Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineDouble your money

Fancy doubling your money in a year by investing in an exciting stock? Sounds great, doesn’t it? It’s harder than you think, but certainly not impossible.

Over the past 12 months, robotic process automation specialist Blue Prism (PRSM:AIM) is up by 439%; online musical equipment retailer Gear4Music (GFM:AIM) has increased by 341%; and computer games service group Keywords Studios (KWS:AIM) is trading 214% higher, for example.

Approximately 130 stocks have increased by 100% or more in value over the past year, according to Sharepad. That’s roughly 6.5% of the 2,000 companies that make up the entire UK stock market, as represented by AIM and London’s Main Market. A very impressive figure.

Over the course of this article we’ll look at stocks which analysts are confident could deliver spectacular returns over the next 12 months. We’ll explain how they came to this conclusion and look at some names in more detail.

Before we go any further, it is important to stress that this approach and the companies we will discuss are incredibly high risk.

Most of the stocks require either a major event to push up the share price, or they are currently depressed due to various issues and hard work is needed to get back on track.

Is this gambling or investing?

The line drawn between gambling and investing is typically based on someone’s perception of risk.

Many might associate investing with sober decisions involving relatively large sums of money. It’s for serious people.

Gambling, on the other hand, that’s just for laugh and perhaps a bit of excitement involving relative pocket change. It’s for people to stick a tenner on black (or red) at the casino, or backing that 100-to-one outsider at the track. It’s for fun.

What we’re really talking about is an attitude to risk.

Putting money in the stock market for your retirement or for your children’s school fees is a long game. It typically means quite a bit of hard work, often involving meticulous research before coming to a decision.

This is sensible investing of the type that could mean incremental capital gains and a steady stream of decent dividends. Lower risk, some might say, although investing in equities (which is another word for stocks and shares) is never risk-free.

Most people do not want to gamble with such ‘serious’ money that is vital for their financial future. But once in a while, and only if there is surplus cash in the kitty, many active investors want a bit more excitement. This article is firmly positioned in that camp.

SYNAIRGEN: WHEN HIGH RISK/HIGH REWARD SITUATIONS GO WRONG

Shareholders can really feel the pain when something goes wrong with a high risk/high reward stock. Just look at biotech firm Synairgen (SNG:AIM) whose shares fell 50% in a single day in April 2017 when FTSE 100 partner AstraZeneca (AZN) pulled the plug on an experimental drug designed to help patients fight common cold viruses.

Shall we roll the dice?

Sometimes rolling the dice on a high-risk stock with the potential to make a substantial profit is worth the ‘gamble’.

Most investors would love the idea of being in early on a new technological development, backing an exploration firm just before it strikes oil, or being a shareholder in a biotech that makes a vital cancer breakthrough, to give three examples.

We see this type of profit potential right now on the UK stock market, although we also see a large amount of stocks that could lose you money fairly quickly. You need to weigh up the risks and rewards for every investment – whether it is a long-term or short-term buy. Do not pick stocks blindly.

Read on to discover 11 stocks deemed by investment banking or stockbroking analysts to be ‘cracking buys’ with considerable share price upside. We’ve provided some commentary on each company.

HOW DO ANALYSTS CALCULATE PRICE TARGETS?

Investment analysts put share price targets into the market, typically as a useful guide to the potential upside or downside to a current share price.

They tend to be subjective instruments designed to help investors distinguish between stocks which an expert thinks ‘will move up a bit and those you think will treble,’ as one analyst has explained to Shares.

Most price targets are based on goals or valuations that analysts believe to be achievable within the next 12 months.

Price targets can be based on a simple extrapolation of a higher price to earnings (PE) ratio, for example. ABC plc trades on a current PE of 12 but the rating should be 15, based on various factors. Apply 15-times earnings per share (EPS) rather than 12 and bingo, there’s your price target.

More often than not you’ll find calculations are much more detailed. Enterprise value to earnings before interest, tax, depreciation and amortisation (EV/EBITDA) is sometimes used; so too sum-of-the-parts (SOTP) models.

The latter strip down the various operating segments of a business and apply appropriate valuations to each based on growth rates and operating profits and margins, then piece together the sums.

There is also the discounted cash flow (DCF) model, which uses some fairly complicated mathematics based on future cash generation, then subtracts back to the present.

Buy one or spread the risk?

Given the extreme potential for volatility and failure of such high-risk shares, investors might take a diversified approach and spread the risk of disaster over several promising shares in the hope that one or two prove themselves and rocket.

These types of stocks should only form a very small part of an investment portfolio due their high risks. Don’t invest any money that you cannot afford to lose.

Nanoco (NANO:AIM) 31.75p

Target price: 75p (Peel Hunt)

Difference between current share price and target price: 136%

Cadmium-free quantum dots technology developer Nanoco could be ‘on the cusp of commercialisation’, according to one analyst.

Its technology, which brings industry-leading sharpness, colour and clarity to digital displays, is in being evaluated by nine original equipment manufacturers (OEMs), and that’s just through its relationship with Taiwanese industrials group Wah Hong.

While smartphones, tablet computers, digital advertising boards are all potential markets for the company, for now it is all about TVs. Hisense, TCL and TPV Philips all demonstrated TVs featuring Nanoco technology at January’s Consumer Electronics Show in Las Vegas.

A possible share price catalyst could be a long awaited contract for mass production TVs using its technology, first designed at the University of Manchester before Nanoco was spun out as an independent company.

Beset with delays, Nanoco has been something of a poster child for breakthroughs shifting further out, and the share price has acted accordingly, slumping from highs of nearly 200p four years ago.

Yet it has commercial partnerships with global industrial giants, such as the Taiwan firm, the US’s Dow Chemical and Merck of Germany. That’s heavyweight assistance and CEO Michael Edelman remains confident that a breakthrough deal is close. (SF)

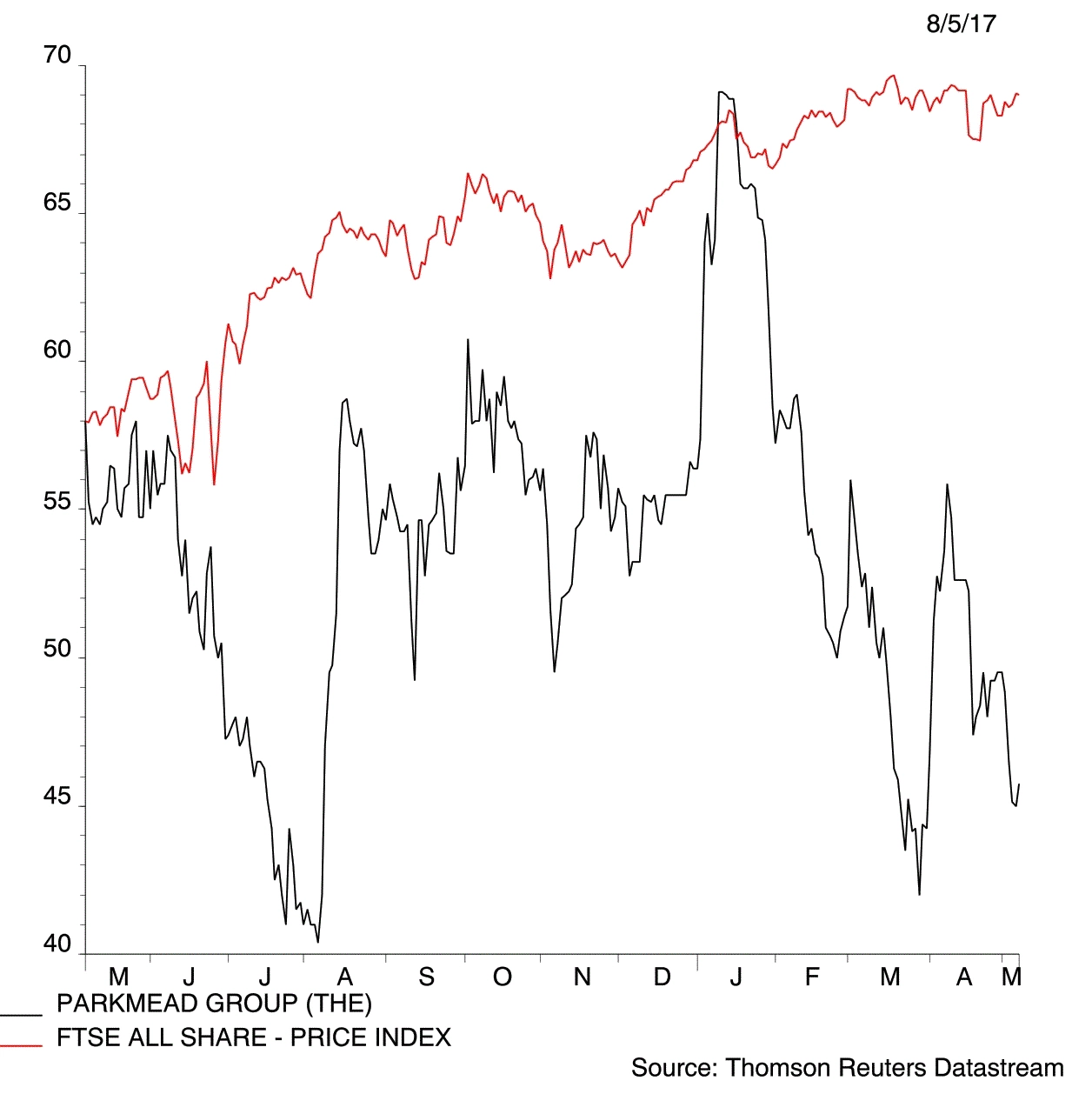

Parkmead (PMG:AIM) 46.1p

Target price : 116.3p (Consensus)

Difference between current share price and target price: 152%

Executive chairman Tom Cross established Dana Petroleum as a buy-and-build oil and gas play in the North Sea in the mid-1990s and it was acquired for £1.5bn by the Korean state vehicle KNOC in 2010. He’s trying his luck again with Parkmead.

Results for the six months to 31 December 2016 showed a gross profit of £0.7m, reversing a loss of £4.1m for the same period a year earlier. That was thanks to the end of loss making production from the Athena field and growth in Dutch natural gas production.

Hitting the ambitious price target for the stock is likely to be dependent on the company putting its £26.7m net cash to work in mergers and acquisitions.

Broker Panmure Gordon, which has a 105p price target and ‘buy’ recommendation on Parkmead, says: ‘The pace of deal activity is picking up and Parkmead’s strong balance sheet puts Tom Cross in a good position to reprise his old magic.’ (TS)

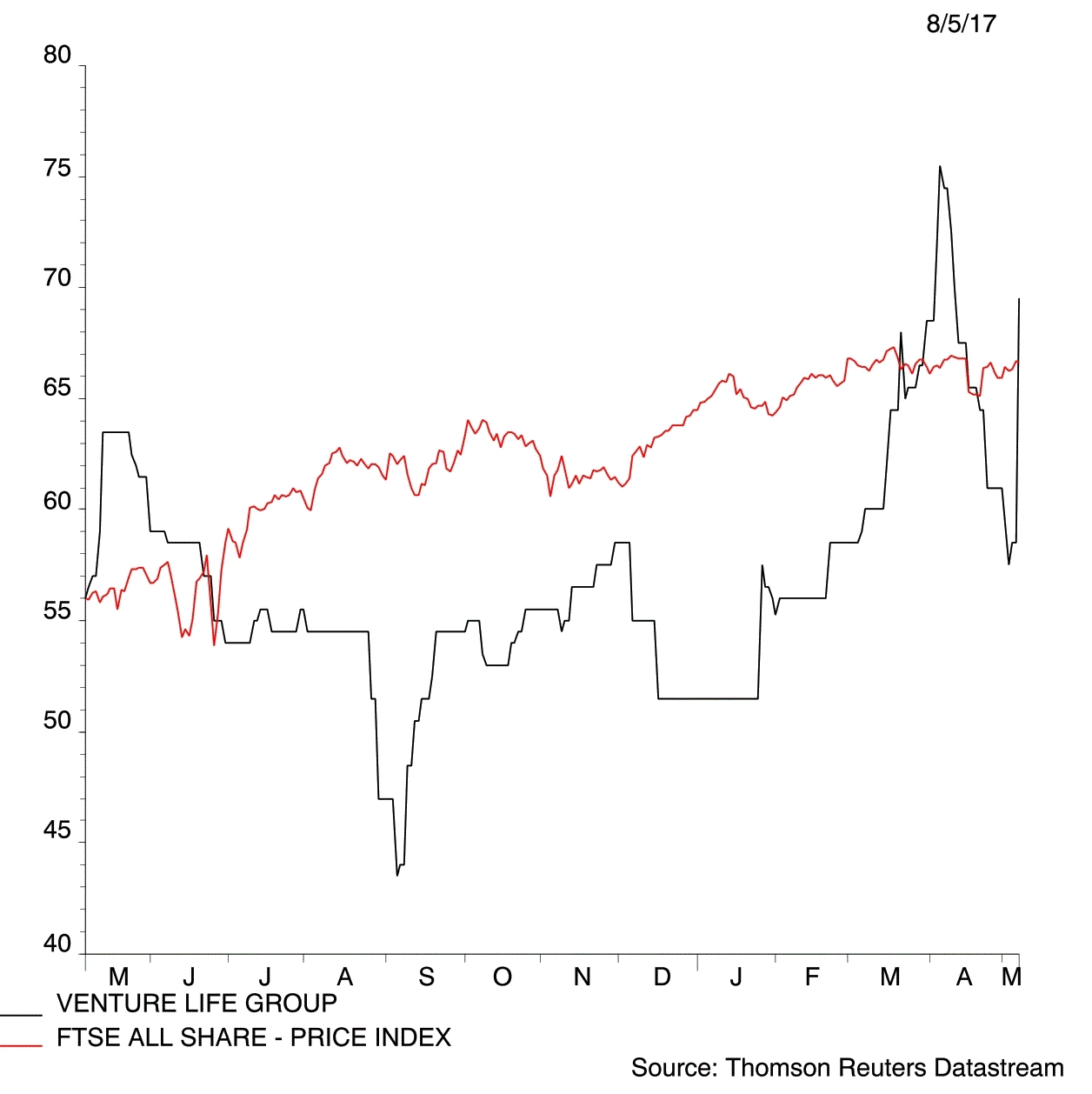

Venture Life (VLG:AIM) 58.5p

Target price: 128p (Panmure Gordon)

Difference between current share price and target price: 119%

Venture Life is a consumer healthcare company focused on self-care products targeted at the global ageing population. It develops, makes and commercialises a range spanning oral care products, food supplements for lowering cholesterol and maintaining brain function, not to mention medical devices, cosmetics as well as eye and skin care products.

‘We consider Venture Life to be a well-positioned growth business taking advantage of a well-developed product platform, with high-quality execution,’ says Panmure Gordon analyst Mike Mitchell. ‘Lower risk compared with biopharma sector stocks; this is a clinically-backed vertically integrated business with good potential to combine both acquisitive and organic growth.

‘The strategy developed and executed over the last three years across products, team, structure and resource is now delivering significant operational leverage with a platform towards sustainable profitability.’

The company achieved in 2016 maiden EBITDA (earnings before interest, tax, depreciation and amortisation) profitability of £800,000 (2015: £600,000 loss) on sales up 57% to £14.3m.

Highlights included the integration of the UltraDEX oral care brand, as well as a flurry of new product launches from partners and the inking of numerous international distribution deals.

The New Year appears to have started strongly, although investors should be mindful of increased net debt and the fact liquidity in the shares could be better. (JC)

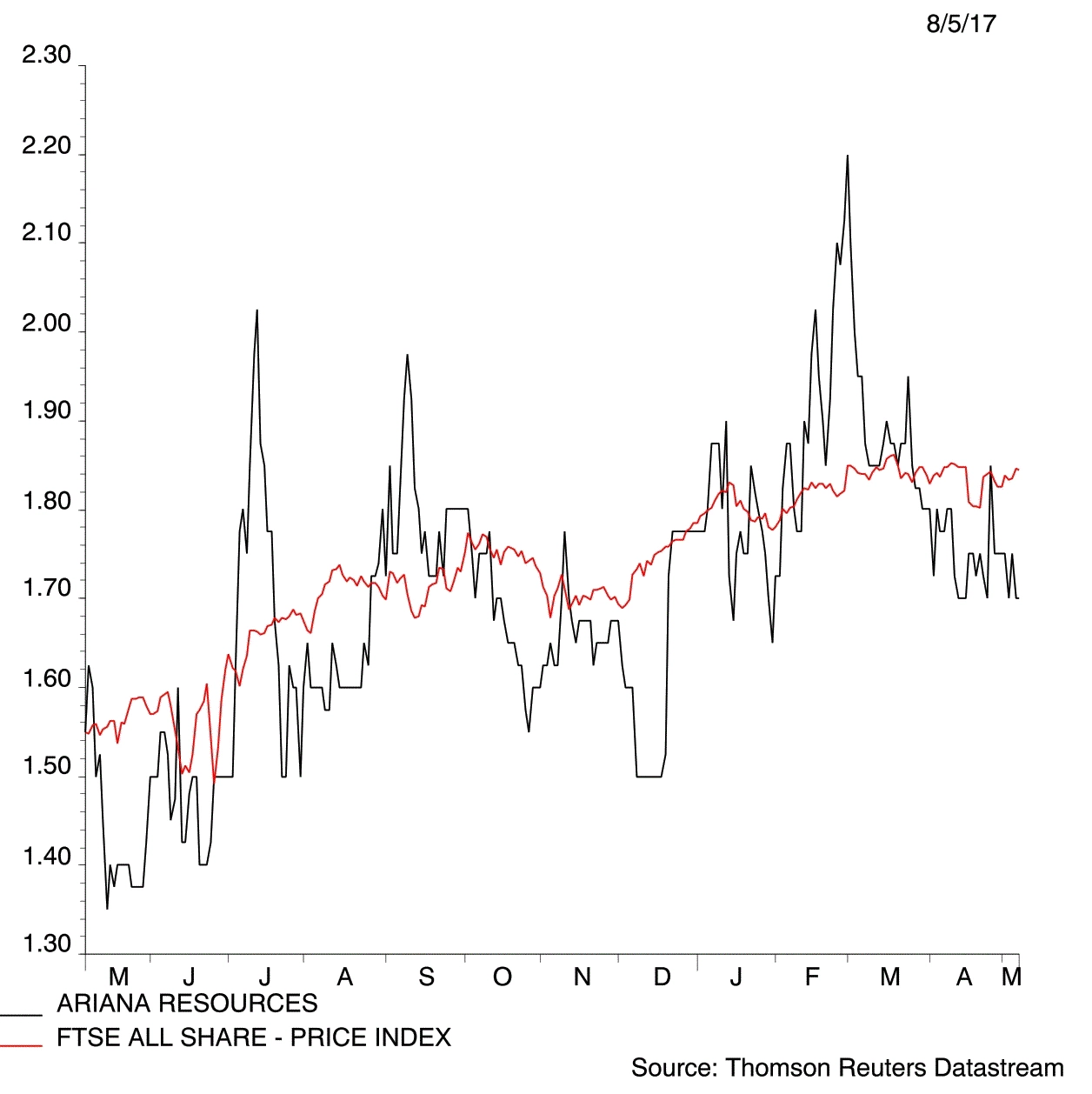

Ariana Resources (AAU:AIM) 1.66p

Target price: 3.31p (Panmure Gordon)

Difference between current share price and target price: 99%

You could double your money over the next year by investing in Ariana Resources, claims broker Panmure Gordon. Its 3.31p price target is approximately twice the miner’s current 1.66p share price.

Ariana has just started production on the Kiziltepe gold and silver mine in Turkey. Theoretically miners should see an upwards re-rating when they move from developer to producer, reflecting their shift from consuming cash to generating cash. That hasn’t happened (yet) at Ariana.

The market seems worried that Ariana won’t generate enough cash in the short term and will need to raise more money for working capital, potentially at a discount to the share price.

The company is also too small at the moment to attract interest from institutional investors so the share price is at the mercy of retail investors, many of whom only want to trade mining stocks for quick wins and not hold the shares for very long.

We believe Ariana’s share price might stand a better chance of moving up once it can show its mine is operating smoothly.

Another catalyst could be new exploration work this summer on a gold project in Turkey called Salinbas. This is located close to Hot Maden, a very high quality gold prospect which has caused a lot of excitement in the market and saw its 30% owner Mariana Resources (MARL:AIM) receive a takeover offer in April.

It is common to experience teething problems with new mines, so don’t assume Kiziltepe will run without any hitches. It remains to be seen how exploration at Salinbas will be funded. (DC)

Horizonte Minerals (HZM:AIM) 2.4p

Target price: 8p (FinnCap)

Difference between current share price and target price: 233%

The miner has a substantial nickel exploration project in Brazil and plenty of cash to complete a feasibility study. FinnCap says Horizonte is trying to position itself as one of the lowest cost nickel producers globally.

The market isn’t overly interested at the moment due to weak nickel prices and question marks over how a £29m business will raise an estimated £354m to build the mine. Raising that amount of money won’t be impossible as long as the nickel price is in a rising trend and there is positive sentiment towards the mining sector at the time. (DC)

ImmuPharma (IMM:AIM) 54p

Target price: 171p (Northland Capital)

Difference between current share price and target price: 217%

The biotech is undergoing its Phase III trial for its core treatment Lupuzor to help treat lupus,

an autoimmune chronic inflammatory disease with no cure.

Lupuzor modifies the behaviour of certain key cells involved in the development of the disease. Northland Capital analyst Vadim Alexandre believes Lupuzor has blockbuster potential.

Investors should recognise the potential risks such as a negative outcome of its Phase III trial or more expensive drug development costs than originally anticipated. (LMJ)

Seeing Machines (SEE:AIM) 3.88p

Target price 12p (FinnCap)

Difference between current share price and target price: 209%

The company’s driver monitoring systems are already being resold into the mining industry by Caterpillar; the next leg up will likely be in cars.

A deal with one massive car maker could see some luxury models roll off production lines

later this year, but getting a second or third

original equipment manufacturing (OEM) motor deal is perhaps what is needed to really ignite the share price.

Fleet trucks, trains and planes are target market opportunities at an earlier stage, and don’t rule out EU regulations enforcing implementation of monitoring equipment to avoid major crash catastrophes. (SF)

Trinity Exploration & Production (TRIN:AIM) 13.25p

Target price: 37p (Cantor Fitzgerald)

Difference between current share price and target price: 179%

The oil producer completed a restructuring process around the turn of the year. It now has sufficient capital to fund a work programme onshore Trinidad which could lift production to 3,000 barrels of oil per day in the coming 12 months.

Trinity needs to achieve this output level if it has any chance of hitting Cantor’s price target. (TS)

St Ives (SIV) 51.25p

Target price: 125p (Numis)

Difference between current share price and target price: 144%

The marketing services group has suffered a squeeze on profit margins due to intense competition in several parts of its business. Investors have had to stomach several profit warnings over the last few years and a big dividend cut.

Broker Numis reckons St Ives ‘is showing signs of being through the worst’. Contrarian investors might find some interest in the stock at present, although ongoing weak share price implies the market remains sceptical until the small cap shows an improvement in trading. (DC)

DekelOil (DKL:AIM) 13.75p

Target price: 29p (Cantor Fitzgerald)

Difference between current share price and target price: 111%

Shares in West African palm oil producer DekelOil could more than double to 29p according to Cantor Fitzgerald. The company owns and operates the low cost Ayenouan palm oil project in Cote d’Ivoire. It is enjoying stronger production and improving selling prices for crude palm oil and palm kernel oil.

Given the strategic attractions of its assets, some experts believe DekelOil could emerge as a takeover target in time, although commodity price volatility and macro and political events are ongoing risks to consider. (JC)

Velocys (VLS:AIM) 52p

Target price: 103.5p (Consensus)

Difference between current share price and target price: 99%

A good first step to small-scale gas-to-liquids play Velocys delivering the upside identified by analysts is demonstrating that its technology is commercial.

Its most advanced project is the ENVIA Energy GTL plant in Oklahoma City. Broker Canaccord Genuity reckons a run period of as little as six months ‘will be enough to demonstrate the viability of the process’ and the ENVIA plant came on stream in February.

If the development fails to deliver, we see a high potential for the share price to collapse. (TS)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.