Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineTime to worry about BP and Shell’s dividends?

Another bout of volatility in the oil price is helping to overshadow strong first quarter results for UK oil majors BP (BP.) and Royal Dutch Shell (RDSB). Both of these stocks are investor favourites thanks to their generous dividends.

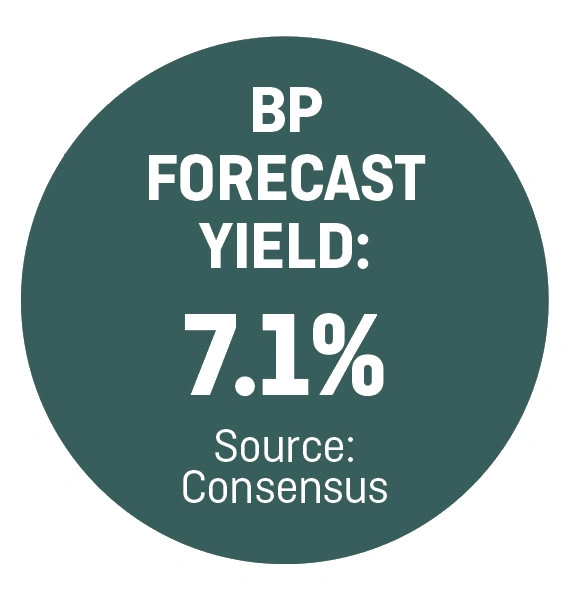

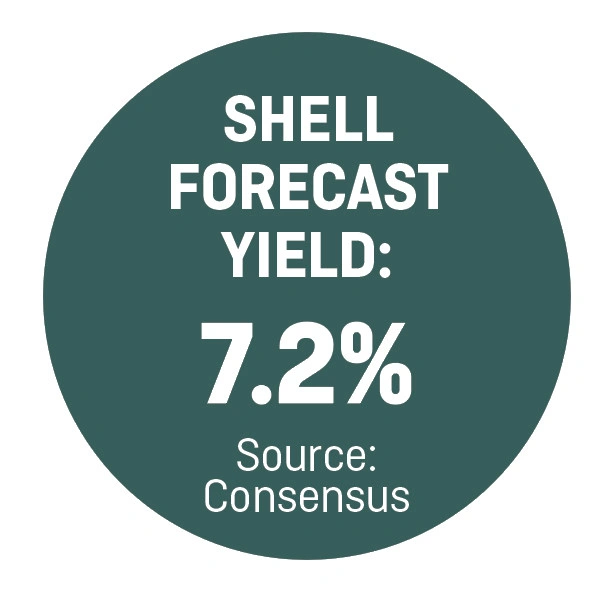

Investors taking a view on both these stocks need to decide if their dividends are sustainable. If the answer is yes then prospective yields upwards of 7% imply a significant value opportunity.

The current oil price below $50 per barrel makes it look more difficult for both BP and Shell to cover their dividend from cash flow, even if they continue to make efficiencies, so this is the key threshold for investors to watch.

Assuming no change to the dividend per share figure, a dividend yield will rise as the share price falls. The latter happens when the market is worried about something, so you mustn’t assume the generous 7% prospective yield is representative of a healthy business.

The share price should rise as the market becomes more comfortable about earnings and the sustainability of the dividend – so in that case the dividend yield would fall.

Oil price remains volatile

In early May oil prices slipped to a five-month low as investors reacted to a continuing build in US inventories. The price action has effectively put an end to the impressive oil price recovery seen since last year.

The successful exploitation of large new deposits of oil contained within shale rock in the US has created a significant new source of supply. That’s a key reason why oil prices collapsed in 2014, having previously traded above $100 per barrel.

Producers’ cartel OPEC, led by Saudi Arabia, failed to react to the over-supply problem until late 2016 when its members cut output. That action merely looked to protect market share.

Low point in 2016

It is worth taking a step back to consider the direction of the oil price over the past year or so.

Oil hit multi-year lows in the first part of 2016 amid jitters over the health of the Chinese economy.

Brent crude, the European benchmark, averaged $35.30 per barrel in the first three months of 2016. The first quarter of 2017 saw a much improved average price of $54.70 per barrel.

As a result, both BP and Shell’s latest set of quarterly numbers looked strong on a year-on-year basis.

A notable feature of both sets of results was the good cash flow performance as both companies have stripped out costs. On 2 May, BP revealed a 47% advance in operating cash flow to $4.4bn and two days later Shell reported free cash flow of $5.2bn (against an outflow of $16.3bn in the first quarter of 2016).

Why cash flow is so important

The market wants to see both companies move closer to the point where they can fund their dividends and capital expenditure from internal cash flows rather than relying on debt, disposals and scrip dividends. The latter is a way of issuing dividends in new shares rather than cash.

Analysis by broker Canaccord Genuity suggests that based

on an oil price of $52.30, BP could cover its dividend from free cash flow in 2017.

UBS says Shell could decide to move back to a full cash dividend, and abandon its scrip dividend programme, in the first quarter of 2018.

‘At this point we believe there will be enough evidence that operating cash flow can fund both the dividend and the capex. In addition, a sufficient amount of the divestment programme will have been completed to see gearing at or around the 20% mark, identified by the company.’

Running to stand still

Is there a risk both Shell and BP will simply be running to stand still if the oil price remains weak? Goldman Sachs is reporting oil may be at a capitulation point, putting its $50 per barrel forecast for 2017 at risk.

Goldman is influential on commodity prices and predicted $100 per barrel oil prices in March 2005 before that threshold was reached in February 2008.

However, its forecasting credentials were tarnished when it subsequently predicted oil would hit $200 which did not happen.

If oil prices stay below $50 for a significant period then Shell and BP’s shares could fall and their yields could rise as the market prices in the risk of a dividend cut.

BP temporarily cancelled its dividend in 2010 after the Gulf of Mexico oil spill but Shell, famously, has not cut its dividend since the Second World War. (TS)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.