Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy we believe UBM is the main event

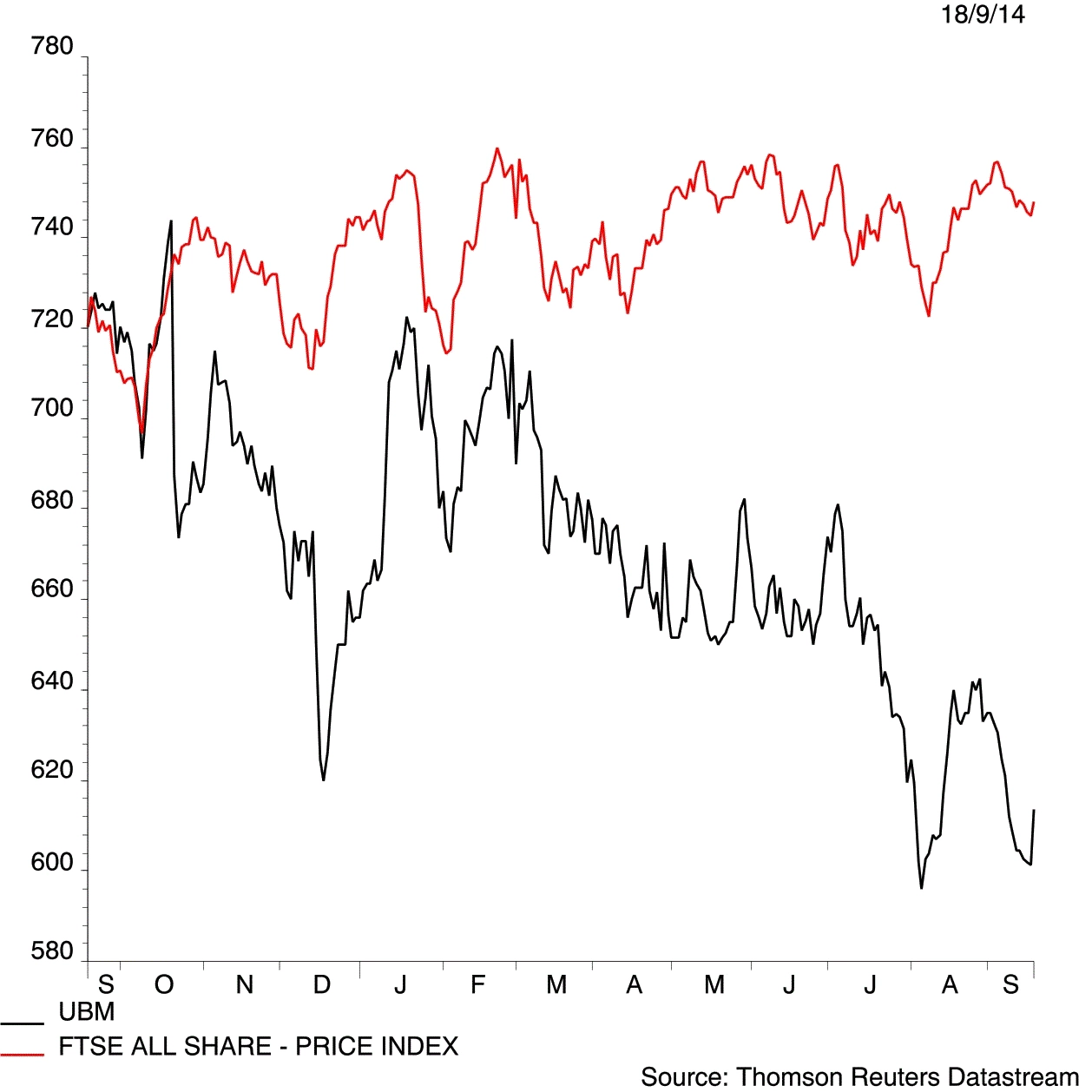

Don’t be put off by shares in UBM (UBM) slightly underperforming the broader UK stock market so far this year. We think the FTSE 250 events company could be a handsome investment over time, so buy at 716.5p.

Central to our positive view is the belief that UBM will benefit from exposure to continuing growth in Southeast Asia and a resilient US economy. It is the leading business-to-business exhibitions player in the US and Asia.

The fact it generates around 40% of its revenue from North America is really interesting when you consider US companies have just reported their best first quarter earnings season in 13 years.

That backdrop could translate into positive business sentiment and hopefully greater confidence among corporates in spending money on activities such as trade events.

Why we like events companies

Events businesses tend to deliver strong cash flow; enjoy robust revenue visibility with lots of repeat business; and, for leading events like the ones in UBM’s portfolio, have material barriers to entry.

The company has sold off non-core assets to focus almost entirely on business-to-business events as part of a strategy launched in 2014.

UBM has generated 14% annualised total return for shareholders over the past five years, according to data from SharePad.

The shares trade on an undemanding 14 times forecast earnings for the current financial year. A nice dividend yield of 3.2% offers another reason to hold the shares.

Although net debt has risen since the $485m acquisition of Asian exhibitions portfolio Allworld, which completed earlier this year, the company still has headroom for further acquisitions in a fragmented events sector.

Investment bank Liberum puts the company’s net debt to earnings ratio at 1.7 times by the end of 2017.

Integration of Allworld on track

At a Capital Markets Day on 4 May, the chief executive of UBM Asia, Jime Essink, noted the integration of Allworld was ‘completely on track’ and ‘going smoother than we could ever have expected’.

By the end of 2017 Essink expects to have merged offices in six of the eight countries where both the existing UBM business and Allworld have a footprint.

Although the company would be vulnerable to a slowdown in global growth, it benefits from diversified exposure to several different sectors which should perform well at different points in the economic cycle. (TS)

UBM (UBM) 716.5p

Stop loss: 573.2p

Market value: £2.8bn

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.