Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineTake profit on Proactis

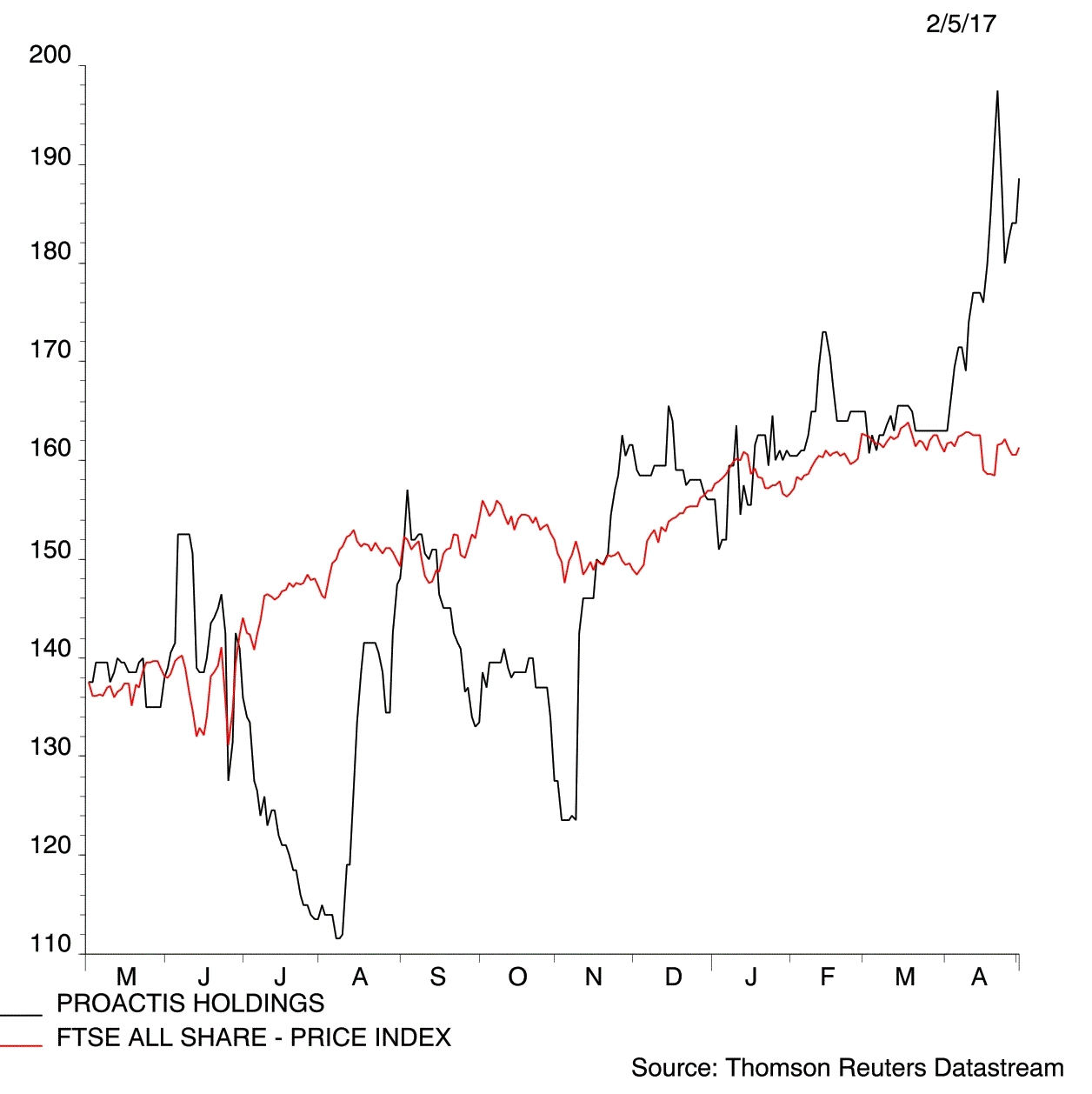

Proactis (PHD:AIM) 187.5p

Gain to date: 43.7%

Original entry point: Buy at 130.5p, 18 August 2016

We said there could be 50%-plus upside in the Proactis (PHD:AIM) share price and we were right. The share price hit 198.9p on 24 April, representing a 52% gain.

The slightly lower current price of 187.5p still represents an excellent time to take well-earned profits on the e-procurement and spend analytics platform provider.

Half year results on 26 April showed impressive 13% organic revenue growth, 27 new clients, 59 deals with existing customers and encouraging renewal trends.

Management have also done a fine job spotting and integrating value-adding acquisitions, including Millstream and Due North.

Further upside may come from its ledger sharing accelerated payment platform, although it remains at the trial stage.

That may encourage some investors to only sell some of their shares, perhaps covering initial outlay, and running the rest for cost-free profit potential.

The shares look fully priced on 17.5 times forecast earnings for the year to 31 July 2018. We’ll keep a close watch on developments and we suggest investors do the same.

Now is the right time to book a well-earned profit. (SF)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.