Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineCan BooHoo.com shares keep rising?

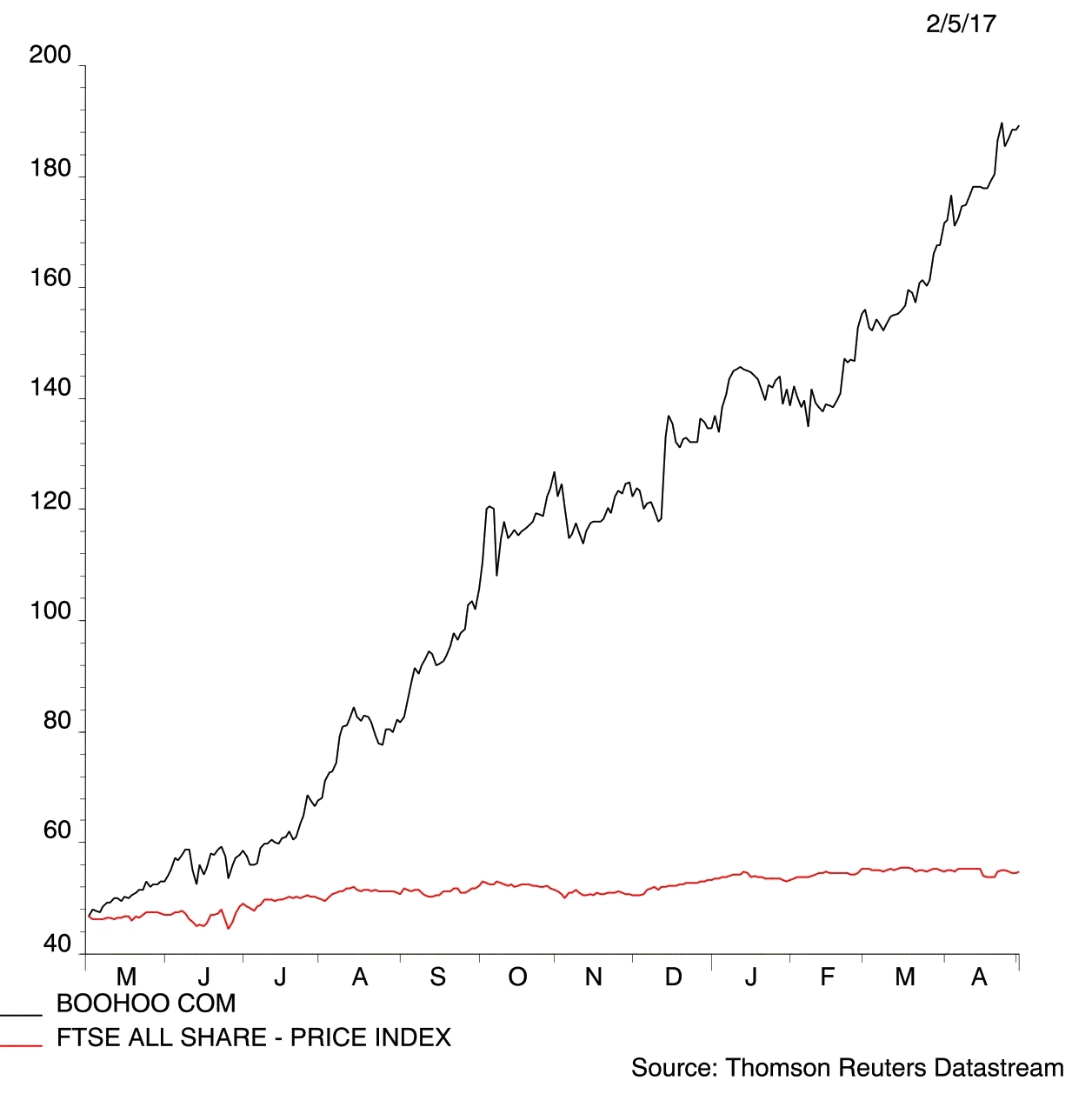

Online fashion star Boohoo.com (BOO:AIM) continues to put smiles on investors’ faces.

The shares at 188.5p aren’t cheap on 70 times forwards earnings. Yet six analysts out of 11 analysts covering the stock rate the shares either as a ‘buy’ or ‘outperform’, according to Reuters data. Key to their positive view is impressive earnings momentum.

Boohoo’s latest financial results show more customers are shopping with its website, ordering more frequently and spending more per order. Boohoo has also morphed into a multi-branded business following the acquisitions of PrettyLittleThing and Nasty Gal.

It is conservatively guiding towards 50% sales growth this year with an EBITDA (earnings before interest, tax, depreciation and amortisation) margin target of around 10%.

We admire Boohoo’s ‘test-and-repeat’ model that limits fashion risk and avoids having unwanted stock.

Well-invested for current growth projections, Boohoo’s addition of complementary brands should help drive further rapid international growth and we’re comforted by the £58.4m net cash position.

Shore Capital analyst George Mensah believes Boohoo has strong earnings momentum. He sees scope for further earnings upgrades as the year progresses – despite having already lifted his estimates in late April.

For the year to February 2018, Mensah forecasts pre-tax profit of £37.5m (2017: £30.9m) for earnings per share of 2.7p (2016: 2.2p). (JC)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.