Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

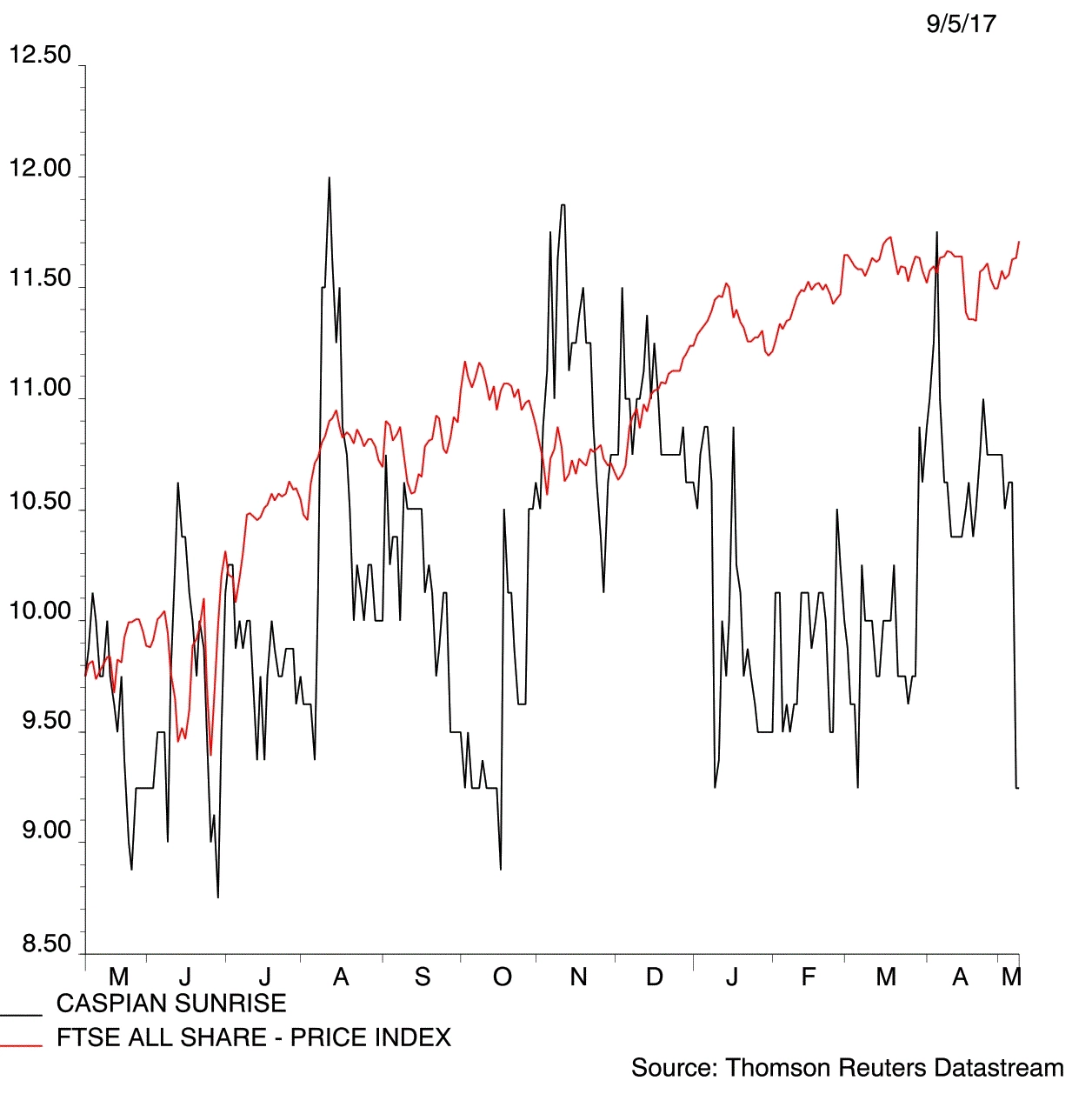

magazineClouds form for Caspian Sunrise

Caspian Sunrise (CASP:AIM) 9.2p

Loss to date: -4.7%

Original entry point: Buy at 9.5p, 30 March 2017

Mixed drilling results and a continuing wait for the Kazakh authorities to sign off on a key transaction with private company Baverstock are putting Caspian Sunrise (CASP:AIM) on the back foot.

The latest work on its BNG asset showed two of the six horizons targeted by the well are not considered worth pursuing with the remainder planned for testing.

If this testing shows up a significant quantity of oil a further two wells will be drilled later in 2017.

On its deep A6 well the company noted limited recoveries of oil had been possible and a chemical wash will be used to stimulate the flow of crude from the well.

The company expects approval on the Baverstock deal, which would see Caspian lift its interest in its flagship BNG licence from 58% to 99%, by the end of the second quarter of this year.

House broker WH Ireland keeps the faith with analyst Brendan Long reiterating a 23.3p price target and ‘buy’ recommendation and commenting the company is ‘poised for extraordinary value creation’.

Keep the faith for now. (TS)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.