Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineHot returns

Asian powerhouse India’s macroeconomic health is the strongest it has been in a decade. The nation could be both a fantastic top down and bottom up investment story. Growth is accelerating driven by demographics and urbanisation, while corporate quality is high with many world class management teams treating minority shareholders properly. Furthermore, inflation is falling and the government remains busy and focused on its pro-growth, pro-reform agenda.

According to April’s IMF World Economic Outlook, India is not only the fastest growing economy in the Emerging Market and Developing Economies segment but the world’s fastest growing major economy. Having grown 6.8% in 2016, ahead of China’s 6.7%, India’s economy is projected to grow 7.2% in 2017 and 7.7% in 2018, outpacing its Asian rival’s projected advances of 6.6% and 6.2%. India remains on track to become the world’s third largest economy by 2030, overtaking Germany, Japan and the UK as an accelerating labour force combines with increasing labour productivity.

One key structural growth driver is the march of India’s middle class. Anticipated going back to the early 1990s and the first days of economic liberalisation, the emergence of the middle classes has been held back by a slower move towards urbanisation than in China, not to mention challenges presented by India’s culturally and geographically diverse population.

Stars are aligning

Stars are now aligning which mean the hoped-for acceleration in middle class spending is on the way. Steady urbanisation has seen a major shift in the labour market from the agricultural sector to manufacturing and services, while India also has a youthful, digitally-savvy population with internet penetration expanding rapidly.

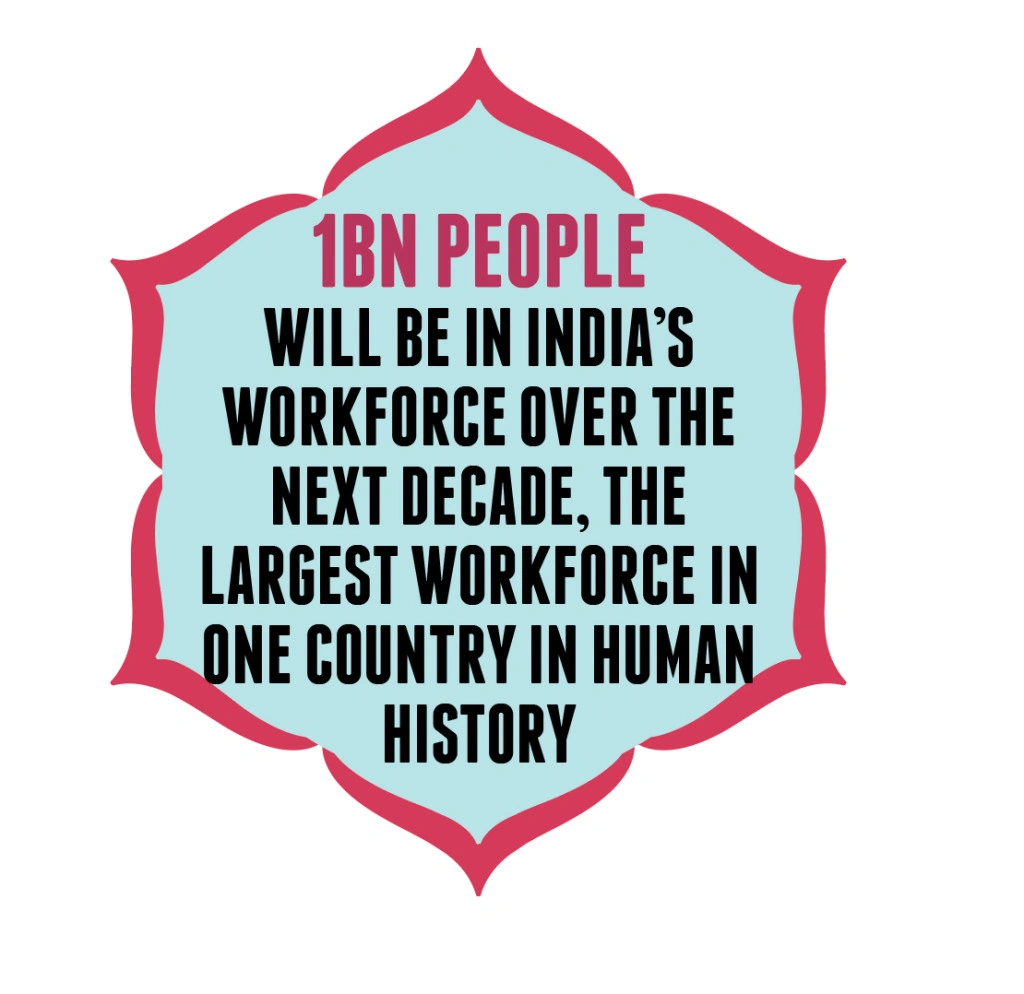

Shares notes a fascinating recent blog post by Viktor Nossek, director of research at WisdomTree Europe, who has identified five reasons why Indian equities could spice up investors’ portfolios. Chief among them is ‘a fast-growing workforce: By 2050, India’s workforce (defined as people between 15-59 years old) is expected to have grown from the current 674m to a staggering 940m. To put this into perspective, the US workforce will be a little over 200m in 2050 at its current rate and China is likely to be facing a shrinking workforce. This will potentially drive up labour costs in China—which would be a dent to its competitiveness.’

Asia’s leading market is not without risk. There are still political and economic uncertainties to navigate, there’s stubbornly embedded corruption, new infrastructure developments frequently falter and the state-controlled banking sector is encumbered by bad debts. And, following positive returns from the Indian equity market, small and mid cap valuations appear stretched.

Tasty potential

Kunal Desai, manager of the Neptune India (GB00B1L6DV51) fund, says: ‘The setup for India over the next few years is particularly positive — alongside increased political stability, we have now passed through the short-term demand reset from demonetisation (see Demonetisation decoded).

‘Corporate earnings are set to rebound as return ratios will be driven higher by the combination of excess capacity, improving demand and operating leverage and continued balance sheet restraint. India’s macro scorecard remains amongst the healthiest in the emerging world whilst investor ownership has receded.’

While some argue the country has failed to live up to the hype thus far, growth-focused investors cannot afford to overlook India. GDP growth is partly being fuelled by a more affluent, expanding population and a swelling consumer market. Combined with the ongoing process of restructuring, India could prove to be one of the most compelling investment stories for the next decade and beyond.

Modi’s major moves

Historically Indian companies had grown in spite of the government. However, since the election of a majority pro-reform party, investors and corporates alike have cheered a new dawn of stable politics.

Indian policymakers that are not shy of taking bold steps and opening the economy; a central bank that successfully fought inflation is now supportive of growth through lenient monetary policy; financial planning that is accelerating consumption, infrastructure and digitisation; and a global macro environment that is not disruptive to India’s growth.

Three years ago, Prime Minister Narendra Modi swept into power in an historic election. The first party in the country’s history to govern without the need for coalition support, Modi’s Hindu-nationalist Bharatiya Janata Party (BJP) was voted in on the promise of an impressive reform agenda.

30 people leave rural india for urban areas

every 60 seconds

With a focus on industrialisation, investment in infrastructure, clearing red tape and fiscal federalism, Modi has had both the political will and the firepower to push through necessary but politically unpopular reforms.

This March, the BJP and Modi won a stunning victory in the state election of Uttar Pradesh, India’s most populous state. The margin of victory was unexpected and has further lowered the political risk premium in India. Commentators believe Modi’s government now has a reasonably clear runway until the next general election in 2019, which will likely stimulate further reform activity in an attempt to drive India’s medium term growth potential higher.

Demonetisation Decoded

Demonetisation, Modi’s shock therapy designed to purge India of its informal economy, is well underway. The demonetisation of Rs500 and Rs1,000 currency notes announced on 8 November and resulting in 86% of the currency becoming non-legal tender overnight, created shockwaves throughout India. By starving the country of cash, Modi’s government is attempting to corner the corrupt, bring tax evaders onto the books and address the issue of counterfeit notes used for terrorism. India is therefore undergoing a dramatic structural shift away from cash and towards a digitally banked economy.

Following the abrupt cancellation of 86% of the Indian currency in circulation by the Modi government, the Indian equity market corrected sharply but recovered in January to March 2017 to touch an all-time high. Politics boosted market sentiment as the BJP party performed very strongly in the provincial elections in several states, particularly in Uttar Pradesh, confirming Modi’s enduring popularity on the ground in the aftermath of Demonetisation.

Neptune’s Desai believes that ‘one of the most significant reforms has been the parliamentary approval of the long-awaited Goods and Services Tax Bill (GST) after a decade of squabbling. Once implemented, the GST will harmonise the patchwork of national, state and local levies with a single unified VAT system, overhauling the country’s fragmented tax system.’

‘Given how this key reform has been used as a political football over the past decade, its smooth passing underlines the reformist drive from the Government whilst its implications could be a game-changer. Tax payers will now be linked to their respective PAN ID numbers which will make evasion far more difficult.

‘As India moves to a unified tax market, productivity will be lifted whilst providing a boost to Modi’s manufacturing push too – the heavy burden of cascading taxes (tax on tax) will be reduced as companies can now claim tax credits for tax already paid by their suppliers. This lower cost of manufactured products will help

boost consumption too.

Perhaps more importantly for global investors though, the GST has underlined our view that India continues to resolutely move in a pro market, pro-reform direction.’

‘Despite the market’s strong performance, India remains a bifurcated market with huge valuation divergence,’ continues Desai. ‘In particular, large-cap, quality stocks were the clear winners in an era of uncertainty and re-adjustment and as a result mid-caps trade at a 29% discount to large-caps.

‘Indeed, mid-caps and cyclicals trade significantly below long-term averages – value exists in the market but you have to find it. The Neptune India Fund therefore remains overweight both mid-caps and domestic cyclicals as they are likely to benefit from valuation support, are under-owned and are the most leveraged to the market’s cyclical upswing.’

Flourish through funds

When investing in far-flung markets, the nous of professional fund managers with contacts on the ground is invaluable. In the funds universe, one portfolio meriting attention is Jupiter India (GB00B2NHJ040), which has returned a cumulative 51.9%, 105.4% and 152.8% over one, three and five year periods respectively according to Trustnet, outperforming the IA Specialist sector. Aiming to generate long-term capital growth, the Avinash Vazirani-managed unit trust’s holdings include Hindustan Petroleum, Godfrey Phillips India and Infosys Technologies.

The aforementioned Neptune India has significantly outperformed the MSCI India Index under manager Kunal Desai’s tenure. To qualify for portfolio inclusion, stocks must be industry disruptors – ‘we are keen to invest in the disruptors, not the disrupted’ – boast high accounting quality, have sufficient liquidity and strong corporate governance.

‘A company that exhibits these characteristics is more likely to benefit from a virtuous circle of increasing investment, sales, cash generation and, therefore, shareholder value,’ says the manager. Those that pass muster with Desai include the likes of structural growth company Asian Paints, turnaround play Infosys and Apollo, India’s largest hospital network.

Options in the closed-ended investment companies space include Terry Smith’s Fundsmith Emerging Equities Trust (FEET). Trading at a 1.6% premium at the time of writing, ‘FEET’ has recently taken positions in Indian generic drugs maker Ajanta Pharma and Royal Enfield motorcycles maker Eicher Motors.

Others include the Aberdeen New India Investment Trust (ANII), on a 10.3% discount as well as the JPMorgan Indian Investment Trust (JII), where an 11.2% discount may tempt value seekers. With a bias towards quality names, the latter trust underperformed its MSCI India Index benchmark in the six months to 31 March. However, its long-term performance is strong. JPMorgan Indian has outperformed the benchmark over the three, five and ten years to 31 March 2017.

‘India is among the fastest growing economies in the world and will be for the foreseeable future,’ says portfolio manager Rajendra Nair. ‘We try and take a long-term view and capture that opportunity. We have a distinct long-term investment horizon – some of our holdings have been in the portfolio for more than a decade such as HDFC Bank, which has delivered extremely profitable growth over time, and we let compounding do the work for us.’

Prospective investors in the trust will be pocketing an exposure to other financial names such as Kotak Mahindra Bank and Indusind Bank.

Those seeking to mitigate India-specific risk could look to the broader Martin Currie Asia Unconstrained (MCP), a trust trading on an even wider 14.1% discount.

‘India’s long-term fundamentals are very interesting and under Modi there is a very interesting domestic story,’ says manager Andrew Graham, although he adds ‘animal spirits are very powerful in India, it is expensive relative to other markets and we are a little bit more cautious on it.’

Relevant portfolio positions include auto manufacturer Maruti Suzuki India, a ‘very profitable, well-run’ producer of small cars, as well as motorcycle maker Hero Moto Corp, which ‘generates a high return on capital, has a net cash balance sheet and pays a growing dividend.’

- - - - - - India Capital Growth - - - - - -

Investors seeking a concentrated fund with high active share and a mid-cap bias can purchase the India Capital Growth Fund (IGC:AIM), an AIM-quoted portfolio of 30-40 stocks with an emphasis on companies deriving the bulk of earnings from the domestic market.

Managed by Ocean Dial Asset Management, India Capital Growth’s 15.5% discount has significant scope to narrow. ‘We firmly believe going down the market cap spectrum does not necessarily mean going down the quality spectrum,’ says fund manager David Cornell, who insists ‘the closed-ended structure is ideal for mid cap India. It means we can take a longer term view.’

David Cornell

‘We see risk as the long-term destruction of capital,’ says bottom-up value investor Cornell. ‘We’re identifying companies managed by people with high levels of integrity and who understand the difference between a P&L and a balance sheet,’ he says. ‘We like to invest in companies with a long term historical track record of delivering profitable returns to shareholders and we like companies that pay dividends.’

Cornell is palpably excited by the growth potential of India, which is ‘where Mexico was 37 years ago’. Portfolio positions include the likes of Jyothy Laboratories, a maker and marketer of fabric whiteners, soaps, detergents and mosquito repellents that ‘has been a strong compounder over the last four or five years. It makes low-priced products that a billion Indians swear by and has strong brand recognition and amazing distribution across India,’ says Cornell.

‘We also like housing finance companies,’ says Cornell, invested in Dewan Housing, a play on rapidly rising penetration off a low base of basic financial products. He is also a fan of demonetisation beneficiary Kajaria Ceramics, the fastest growing and most profitable company in the Indian tile industry with a vast unorganised or informal market to chase. ‘The informal sector will either have to pay tax or it will get swallowed up,’ says Cornell, who insists Kajani’s ‘market share gains will be huge in the next four to five years.’

- - - - - - London-listed exposure - - - - - -

Investors can also access India through ETFs such as Amundi ETF MSCI India (CI2U), db x-trackers MSCI India (XCX5), Lyxor MSCI India (INRL) and WisdomTree India Quality (EPIQ). A number of London-listed companies also offer a passage to India, among them alcoholic drinks giant Diageo (DGE). The majority owner of India’s United Spirits is seeing tipples such as Johnnie Walker and McDowell’s on a growth tear and is increasingly helping wedding planners in the country set up pop-up bars at their events. Packaged consumer goods colossus Unilever (ULVR) has been in India since the 1880s, while health and hygiene products giant Reckitt Benckiser’s (RB.) Dettol and Harpic brands are growing strongly in the Asian nation.

Soon-to-be-subsumed into Tesco (TSCO), food wholesaler Booker (BOK) operates in India from four sites in Mumbai, one in Surat and one joint venture branch in Pune. Other stocks offering some exposure to India’s growth include airports and train stations food seller SSP (SSPG), which recently entered the world’s second most populated country by acquiring 15% of Travel Food Services (TFS) in India in December 2016. A further 18% was bought in March 2017, bringing SSP’s shareholding to 33%. Kate Swann-steered SSP will acquire a further 16% stake in TFS, which has operations in six of the main airports including Delhi and Mumbai as well as in railway stations, by the end of 2018.

Other India options include Holiday Inn owner InterContinental Hotels (IHG) or Mortice (MORT:AIM),forecast to grow quickly through its exposure to India’s personal security market through its Peregrine Guarding subsidiary. Lower down the market cap ranks, youth fashion portal Koovs (KOOV:AIM) offers a play on the booming demographic of young Indian urbanites, while OPG Power Ventures (OPG:AIM) has a compelling medium to longer-term investment case.

Following its merger with Cairn India, Vedanta Resources (VED) has been transformed into a diversified natural resources powerhouse anchored in India. Via its taste & nutrition arm, Ireland-based ingredients-to-packaged foods group Kerry (KYGA) is establishing a new production facility in India to support taste and clean-label technology delivery.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.