Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineHas Ithaca's odyssey come to an end?

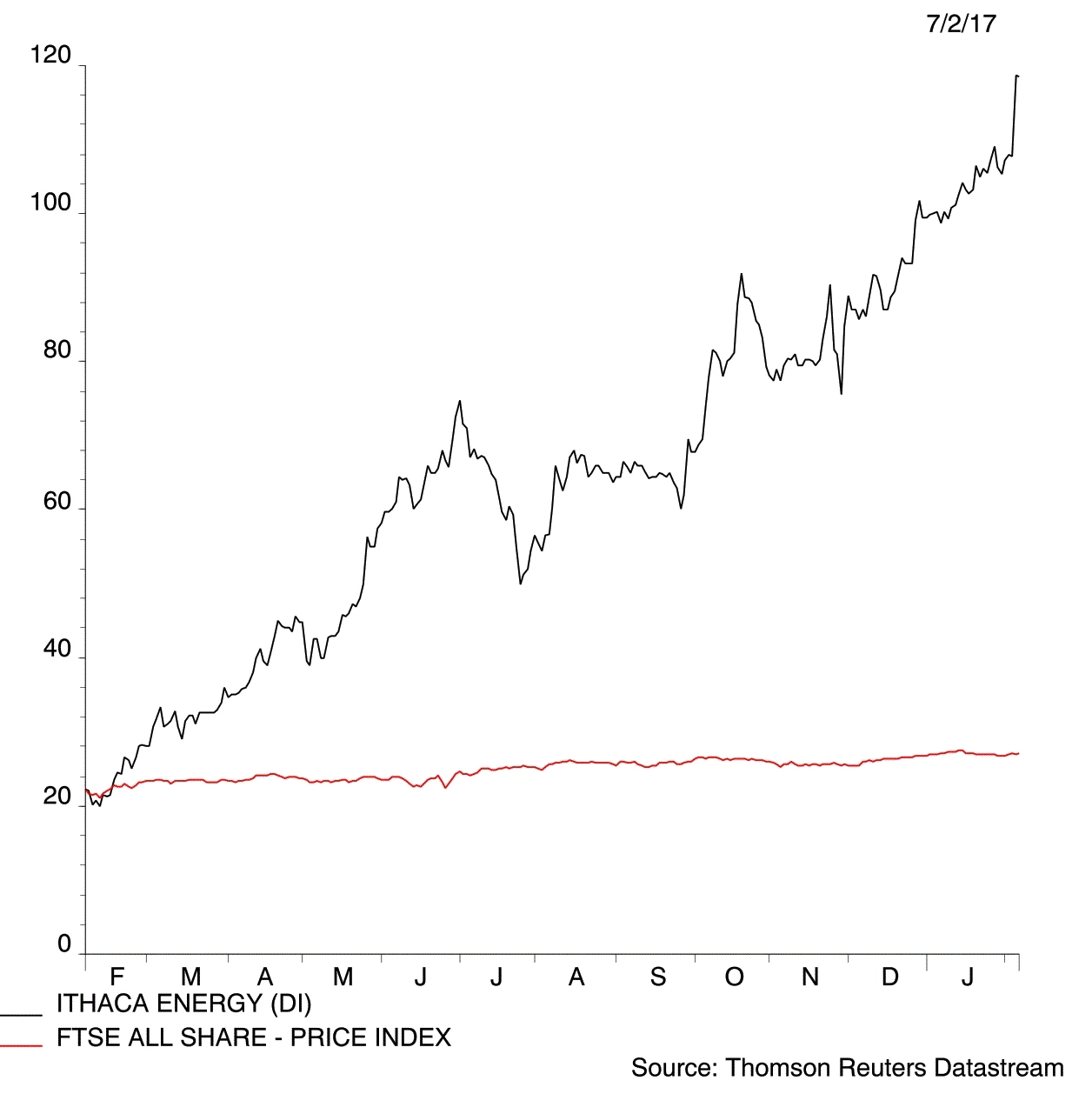

Ithaca Energy (IAE:AIM) 118.5p

Gain to date: 37.8%

Original entry point:

Buy at 86p, 22 December 2016

North Sea oil producer Ithaca Energy (IAE:AIM) is up nearly 40% on our entry price after becoming subject to a recommended 120p per share offer from Israeli firm Delek (DLKG:TLV)

(6 February).

We’d cash out now. The modest 12% bid premium has disappointed some shareholders given that Ithaca is on the cusp of substantial cash flows from its Stella field.

Paul Mumford, a fund manager at Cavendish Asset Management which is the company’s fourth largest shareholder, ‘strongly’ urges shareholders to reject the offer.

‘Ithaca’s shares have been as high as 140p per share in the past and with a further rise in oil price it could go even higher, meaning this acquisition would be relatively cheap,’ he says.

This opposition seems unlikely to derail the deal given Delek already owns 19.7% of the business. Canaccord Genuity says the valuation is ‘fair but not generous’ adding ‘the derisking effect of the all-cash offer just about offsets a slightly disappointing premium’.

It does not expect a rival bid and moves its recommendation on the stock from ‘buy’ to ‘sell’. Canaccord suggests Faroe Petroleum (FPM:AIM) could be another takeover target in the sector with Delek picking up a 13.2% stake shortly before Christmas.

Sell in the market now.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.