Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThree funds looking for bargain-priced stocks

Deep value investing involves buying bargain basement shares in the hope they will eventually move back to their intrinsic value. It is a strategy that has forged the reputations of some of the world’s greatest investors.

Value investing can be highly volatile and takes a lot of patience; hence many fund managers shy away from it.

Among the notable exceptions are Nick Kirrage and Kevin Murphy, managers of the Schroder Recovery (GB0007893760) fund. They’ve delivered 8.3% annualised returns for investors over the past 10 years, according to Morningstar.

We’d also highlight Joe Bauernfreund who has a specific deep value style for the British Empire Trust (BTEM), seeking out quality companies trading at a wide discount to net asset value. The investment trust had an exception year in 2016 with close to 42% share price gain.

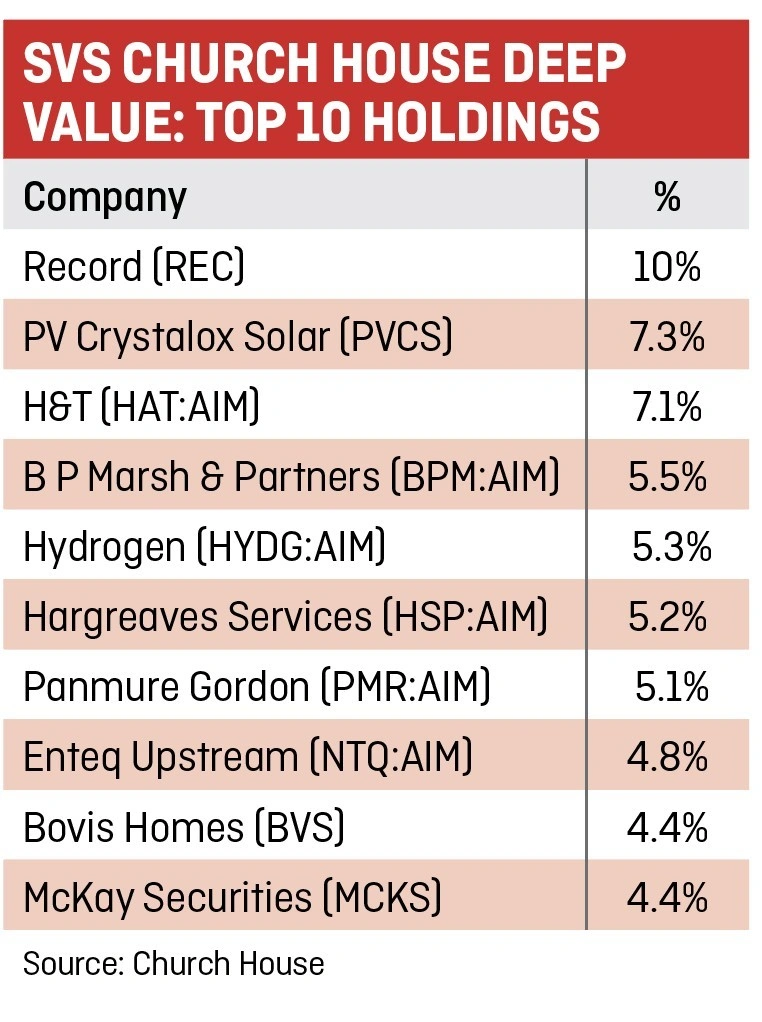

Less well known to investors is the SVS Church House Deep Value Investment Fund (GB00B79XM025), a concentrated portfolio of holdings exhibiting deep value characteristics seeking to generate long-term capital growth for investors.

The fund, which launched in 2012, has achieved 7% annualised total return over the past five years. Its price went up nearly 24% in 2016 which put the fund in the top 3% of best performers in the UK Small-Cap Equity category, according to Morningstar.

How does it spot a value opportunity?

SVS Church House Deep Value is run by Jeroen Bos who justifies a company’s value based on balance sheet information rather than future earnings forecasts.

His goal is to find companies where the assets on the balance sheet outnumber the liabilities. He trawls the market for so-called ‘net-net investments’, first described by famous investor Benjamin Graham. This is when the current assets of the company outnumber all of its liabilities, enabling investors, theoretically, to buy a pound for 50p.

What questions does it ask?

‘When I go and see these companies, my first question is always: are you planning to take the company private?’ explains Bos.

‘When things are going bad,

it is very easy to rob shareholders because nobody is interested in the company anymore and nobody is going to put up a fight. That is obviously a big risk for me.’

Bos also probes prospective investee management teams to find out if they are planning a dilutive rights issue, seeks comfort in sizeable management stakes and is reassured by the presence of other institutional shareholders on the register.

Examples of successful investments

The portfolio really took off following the vote for Brexit, as it provided an opportunity to go fishing for bargains amid a broad market decline.

‘We bought Telford Homes (TEF:AIM) in the aftermath of the Brexit vote, when many commentators expressed their doubts for the immediate and medium term outlook for the industry,’ recounts Bos.

‘As a result the whole sector endured an immediate sell-off, which was of such an extent that Bovis Homes (BVS) and Telford could then be bought at their near liquidation valuations; levels last seen in the recession years of 2008/9.

‘The net-net for Telford worked out at 282p, based on the “Group Balance sheet including proportional share of joint ventures”, as at 31 March 2016 and released in June that year. We paid 268p and Telford is trading today at 420p.’

Bos also pounced on property companies including McKay Securities (MCKS), bought at 175p and now trading at 230p. Other investment included Great Portland Estates (GPOR) and Land Securities (LAND).

Look for assets on the balance sheet

that exceed liabilities

Takeover joy

Having ‘waited a good while for takeover approaches to reappear’, two of the fund’s investments have been on the receiving end of bids in recent months.

Bovis had two approaches by Galliford Try (GFRD) and Redrow (RDW), both since withdrawn; while stockbroker Panmure Gordon (PMR:AIM) is being acquired for £15.5m.

‘We are happy with the Panmure bid, as it has proven a very profitable investment for us. The investment was made on the basis that we expected consolidation would be inevitable in this sector, where Panmure Gordon seemed to be us the most attractive target.’

What else is in its portfolio?

Other portfolio performers include pawnbroker H&T (HAT:AIM), a beneficiary, among other factors, of capacity withdrawal after rival Albemarle & Bond went belly up.

‘I paid 172p for H&T,’ says Bos, ‘and the stock is now trading at 299.75p’, a princely gain approaching 75% at the time of writing.

Bos still holds interior fit-out and refurbishment specialist Havelock Europa (HVE:AIM), a recovery stock he still thinks will come right.

‘Management told me what they were going to do and they’ve done exactly that,’ insists Bos, encouraged by new chairman Ian Godden’s purchase of stock at a premium to the then-share price. ‘That to me is a very positive sign.’

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.