard talk that Fevertree is going to move to London’s Main Market. The company’s advisers say there are no plans at present, but we see this as a short-term risk to the share price if it does happen. The stock is a popular choice for investors wanting AIM shares that qualify for inheritance tax benefits. IHT portfolio managers would be forced to sell if Fevertree went to the Main Market as the shares would no longer qualify for the tax benefits.

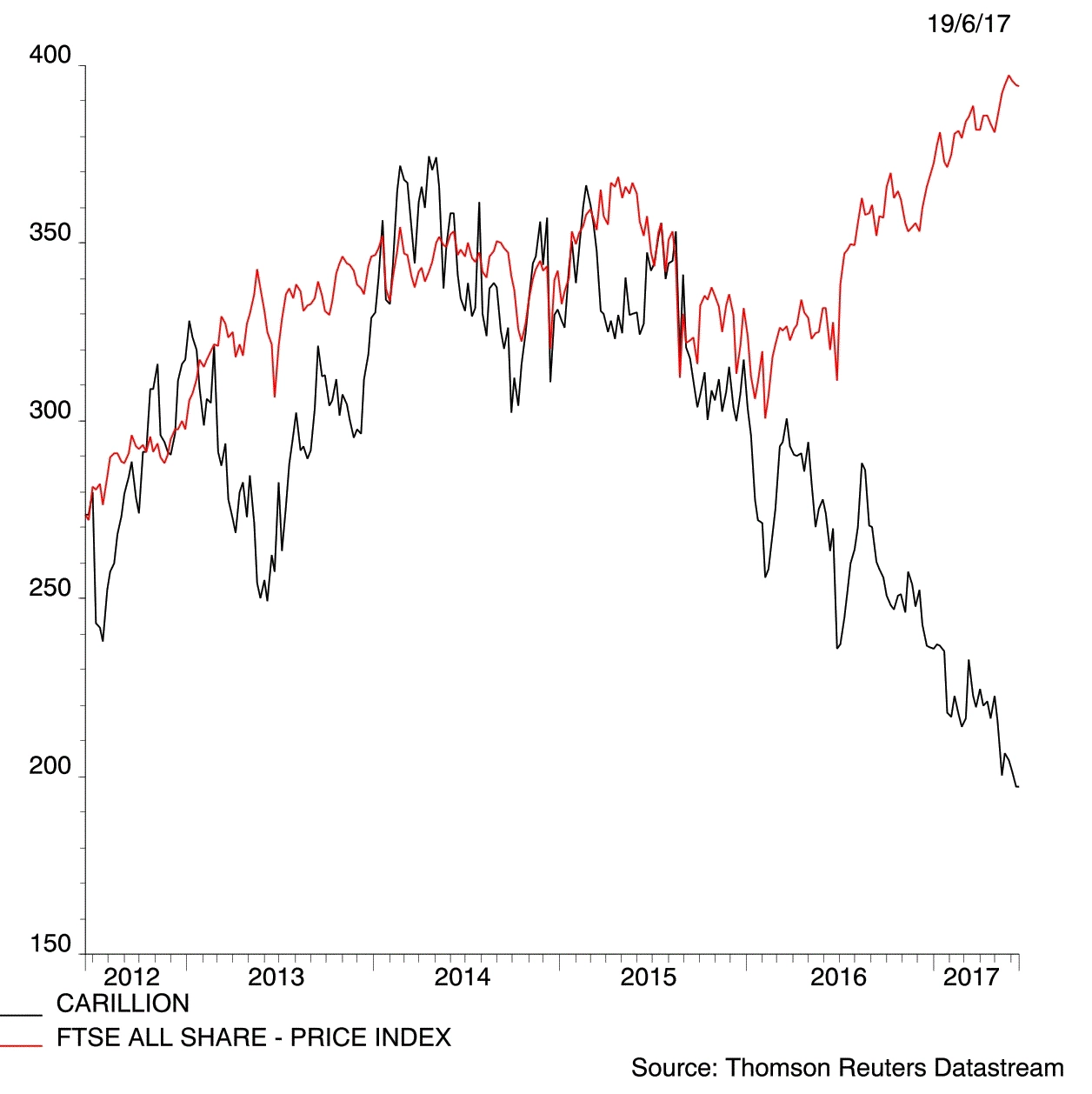

Carillion (CLLN) 199.7p

Current market status: HATED

Carillion is the most shorted stock on the UK market, meaning a large number of investors are betting on the shares falling in value upon which they will make a profit.

Investors with a negative viewpoint are generally looking for weaknesses not yet fully priced in by the market.

In Carillion’s case the main issues are patchy accounting, a strained balance sheet and a difficult macro-economic backdrop.

A £150m convertible bond launched in December 2016 was perceived as an expensive way of securing new capital and there are fears of a dilutive fundraising in the near future.

At the same time the company’s work maintaining railways, roads and military bases has been hit by delays in government spending in the wake of the Brexit vote, a situation which may be exacerbated by the current political uncertainty. Its Middle East business was also hit by the downturn in oil prices a few years ago.

WHAT ARE THE POSITIVE POINTS FOR THE INVESTMENT CASE?

1. Determination to tackle balance sheet issues

The company’s new finance director Zafar Khan, appointed last August, is committed to getting borrowings under control.

Average net debt in 2016 was £587m, the pension deficit was £663m and there was an early payment facility for suppliers of £498m.

Management are incentivised to reduce year end net debt of £219m by up to £50m, which is likely to be achieved by cost cutting, and new means are being sought to handle the £50m annual payment towards the pension deficit.

2. Earnings are still expected to grow

Although the company is operating in a tough market environment, the consensus among analysts is for earnings to still grow in 2018 and 2019. Unlike many of its quoted peers, Carillion hasn’t actually been plagued by profit warnings over the past few years.

The company demonstrated some confidence in the outlook by recently hiking the dividend 1%. Also, despite its recent troubles, the business has a strong position in UK facilities management and is the leading player in this space.

The current forward price-to-earnings ratio of 5.6 times arguably fails to reflect this position. Instead, this very low rating implies Carillion is a business in serious trouble. Perhaps the market is being too pessimistic?

3. Orders are picking up

In a trading update ahead of its AGM in May the company said it had made ‘an encouraging start to the year in terms of winning new business’.

New orders and probable orders worth around £1.3bn had increased visibility on expected 2017 revenue to more than 85%. The company says it will also be more selective to focus on markets and contracts which offer ‘good quality earnings and cash flow’. Notably it exited its construction operation in the Caribbean in December 2016 citing a lack of opportunities which met its criteria.

Ocado (OCDO) 269.2p

Current market status: LOVED and HATED in equal measure

The food delivery group is loved by customers thanks to superior customer service and a great range of high quality products. The share price, however, is very volatile. Bulls ignore a sky-high valuation and say it has the potential to be a global player. Bears says the valuation is too high and progress with international expansion has been too slow.

Why do some people love the stock?

Online grocery facilitator and distributor Ocado (OCDO) has at long last delivered a deal with an overseas retailer to use its ‘Smart Platform’.

A play on channel shift, Ocado runs online delivery services for WM Morrison Supermarkets (MRW) and Waitrose, but its priced-for-perfection rating reflects excitement over the potential for further international tie-ups.

Also at play are reheated bid rumours with Amazon, John Lewis or even Morrisons touted as potential predators.

WHAT ARE THE NEGATIVE POINTS FOR

THE INVESTMENT CASE?

1. Frothy valuation

Ocado’s valuation is ludicrously high; the shares at 269.2p trade on more than 190 times Numis’ 1.4p earnings per share forecast for the year to November 2017.

As for pricing in takeover potential, it is worth pointing out that Jeff Bezos’ Amazon (seen as the most logical buyer) has had ample opportunity to acquire Ocado to date, with no evidence of actual interest.

2. Lack of transparency with new contract win

Disappointingly, Ocado’s first international deal is with an unnamed regional European retailer rather than a global grocery giant.

There’s also a hint of ‘jam tomorrow’ about the tie-up; earnings and cash neutral in the 2017 and 2018 financial years, then ‘increasingly accretive thereafter’.

3. Poor shareholder returns

To paraphrase Shore Capital, Ocado is a shopper friendly business, not a shareholder friendly one.

Sub-scale as a standalone grocer, Ocado has become a pure-play picker, packer and deliverer of groceries for other supermarkets. Indebted, spending heavily and generating skinny margins, Ocado trades without dividend and operates in an industry where competition is cut-throat.

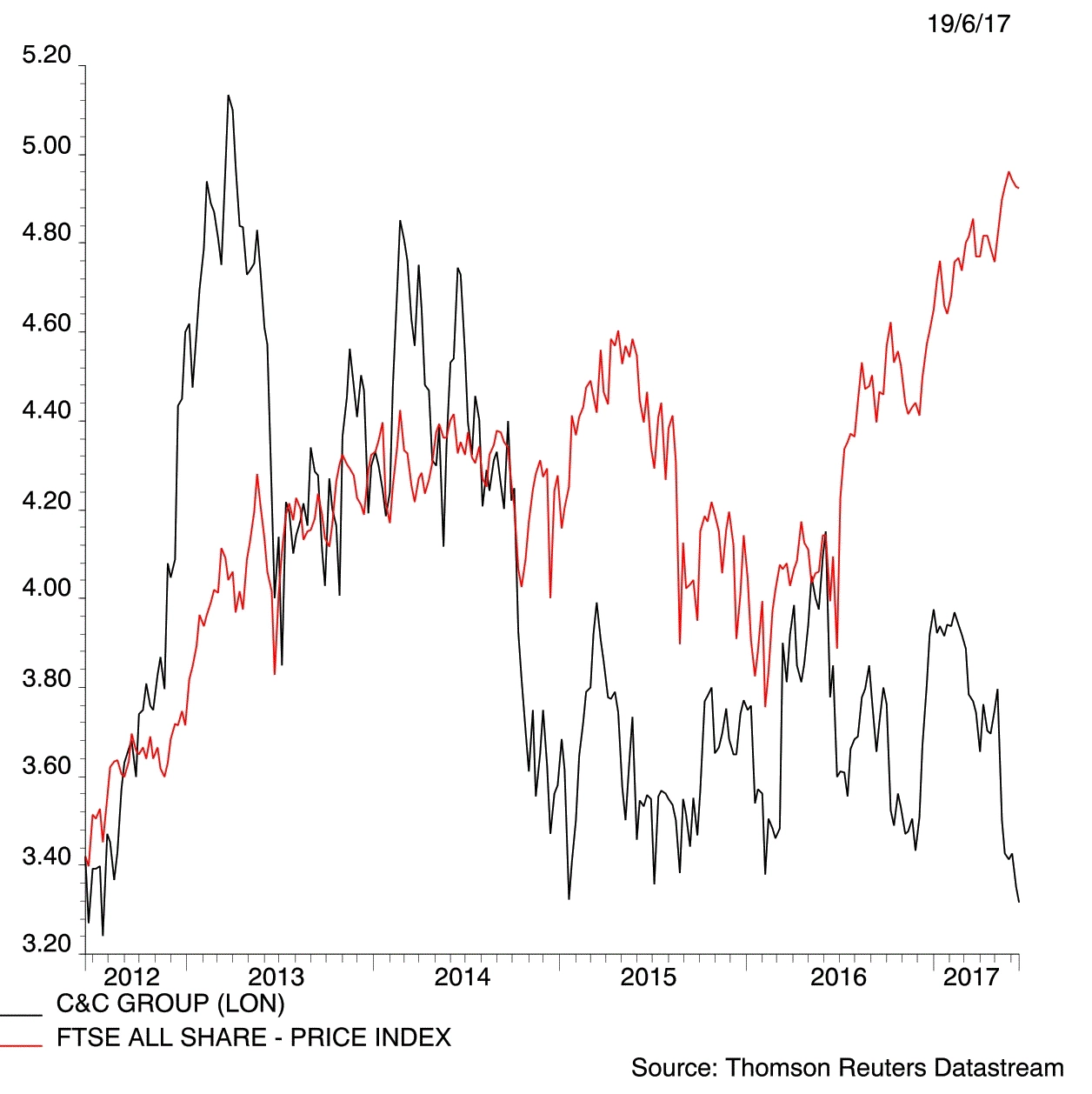

C&C (CCR) €3.33

Current market status: HATED

Best known as the maker of Magners cider, C&C seems to

be a bit confused about its future direction at present. The shares are down 16% over the past year and down 3% over the past five years.

The beer, cider, wine and soft drinks manufacturer and distributor is rubbish at making acquisitions. It tried and failed to buy pubs company Spirit three years ago; previous deals that it did make have resulted in minimal value creation for shareholders.

Irish Independent sums up the situation nicely: ‘Having spent more than half a billion euro – most of which it has since written off – on acquisitions over the past decade and failed to grow either profits or sales, drinks manufacturer C&C is going around in circles.’

Increased competition in the cider and craft categories have also weighed on the share price.

But is the market overlooking something? Let’s take a look at the bull case.

WHAT ARE THE POSITIVE POINTS FOR THE INVESTMENT CASE?

1. Cash generative stock

The premium drinks play is highly cash generative and returns capital via dividends and share buybacks. A strong balance sheet also gives C&C the firepower to invest in its production assets and brands.

2. Brand strength

Many of us will have consumed C&C’s tipples including leading Irish cider brand Bulmers, the aforementioned premium international cider brand Magners, Scottish beer brand Tennent’s and US craft cider offering Woodchuck, at some point. C&C also distributes AB InBev beers, among them Corona, in Scotland, Ireland and Northern Ireland.

3. Growth potential

C&C is a resilient business whose strong local brands

have stood the test of time. It also has a growing premium

and craft portfolio. In Magners, it has a truly international cider asset growing in territories as diverse as Russia, Spain and Thailand, while Tennent’s is another export champion.

![]()

Vodafone (VOD) 220.35p

Current market status: LOVED

Vodafone (VOD) is a staple stock for many investors thanks to its 5.9% dividend yield, the seventh biggest on the FTSE 100. The fan base has expanded recently thanks to improving organic service revenues and better cash flow metrics, the latter point easing future income affordability worries. It has also found a solution in India, a big past concern.

WHAT ARE THE NEGATIVE POINTS FOR THE INVESTMENT CASE?

1. Stiff competition

Very stiff competition acts as an anchor to profit growth. Europe represents close to two-thirds of Vodafone profit and the emergence of Iliad in Italy could lead to a cut-throat price war. The UK is also stubbornly refusing to get better with service revenue again falling last year.

2. Cash flow concerns remain

Cash flow concerns may have eased but they have not disappeared. Much of last year’s impressive €4.1bn free cash flow was thanks to big cuts in investment spending. Fewer promotions amid a weak handset market could constrain any recovery in service revenue. If so there might be implications for the payout longer-term.

3. Lack of fibre access

Lack of fibre access for broadband is still a big problem in the UK and in parts of Europe, hence the excitement of any merger with Virgin Media-owner Liberty Global such is speculated. Limited fibre caps Vodafone’s multi-play package sales proposition and makes improved service revenue gains far harder to come by.

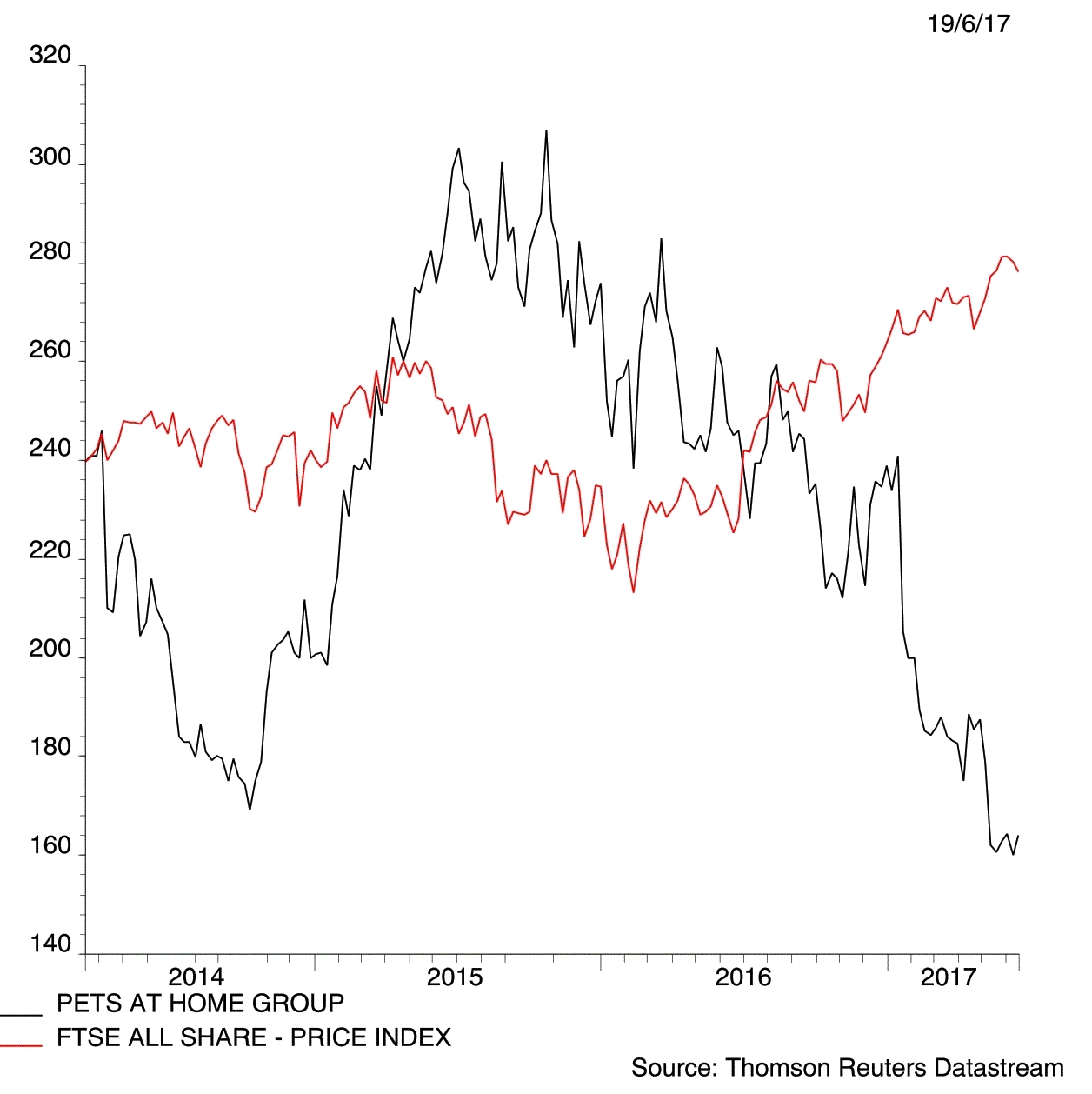

Pets at Home (PETS) 155.51p

Current market status: HATED

Specialist retailer Pets at Home (PETS) has seen

its share price fall by 37% over the past year. Analysts keep downgrading earnings forecasts amid poor trading.

Like-for-like merchandise sales have been persistently soggy, costs are rising and the consumer outlook is getting worse. Pets at Home also faces increased competition from online rivals and from the value-focused general merchandisers with physical stores.

Given the shares have been weak for some time, now might be a good point to take a contrarian view and look at the positive attributes.

WHAT ARE THE POSITIVE POINTS FOR THE INVESTMENT CASE?

1. Market leadership

Pets at Home is the largest UK omni-channel specialist pet care retailer with a network of over 400 stores and market leadership in merchandise categories. Its services division, offering vet and grooming services, is the growth engine with a strong long-term opportunity in a fragmented market.

2. Resilient industry

The £821.5m cap operates in a resilient market that grew throughout the recession. Pets at Home has a loyal, growing customer base that is also emotionally engaged. Pet owners will prioritise spending on their canine, feline and other furry friends, one factor behind the retailer’s reliably strong cash generation.

3. Retail park presence

Pets at Home has high exposure to UK retail parks, which are seeing stronger footfall than high streets and shopping centres. At the same time, online merchandise sales are growing and Pets at Home is also enjoying growth in active VIP loyalty scheme membership.

By Tom Sieber, Daniel Coatsworth, James Crux and Steven Frazer

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.