Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThe way to play Japan

There are any number of ways UK investors can gain exposure to Japan, the world’s second largest developed economy. There are plenty of open-ended and closed-ended funds to choose from but for us one investment trust stands out. It trades at a wide discount to net asset value (NAV) with scope to narrow and the ‘GARP’ approach of its relatively new manager is compelling. Step forward Fidelity Japanese Values (FJV).

Long-serving Fidelity man Nicholas Price, who has been managing money in Japan for about 16 years through any number of market cycles, says earnings are picking up in Japan and companies are generally making positive revisions to forecasts. He believes higher long-term global interest rates, a further weakening of the yen against the US dollar and continued increases in shareholder returns through dividends and buybacks should support Japanese stocks.

GARP approach

Price follows a consistent ‘growth at a reasonable price’ investment approach. ‘I utilise Fidelity’s extensive research capability in Japan and globally, but I also conduct my own research as well, looking for undercovered names in the mid and small cap space,’ says the Tokyo-based Price. ‘Companies that I own in the portfolio are definitely more focused than in the past on buybacks and dividends,’ he adds.

Since taking over as manager in 2015, the bottom-up stockpicker has reduced the number of holdings from more than 100 to 88 and pursues more of an all-cap approach than

his predecessor.

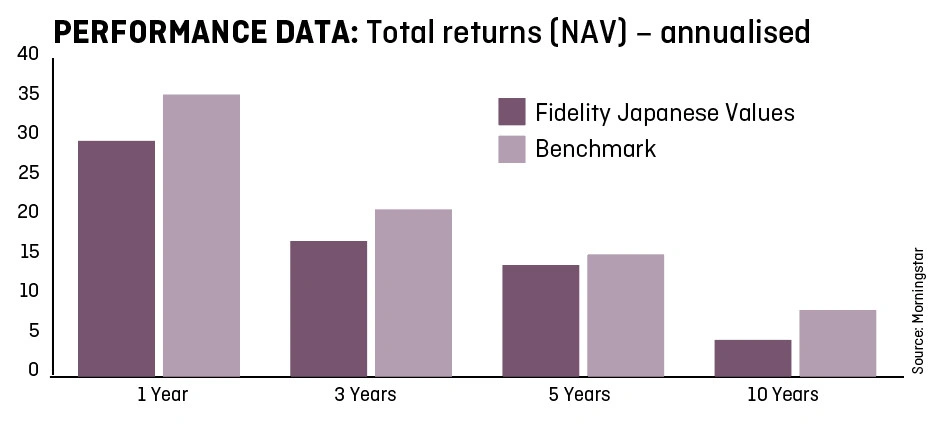

When pressed on the discount to NAV, the trust having underperformed the benchmark for many years according to Morningstar data, Price answers: ‘The key thing that will cause the discount to come in on a mid-term basis will be sustained reasonable performance of the fund against its peer group. And then periodically, the board of directors has done buybacks.’

Competitive advantage

‘My advantage is that I’m on the ground, I speak the language and I visit companies. Those companies may not be well understood in the market and that gives us an advantage as we look for their growth prospects over the mid term,’ says Price.

‘I have a fairly aggressive risk-reward profile, so I have quite a concentrated portfolio and a consistent bias towards mid and small cap growth stocks,’ adds Price, who likes companies that are transforming from stable domestic cash generators to Asian growth stories.

‘The typical name I would like would be a company that has a good runway of growth for the next three to five years, an ROE going north of 10%, a shareholder friendly management and also a relatively reasonable valuation relative to its growth.’

Price says he is not interested in hyper-growth, hyper high earnings multiples. ‘My ideal company would be one where the market is not yet recognising its growth prospects and therefore as it does and we own the stock, you get multiple expansion,’ he adds.

Big in Japan

While mid and small caps are the primary focus, one large cap stock in the portfolio is Softbank (9984:TSE), the telecom services titan steered by billionaire Masayoshi Son that bought London-listed tech giant ARM last year. Price argues the market is overlooking the immense synergies that can be achieved through the acquisition, Softbank having previously bought Sprint (S:NYSE), a listed company in the United States.

‘When we bought into Softbank, we felt the market was very negative on the Sprint acquisition, but our analysts in London and Tokyo felt that Sprint would turn around,’ says Price.

The former retail analyst is a fan of Nitori (9843:TSE), ‘the number one furniture retailer in Japan which has grown its sales and earnings consecutively for fifteen years. Up until about two years ago, the company really did no IR at all – it was a bit of a black box.

‘Recently they’ve opened up a bit more and I’ve been able to understand the growth strategy better. The company continues to grow successfully in Japan and its Chinese operation has become more profitable, with the market pricing in a higher multiple for the stock.’

He also owns Yume no Machi Souzou Iinkai (2484:TSE) which it compares to Just Eat (JE.) in the UK. However he notes more growth potential as commission rates are significantly lower than its UK counterpart.

Other names that excite Price include Kakaku.com (2371:TSE), the company behind Tabelog, a restaurant reservations site that will the key growth driver in the next few years.

Another is sports equipment brand Yonex (7906.TSE), ‘the number one in badminton globally’, currently accelerating its sales in China, one of the world’s biggest markets for players of badminton.

Fidelity's Nicholas Price

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.