Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineChrome price shock puts cloud over Tharisa

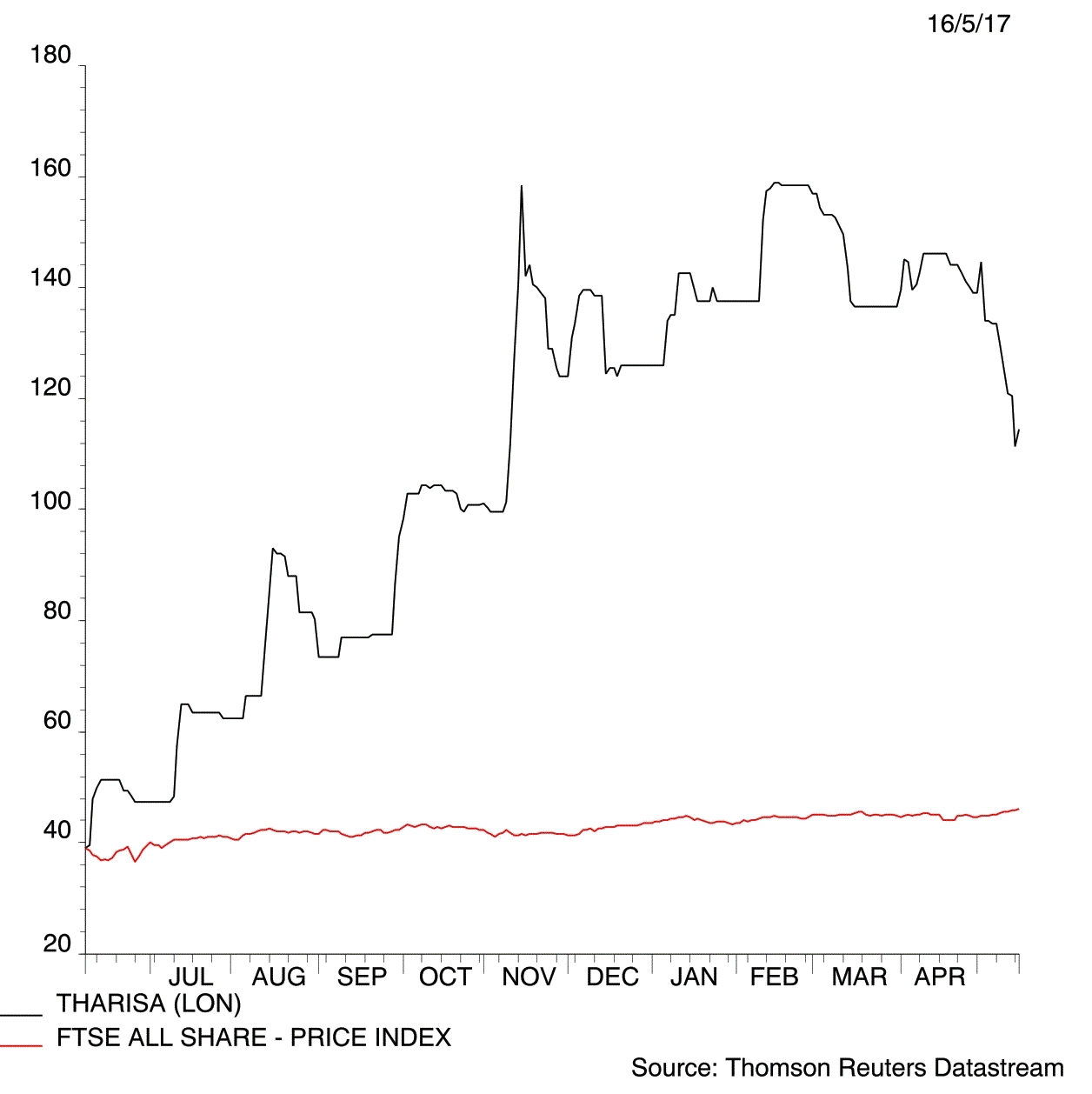

Tharisa (THS) 110p

Gain to date: 42%

Original entry point: Buy at 77.5p, 29 September 2016

Miner Tharisa (THS) tells Shares its full year earnings and cash flow expectations may have to be downgraded if the chrome price doesn’t recover from its recent sell-off. We view the commodity market correction as a short-term issue and not a reason to dump shares in Tharisa.

The chrome price has been affected by a credit squeeze in China where authorities are trying to stop banks from lending too much money. That’s hurt commodities demand – hopefully only temporarily.

Tharisa remains positive and says it will focus on improving operational efficiency, feed grades and metal recovery rates. ‘Chrome has gone from highs of $390 per tonne late last year to the mid $100s level at the moment,’ says chief executive Phoevos Pouroulis. ‘Those levels aren’t sustainable.’

He adds: ‘The chrome market is always very volatile. We can withstand the cyclicality in prices thanks to being a very low cost operator.’

Broker Peel Hunt assumed chrome prices would fall this year to $170 per tonne. Its forecasts for Tharisa’s financial year ending September 2018 only use a $188 per tonne chrome price – not the $300+ level at which the metal recently traded.

Take advantage of recent share price weakness (down 23% since early May) and buy more at 110p. Peel Hunt has a 205p price target. (DC)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.