Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineFull throttle: Why AIM stocks are racing ahead

The AIM market has come out of the blocks in 2017 like Usain Bolt, leaving the mainstream stock market indices trailing in its wake. This article contains some of our best AIM stock ideas and explains why the market has been racing ahead.

The FTSE AIM All-Share index has rallied 7.9% year to date to close at 910.38 on 1 March 2017, the highest the junior index has been since 2011. That compares to a 3.7% gain from the FTSE All-Share and 4.2% advance from the FTSE Small Cap index.

The stock market’s often smallest and typically riskiest companies might appear to be suddenly attracting unprecedented attention from investors. Yet AIM’s outperformance can be tracked further back from the start of 2017.

AIM has been beating other traditional UK stock market indices for the past two years, although it really started racing away last summer.

Why has AIM rallied?

Some of this apparent new enthusiasm for the junior stock market is thanks to tax benefits that come with investing in AIM stocks. Yet Amati Global Investors small cap fund manager Douglas Lawson believes company and sector specifics are having a much larger impact on performance.

‘Nearer-term, the recovery in many resources companies is having an effect,’ he explains. Oil, gas and mining companies on AIM are collectively worth in excess of £10.6bn, or 12.6% of the AIM All-Share’s combined £84.7bn market cap at present. Even more important is the influence of AIM’s very biggest companies.

Who are the largest firms on AIM?

‘The top companies, ASOS (ASC:AIM), Boohoo (BOO:AIM), Fevertree (FEVR:AIM), Burford Capital (BUR:AIM) have done incredibly well,’ says Lawson.

That’s an understatement. Online retailer ASOS is up 78% during the past 12 months.

Boohoo, another digital fashion business, has rocketed 269% in a year; litigation funder Burford Capital is 217% ahead. Tonic water supplier Fevertree has seen its share price soar 163% over the past 12 months.

Back in January 2016 there were four companies with a market cap over £1bn; they had an aggregate market value of £7.3bn. By comparison, at the start of March 2017 there were eight AIM companies with market capitalisations in excess of £1bn. The aggregate market value stands

at £14.7bn.

‘ASOS would be a FTSE 100 company if it was on London’s Main Market,’ says Amati’s Lawson, pointing out the firm’s £4.59bn market value. The other three would theoretically all slip comfortably into the FTSE 250, among the 50-odd AIM stocks that might feasibly qualify as mid-caps.

AJ Bell investment director Russ Mould says: ‘Remember that AIM’s total market cap of £84.7bn compares to around £2tr for the FTSE 100 and once you add in the FTSE 250, Small Cap and Fledgling, AIM is only 3% to 4% of the UK total market cap.’

A shift from quantity to quality

Many experts believe there is an incremental shift from quantity to quality of companies on the AIM market. At the end of 2016 there were 982 companies quoted on AIM, down from a high of 1,694 at the end of 2007.

Research by chartered accountant UHY Hacker Young shows 105 companies left AIM in 2016; with 46 delistings caused by financial stress or strategy failure.

‘Many AIM firms are less mature than the more established concerns of the FTSE 100, FTSE 250 or even the FTSE Small Cap and as such the risks are generally higher,’ reminds AJ Bell’s Mould. ‘Companies can be more dependent on one particular geographic market, product, service or manager, so the margin for error is less if something does go wrong, as their businesses are less diverse.’

But the plunging pound has also had a big impact. Weaker sterling has made every London listed company effectively more attractive to overseas buyers. On UHY’s numbers, 34 companies were acquired from AIM in 2016, up from 28 a year earlier; 13 of them in the final quarter.

‘It’s difficult now to get an IPO (initial public offering) away if a company doesn’t tick lots of quality criteria,’ says Amati’s Lawson. ‘As well as the fairly obvious elements, such as management having a firm grasp of company financials and having a clear vision of where they want to take the business, UK investors would rather have lower growth with profits. It’s one of the differences with many fast growing US businesses.’

Sadly a large proportion of companies on AIM are under-researched by analysts, so investors don’t have the necessary research notes and earnings forecasts to help them get a better handle on the investment case.

However, you could say this situation is positive for more experienced stock pickers if they can spot opportunities not yet picked up by the broader market.

Helping you find opportunities

To help you on your investment journey, we’ve analysed the market using SharePad’s data system to give you a wealth of AIM stock ideas based on three criteria: growth, income and momentum.

We’ve looked for robust growth prospects from profitable businesses and where we think the share price will enjoy a decent lift over the next year or so. We’ve sought income opportunities backed comfortably by earnings.

We appreciate a good share price run for smaller companies can go on far longer than anyone might expect. Therefore we have looked for the best share price gains so far this year to find ‘momentum’ trades. We’ve excluded loss-making businesses and companies on soaring price to earnings (PE) multiples.

From each list we have selected our preferred option, plus picked out a couple of other interesting ideas. We hope this provides a decent level of quality control so you’ve got a more informed starting position for your own further research. Keep reading to discover our top stock picks.

GROWTH AT A REASONABLE PRICE

OPG Power Ventures (OPG:AIM) 47p

The power generator in India has spent years building its 714MW asset base of coal-to-electricity plants, and is increasingly looking at solar and wind for environmentally-friendly energy. That is good for investors who want growth and income.

Plans were dealt a major blow in February with a series of unfortunate events in the Tamil Nadu area of India capping output at the company’s Chennai-based power projects. That implies a £5m to £6m hole in revenue for the year to 31 March 2017.

In the context of market expectations of £204.5m income this year (even after downgrades) the shares’ rough 20-odd% decline looks like a big over-reaction. India will require vast new energy sources to meet requirements in the future, underpinned by both internal development and demographic change.

A first year of dividends this year implies a rough 0.8p payout shooting up to 2p in 2018 and 3p to 31 March 2019 for OPG.

Central Asia Metals (CAML:AIM) 233p

Although described as a mining stock, this is essentially a recycling business. It reprocesses waste from old copper mines in Kazakhstan to extract metal that’s been left behind. It does this at low cost, resulting in high profit margins. Strong cash generation enables it to pay a decent dividend and it is currently yielding 5.5%.

The company is highly disciplined and won’t start any new projects unless it can make a high return on investment. That approach should be applauded.

It recently said a project in Chile wouldn’t start development until it had ‘reviewed its options’. We translate as being a no-go for the project as its economics look weak. The focus now shifts back to Kazakhstan where it hopes to undertake exploration on a copper prospect.

Empresaria (EMR:AIM) 152.6p

Recruitment consultant Empresaria is enjoying considerable earnings momentum thanks to diversification benefits. It serves a wide range of sectors in many different countries.

There will inevitably be a few industries or countries where economic conditions are negative for the jobs market in any given year. Fortunately, Empresaria tends to have enough good sectors or countries to more than offset the bad ones. The shares trade on an undemanding valuation of 10.7 times forecast earnings for 2017.

Broker Arden Partners believes the shares could rise by up to 50% over the coming year. It reckons earnings per share growth will jump from 12.6% in 2016 to 22.7% in 2017.

We like Empresaria’s general bias towards temporary placements. Recruiters earn more money through permanent job placements, yet the current economic environment favours more flexibility when it comes to corporates managing staff numbers. Employers want to be able to hire people when they need them, but not be stuck with too many staff if there is a downturn in economic conditions.

Higher quality business

Earnings quality should improve thanks to recent investments. Last summer it bought New Zealand-based Rishworth which places pilots in jobs with commercial airlines, typically on three to five year contracts. Recruiters normally pay their candidates’ salaries before they get paid by clients, thereby requiring a pot of cash to cover these outgoings which is known as ‘working capital’. Empresaria says it normally gets paid 50 days later.

The situation is different with Rishworth. Airlines either pay the pilot salary costs to the recruiter in advance or within a short period. That is positive for the group’s working capital.

Empresaria also bought an IT recruitment business last year which sources talented people for jobs on innovative technology projects. Candidates are in high demand, so salaries can be fairly decent. This, in turn, generates a good chunk of commission for Empresaria.

Don’t worry about a large jump in net debt during 2016. That’s principally down to the acquisitions. It is a cash generative business and it says debt will quickly come down over the next few years.

INCOME VIA DIVIDENDS

Stadium (SDM:AIM) 95p

In-house designed bespoke solutions are dragging the electronics company higher up the value chain with judicious acquisitions accelerating the process.

Stadium has its eyes firmly fixed on niche areas where it is developing longer-term partnerships. The focus is on areas such as human machine interfaces or high-tech control panels to run complex technology kit. It also has various wireless and power components playing into an artificial intelligence background theme.

It lost a major customer last summer which hurt its share price temporarily. The shares are now slowly recovering, helped by the lure of attractive dividends from typically robust cash flow. A 3p expected dividend this year (3.2% yield) might be bolstered by a modest special dividend, in our view, after the company tidied up its balance sheet towards the end of January 2017.

Pan African Resources (PAF:AIM) 17p

The South African miner has long been known as a generous dividend payer. We’d argue that reward is necessary given it is a higher risk business than some of the bigger gold players on the London stock market.

A 4.8% prospective yield is attractive but we’d expect the share price to be quite volatile given its mixed operational track record.

Pan African has several gold mines and a platinum reprocessing operation. One of the mines, Evander, is very high grade – sadly it has a troublesome operational history both under Pan African and its previous owner Harmony Gold. There have been many fatalities over the years.

A planned gold tailings plant will help increase group gold output and bring down costs.

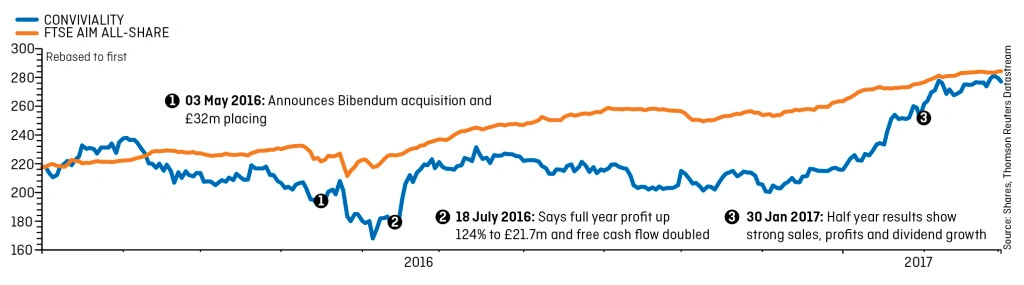

Conviviality (CVR:AIM) 279.25p

Conviviality could stand as an exemplar of all three growth, income or momentum categories. Investor awareness of its growing size and influence in the UK drinks market has helped drive up the share price and the clamour for exposure to its compelling income characteristics has returned following a brief wobble last summer amid the Brexit vote stock market sell-off.

Half year results on 31 January 2017 illustrated how the business has changed for the better through M&A. Pre-tax profit fizzed 295% higher to £15.4m on a sales surge to £782.5m (H1 2016: £252m), reflecting the transformation of Conviviality through the acquisitions of Matthew Clark, the UK’s biggest drinks distributor to the on-trade, and wines and spirits wholesaler Bibendum.

These major deals are already yielding cost synergies and cross-selling benefits, although Conviviality is serving up robust organic growth amid difficult market conditions. For the six weeks ended 1 January 2017, seasoned retailer and CEO Diana Hunter also reported positive like-for-like sales in retail, where Conviviality trades as Bargain Booze, Bargain Booze Select Convenience and Wine Rack.

Investors also warmed to the doubling of the interim dividend to 4.2p, indicating Hunter’s confidence in Conviviality’s future growth prospects and cash flow at a time when the competitive threat is evolving.

The proposed takeover of food wholesaler Booker (BOK) by Tesco (TSCO) is a competitive risk to consider. However, it is worth considering that Conviviality is an alcohol specialist rather than a broad convenience store and Bargain Booze’s keen prices should help keep the tills ringing even if the UK economy turns down.

For the financial year to April 2017, N+1 Singer forecasts pre-tax profit of £46.1m (2016: £21.7m) for earnings per share of 21.2p. That puts Conviviality on an undemanding PE of 13.2 and offering a decent 4.5% yield, based on a 12.6p dividend forecast. Analysts expect the dividend to grow to 13.6p in 2018 and 14.4p in 2019.

TAKE ADVANTAGE OF SHARE PRICE MOMENTUM

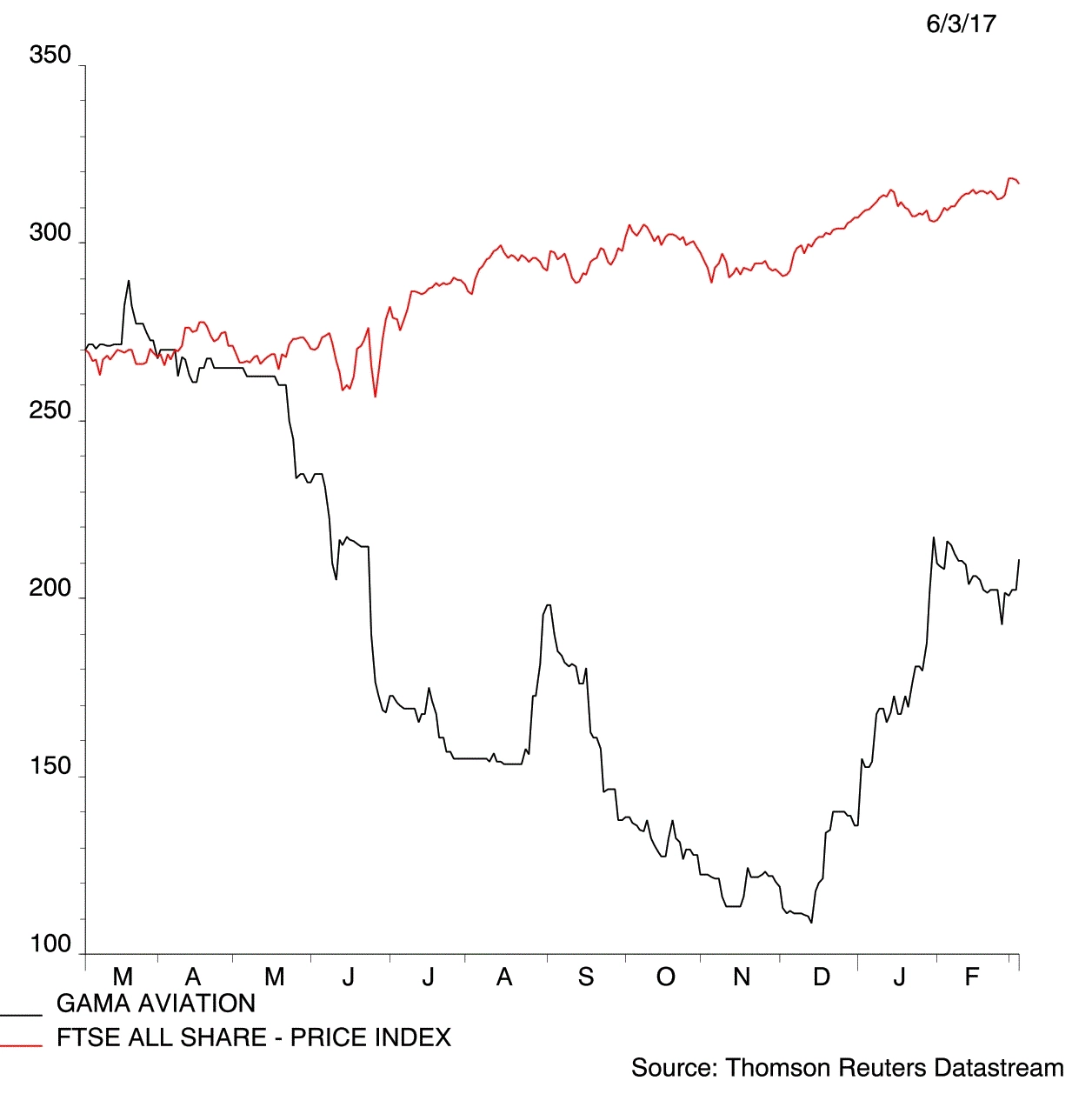

Gama Aviation (GMAA:AIM) 202.5p

Shares in Gama have raced ahead since it announced the merger of its US aircraft management and charter business with parts of BBA Aviation. This boosts the size of its managed fleet and should help achieve at least $2m cost synergies over the next two years.

Gama is a good way to get exposure to the private jet market. It undertakes aircraft maintenance and finds ways for aircraft owners to benefit from greater usage of their fleet. It also gets involved with charter work. For example, it recently won a three-year contract with the National Police Air Service for maintenance work and a five-year deal with an unnamed client to manage and fly planes to undertake aerial surveys.

Produce Investments (PIL:AIM) 194.5p

Since December, shares in potato and daffodil company Produce Investments have raced higher to 194.5p, in part reflecting increased liquidity following Toscafund Asset Management selling down and out completely.

The re-rating of Produce Investments also reflects momentum in the business. Full year results (29 Sep 2016) revealed operating profit up over 14% to £9.21m. Volumes in the core potato market steadied and Produce’s new business model helped to absorb crop price volatility.

The vertically integrated business has nearly all the major UK supermarkets as customers. Produce’s diversification into daffodils and ownership of the Jersey Royal potato brand provide some fertile grounds for expansion.

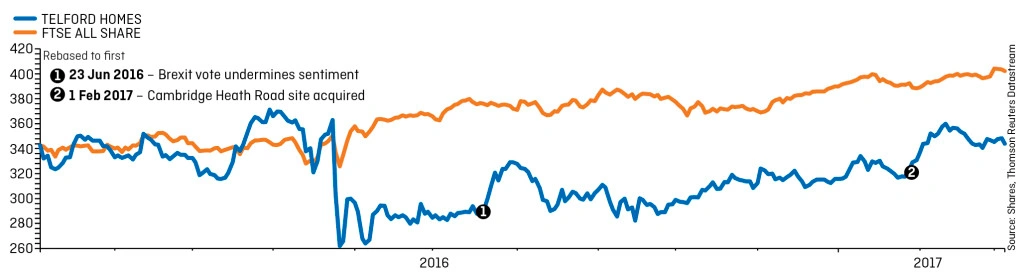

Telford Homes (TEF:AIM) 350p

We are fans of Telford Homes as we believe its niche exposure plays well into the dynamics of the London property market. The company is focused on ‘non-prime’ London, exemplified by its £30.2m purchase for development of the former London Electricity Board building in Bethnal Green in February.

Resilient demand drivers

Given the concentration of jobs in the capital and the chronic undersupply of available homes we think it is easier to predict demand for this type of development than high end properties which are often reliant on overseas purchasers. This point is particularly relevant in the wake of the Brexit vote.

The company has ambitious growth plans – aiming to double in size within five years and exceed £50m in pre-tax profit by 31 March 2019.

It has a £1.4bn pipeline at the last count, comprising some 4,000 homes. This potential and visibility is not fully reflected in the valuation. The stock trades at 1.1 times house broker Peel Hunt’s forecast March 2018 net asset value and offers a prospective yield of 4.6%.

Achieving growth will require investment and the company is already sitting on net debt of more than £100m, however increasing exposure to the ‘build-to-rent’ market could help reduce any strain on the balance sheet.

Build-to-rent or private rented sector developments see all the properties built for rent rather than sale. Increasing exposure to this space could limit borrowings in the future as the deals are typically forward funded by institutional investors.

Canaccord Genuity says: ‘The group looks well placed to significantly increase the scale of the business over the next five years, with management expecting to double its size. There is also the choice of using more build-to-rent sales to de-risk the balance sheet or to drive more growth.’

The company is next set to update on trading on 12 April.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Gear4music is hitting the high notes

- Mitie’s destruction of value

- Gold miner shock as government bans exports

- Just Eat wins back market favour

- Standard Life and Aberdeen still in play

- Large risks hang over Aggreko’s earnings

- BT breaks the billion barrier with football deal

- Who’s next as Shawbrook battles takeover approach?

Editor's View

Great Ideas Update

Investment Trusts

Larger Companies

Main Feature

Smaller Companies

Story In Numbers

- UK-Listed Asset Managers 2017

- Major Stock Market Indices 2017

- £57.7m: Centamin chairman’s non-stop share sale

- €10m: Punishing fine for data breaches

- 51%: Amount of new build homes with ‘major faults’

- £3.24: Average weekly spend on Football Pools

- Five-month low: UK business activity

- 6.5%: China scales back growth expectations