Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineMore inspiration for your ISA

With a new tax year just around the corner you might be wondering which investments to place in your ISA. The annual allowance is increasing to £20,000 on 6 April, giving you greater scope to put your hard-earned cash to work in a tax-efficient manner.

In last week’s issue of Shares we gave some stock and fund ideas for people falling into three broad categories: the forward thinker, the beginner and the undecided.

This week we’ve gathered suggestions for another three types of investor: the cautious, the switcher and the aggressive.

The ideas are aimed at both beginner and experienced investors.

When building a portfolio, it is vital to ensure your investment selections are capable of achieving your objectives and are in line with your attitude to risk.

Even if you’re a cautious investor, you don’t necessarily have to limit yourself to cautious investments. Ryan Hughes, head of fund selection at AJ Bell Youinvest, says by combining lower-risk investments with slightly higher-risk ones you can benefit from diversification, which in turn lowers the overall risk of your portfolio.

Hughes says investors have to take an element of risk to achieve a 4% total return in today’s market. Cash offers nowhere near 4% and the yield on 10-year government bonds is around 1.25%. The FTSE 100 is forecast to yield around 4% this year.

‘As a cautious investor you’re going to have to look at an element of corporate bond and equity exposure. Within that equity exposure it might be worth looking at an absolute return fund which can benefit from falling as well as rising share prices and aims to produce a positive return in all market circumstances,’ says Hughes.

Asset weightings

One idea to consider is equally weighting three different strategies: corporate bond, absolute return and equity income. An example of a corporate bond fund is Royal London Short Duration Credit (GB00BD050B66), which focuses on bonds with less than five years to maturity. It has delivered returns of 13.2% in total since its launch in late 2013.

‘For those investors who are more cautious, looking to short duration could prove to be the best way to mitigate the problems caused by rising rates,’ explains Hughes.

Absolute return funds include Henderson UK Absolute Return (GB00B5KKCX12). Hughes says the fund has been good at navigating volatile markets, which could prove useful as the UK starts its formal withdrawal from the EU. The fund has grown by more than 60% over the past seven years.

‘With a low-risk approach to investing, this is a good option for those making their first investments in the stock market,’ Hughes says.

International exposure

Someone like Melanie could try to aim for a total return in the high single digits, although this is difficult in the current environment of low interest rates and poor bond yields.

Andrew Craig, founder and author at Plain English Finance, says the ‘permanent portfolio’ theory, where you invest 25% each in gold, the 10-year bond of a large western government, cash and a big equity market index, is likely to result in underperformance in the world today.

Instead, he says investors might need to seek out an international and multi-faceted product or one that applies some kind of trend following to mitigate the risk of underperformance.

An example of a more international fund is 7IM AAP Moderately Adventurous (GB00B2PB2M73). It has a five-year annualised return of 8.3% and offers asset and geographical diversification.

Funds and exchange-traded funds (ETFs) pretty much do the same job in a portfolio. One fund or ETF can invest in hundreds, sometimes thousands, of stocks and/or bonds, bringing instant diversification. You don’t have to keep track of every security because the fund or ETF is managed by experts who do that for you.

But there are important differences. ETFs are index-tracking investments which usually makes them cheaper than funds. Unlike funds, they don’t need to employ vast teams of analysts to evaluate every company in the market.

‘ETFs are also easier to monitor – when you buy an ETF, you know your return will be close to the index,’ says Adam Laird, head of ETF strategy, Northern Europe at Lyxor.

Active funds can often charge 1% or more in fees. ETFs are generally much cheaper.

Research by Lyxor shows less than half (47%) of active fund managers outperformed their benchmark in 2015. Over the five years between 2010 and 2015, just 23% of managers outperformed.

‘There are multiple reasons for this, but fees are clearly one important factor,’ says Laird.

It’s important to look at more than the headline fee quoted by ETFs. They can have large bid-offer spreads – the difference between the price at which they can be sold and bought. You should also compare the dealing and holding charges levied by your investment platform for ETFs and funds.

Swapping funds

Peter Griffin, investment director at financial planning firm Gale and Phillipson, says that aside from costs, there is much more to consider than simply picking an ETF with a name that sounds right.

‘Does your “global” ETF exclude emerging market equities? Does your emerging market ETF overlap with any more general Far Eastern holdings? For example, HSBC MSCI Emerging Market UCITS ETF (HMEF) is on our panel and would pair well with Far Eastern holdings in our portfolios. Research is crucial to avoid missing out on exposure you want to hold or doubling up where you don’t,’ says Griffin.

It’s relatively easy to swap a large-cap UK or US fund for the corresponding ETF. The fees are very low because the ETFs track developed and well-known indices.

iShares FTSE 100 UCITS ETF (CUKX) and Vanguard S&P 500 UCITS ETF (VUSD) both have ongoing charges of just 0.07%. This is far cheaper than something like GAM Star Capital Appreciation US Equity (IE00B5SLLT59), which has one of the highest charges in the North America fund sector at 1.07%.

GAM’s active fund employs a huge team of people to make investment decisions. Its three-year annualised return is 12% compared with 23% for the Vanguard ETF.

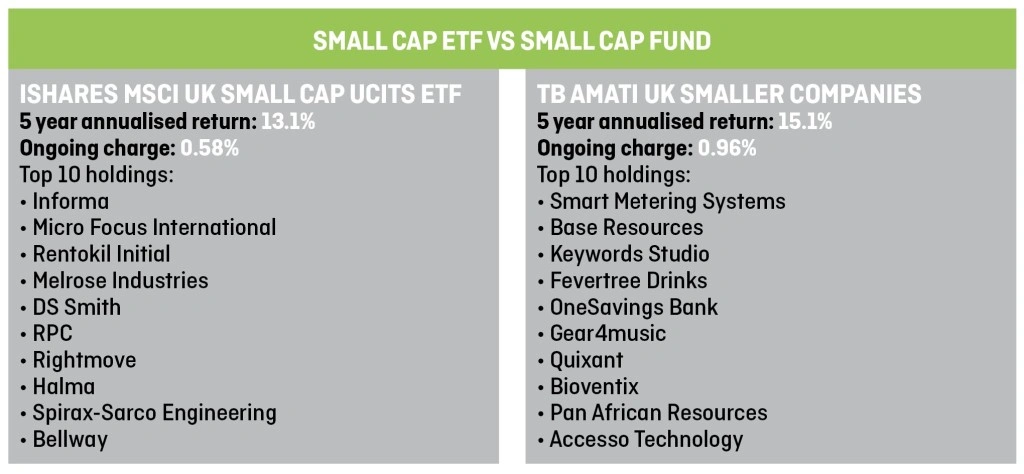

You can also get ETFs offering small-cap exposure, such as iShares MSCI UK Small Cap UCITS ETF (CUKS), which has an ongoing charge of 0.58%. A comparable fund is TB Amati UK Smaller Companies (GB00B2NG4R39), with an ongoing charge of 0.96%.

Instead of simply tracking an index, the Amati fund invests in companies which the managers believe have the potential to generate attractive levels of revenue and earnings growth over the long-term. It is also investing in much smaller companies than the iShares ETF.

You are paying slightly more to get active fund management. It can be worth paying a bit more if the fund manager can consistently deliver positive results better than the corresponding benchmark index.

That’s an important point. Don’t automatically go for ETFs just to have a lower fee. An active fund is well worth owning if the fund manager is good at their job.

Equity income

It’s even possible to get access to an equity income strategy via an ETF. Some target high-yielding stocks, such as iShares UK Dividend UCITS ETF (IUKD). Griffin says a passive approach will reduce the cost, but may remove some elements of risk control present in active funds.

There aren’t many funds which focus on individual sectors, which is an area where ETFs come to the fore. You can get ETFs tracking most sectors, some of which are very niche. For example, Laird says Lyxor MSCI World Information Technology UCITS ETF (TNOW) has been popular this year because investors like the innovative nature of IT and high tech companies.

Someone with a high risk appetite and an investment timeframe of 10 years can usually afford to weight the majority of their portfolio towards equities.

Alan Cram, head of investments at financial advice firm Ellis Bates, suggests having an equity exposure of 90% but still ensuring your portfolio is diversified.

‘Regardless of a high appetite to risk, it is still essential to diversify across a range of holdings and think carefully about how exposure to risk/reward can be managed through sectors and regions that provide the potential for greater returns over the long-term,’ he says.

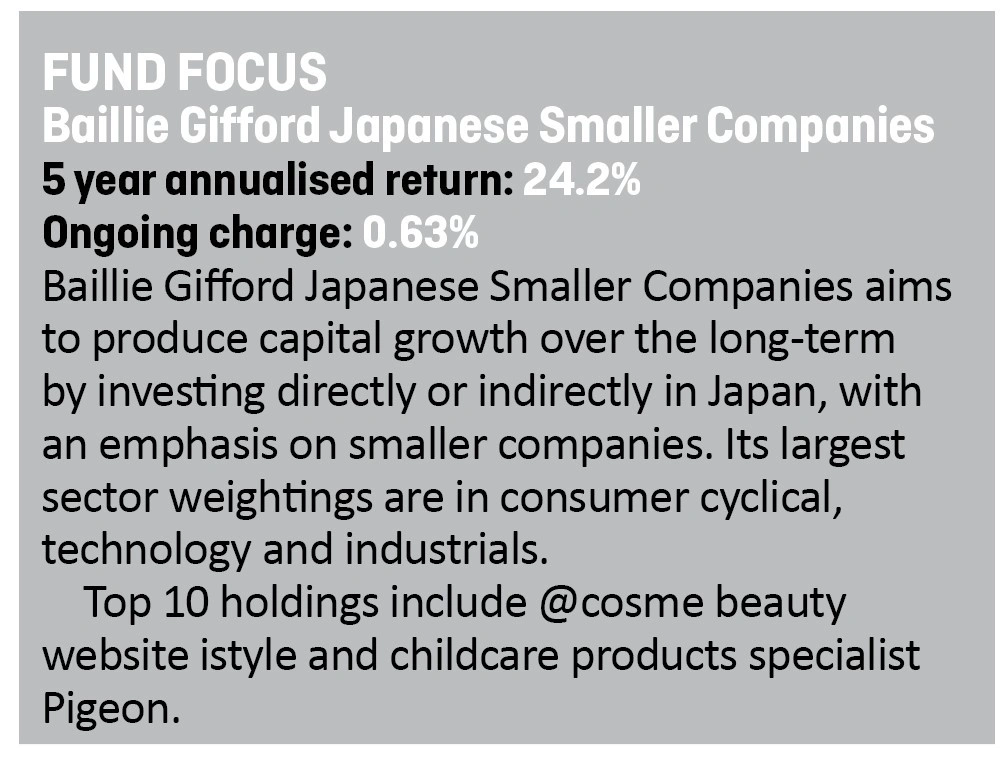

Cram says you can add risk and potentially higher returns to your portfolio by investing in single country equity funds, such as Jupiter India (GB00BD08NQ14) and Baillie Gifford Japanese Smaller Companies (GB0006014921). He says someone like Martha could also consider emerging markets funds like MI Somerset Emerging Markets Dividend Growth (GB00B4Q07115).

‘These offer exposure to country-specific factors, such as the compelling demographics of India, with managers finding opportunities in less researched areas of the global stock market.’ he explains.

Sector focus

Andrew Craig at Plain English Finance reckons high risk investors should consider the tech and biotech sectors when choosing equities.

‘I believe both these sectors are going to witness enormous value creation in the next decade. In the tech sector, companies who succeed in a wide range of new industries that include robotics, artificial intelligence, renewable power generation and storage, transportation, agriculture – the list goes on and on – are going to be the Apples and Googles of the next decade,’ he says.

One way to play the tech theme is via investment trust Scottish Mortgage (SMT). It invests in a global portfolio of companies which the manager believes are at the cutting edge of new technologies.

Top 10 holdings include Amazon, Alibaba, Facebook and Google’s parent company Alphabet. It has a five-year annualised return of 22.3%.

Craig likes biotech because of the significant scientific progress likely to be made over the next few years. He believes companies could achieve multi-billion dollar market valuations on the back of breakthrough drugs and other medical technologies.

‘This march of technology, married to the demographic big picture (ageing, an obesity epidemic and continued global population growth) means the addressable economic value here is enormous.

‘There will continue to be superior returns for patient investors willing to get to grips with the sector and who can look through the day-to-day noise,’ he explains.

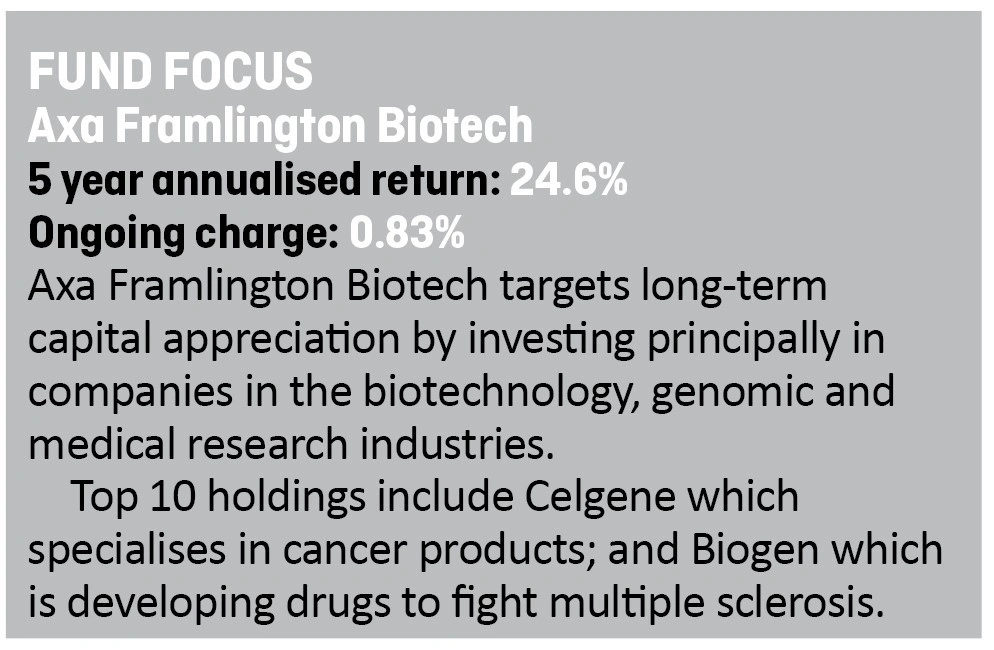

Funds in the biotech space include Axa Framlington Biotech (GB00BRJZVL27) and Biotech Growth Trust (BIOG). Both funds had a tough year in 2016 largely caused by concerns that Hillary Clinton would be elected US President and impose price controls on the healthcare industry.

Finally, someone like Martha might want to consider adding a fixed income element to their portfolio such as through a fund like M&G Emerging Markets Bond (GB0031958738) which has a five-year annualised return of 9.8%.

Cram says you can add fixed income without eliminating the potential for growth by investing in emerging market debt, which offers more attractive yields than developed economies.

DISCLAIMER: Daniel Coatsworth, who edited this article, owns shares in Scottish Mortgage

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

Feature

Great Ideas Update

Investment Trusts

Larger Companies

Main Feature

Smaller Companies

Story In Numbers

- Most popular exchange-traded funds in March 2017

- Best performing stocks in FTSE All-Share Index so far this year

- Hurricane may be sitting on ‘largest undeveloped discovery’ in North Sea

- 12.5%: Percentage of Lloyds’ loans deemed ‘high-risk’

- $54.7bn: Netflix’s blockbuster value creation

- Watkin Jones family and directors cash in £70m worth of stock

- 80: A rare ‘buy the market’ alert has been sounded for US equities

- £1m: Acacia’s daily hit from export ban